Table of Contents

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

| Large Accelerated Filer | ☐ | ☒ | Non-accelerated Filer | ☐ | ||||||

| Emerging growth company | ||||||||||

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

| ☐ | U.S. GAAP |

| ☒ |

| ☐ | Other |

Table of Contents

VINCI PARTNERS INVESTMENTS LTD.

TABLE OF CONTENTS

| Page | ||||

| 1 | ||||

| 5 | ||||

| PART I | ||||

| ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

7 | |||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 63 | ||||

| 63 | ||||

| 67 | ||||

| 109 | ||||

| 110 | ||||

| 111 | ||||

| 111 | ||||

| 111 | ||||

| 130 | ||||

| 133 | ||||

| 133 | ||||

| 134 | ||||

| 134 | ||||

| 134 | ||||

| 137 | ||||

| 138 | ||||

| 140 | ||||

| 141 | ||||

| F. Disclosure of a Registrant’s Action to Recover Erroneously Awarded Compensation. |

141 | |||

| 141 | ||||

| 141 | ||||

| 144 | ||||

| 145 | ||||

| 145 | ||||

| 145 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

i

Table of Contents

| 147 | ||||

| 147 | ||||

| 148 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 167 | ||||

| 167 | ||||

| 168 | ||||

| 168 | ||||

| 168 | ||||

| ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

168 | |||

| ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES |

169 | |||

| 169 | ||||

| 169 | ||||

| 169 | ||||

| 169 | ||||

| PART II | ||||

| 170 | ||||

| ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

170 | |||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| B. Management’s annual report on internal control over financial reporting |

170 | |||

| C. Attestation report of the registered public accounting firm |

171 | |||

| 171 | ||||

| 172 | ||||

| 172 | ||||

| 172 | ||||

| 172 | ||||

| ITEM 16D. Exemptions from the listing standards for audit committees |

173 | |||

| ITEM 16E. Purchases of equity securities by the issuer and affiliated purchasers |

173 | |||

| 174 | ||||

| 175 | ||||

| 175 | ||||

| ITEM 16I. Disclosure regarding foreign jurisdictions that prevent inspections |

175 | |||

| 175 | ||||

| 175 | ||||

| PART III | ||||

| 178 | ||||

| 178 | ||||

| 178 | ||||

| F-1 | ||||

ii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

All references to “U.S. dollars,” “dollars” or “$” are to the U.S. dollar. All references to “real,” “reais,” “Brazilian real,” “Brazilian reais,” or “R$” are to the Brazilian real, the official currency of Brazil. All references to “IFRS” are to International Financial Reporting Standards, as issued by the International Accounting Standards Board, or the IASB.

Financial Statements

Vinci Partners Investments Ltd., which we refer to in this annual report as “Vinci Partners,” was incorporated on September 21, 2020 as a Cayman Islands exempted company with limited liability duly registered with the Cayman Islands Registrar of Companies. Vinci Partners was incorporated to become the holding entity of Vinci Partners Investimentos Ltda., which we refer to in this annual report as “Vinci Partners Brazil.” Until the contribution of Vinci Partners Brazil’s quotas to us by Vinci Partners Brazil’s quotaholders prior to the consummation of our initial public offering on February 1, 2021, or our IPO, Vinci Partners had not commenced its operations and had only nominal assets and liabilities and no material contingent liabilities or commitments. Please refer to “Item 4. Information on the Company—C. Organizational Structure” for a description of the operations of our material operating subsidiaries.

We present in this annual report the audited consolidated financial statements of Vinci Partners for the years ended December 31, 2023, 2022 and 2021. The audited consolidated financial statements of Vinci Partners were prepared in accordance with IFRS Accounting Standards, as issued by the IASB.

Vinci Partners maintains their books and records in Brazilian reais, the presentation currency for their financial statements and also the functional currency of our operations in Brazil. Unless otherwise noted, the financial information presented herein as of December 31, 2023 and 2022, and for the years ended December 31, 2023, 2022 and 2021, is stated in Brazilian reais, our reporting currency. The consolidated financial information of Vinci Partners contained in this annual report is derived from Vinci Partners’ audited consolidated financial statements as of December 31, 2023, 2022 and 2021, and for the years ended December 31, 2023, 2022 and 2021, together with the notes thereto. All references herein to “our financial statements,” “our audited consolidated financial information,” and “our audited consolidated financial statements” are to the audited consolidated financial statements of Vinci Partners included elsewhere in this annual report. All references herein to “we,” “us,” “our,” or the “Company” are to Vinci Partners.

This financial information should be read in conjunction with “Item 5. Operating and Financial Review and Prospects” and our audited consolidated financial statements, including the notes thereto, included elsewhere in this annual report.

Our fiscal year ends on December 31. References in this annual report to a fiscal year, such as “fiscal year 2023,” relate to our fiscal year ended December 31 of that calendar year.

Financial Information in U.S. Dollars

Solely for the convenience of the reader, we have translated some of the real amounts included in this annual report from reais into U.S. dollars. You should not construe these translations as representations by us that the amounts actually represent these U.S. dollar amounts or could be converted into U.S. dollars at the rates indicated. Unless otherwise indicated, we have translated real amounts into U.S. dollars using a rate of R$4.8413 to US$1.00, the commercial selling rate for U.S. dollars as of December 31, 2023, as reported by the Brazilian Central Bank (Banco Central do Brasil), or the Brazilian Central Bank.

Special Note Regarding Non-GAAP Financial Measures

This annual report presents our FRE, FRE Margin, PRE, PRE Margin, Distributable Earnings, and Distributable Earnings Margin, which are non-GAAP financial measures, and their reconciliations to the nearest measure as defined by IFRS Accounting Standards, for the convenience of investors.

Table of Contents

We present Fee Related Earnings, or FRE, because we believe this metric is useful to monitor the baseline performance of, and trends in, our business, in a manner that does not include performance fees, investment income and expenses that do not arise from our normal course of operations. FRE is calculated as operating profit, less (a) net revenue from realized performance fees, less (b) net revenue from unrealized performance fees, plus (c) share-based payments plus (d) compensation allocated in relation to performance fees plus (e) non-operational expenses, which are comprised of expenses relating to professional services rendered in connection with acquisitions and our international corporate organization (which expenses were added to the calculation of FRE beginning in the year ended December 31, 2022 to ensure the metric’s usefulness as a tool to assess our ability to generate profits from revenues and expenses arising out of our normal course of operations). FRE Margin is calculated as FRE divided by the sum of net revenue from fund management and net revenue from advisory services.

We present Performance Related Earnings, or PRE, because we believe this measure can provide useful information as a performance measure that we use to assess our ability to generate profits from revenue that relies on outcomes from funds above their respective benchmarks. We calculate PRE as operating profit less (a) net revenue from fund management, less (b) net revenue from advisory services, plus (c) personnel and profit-sharing expenses, plus (d) other general and administrative expenses, less (e) compensation in relation to performance fees. PRE Margin is calculated as PRE divided by net revenue from performance fees.

We present Distributable Earnings as a metric used by our board of directors to assess our performance and capabilities to distribute dividends to our shareholders. Distributable Earnings is calculated as profit for the year, less (a) net revenue from unrealized performance fees, plus (b) income taxes from unrealized performance fees, plus (c) compensation allocated in relation to unrealized performance fees, less (d) unrealized gain from investment income, plus (e) income taxes on unrealized gain from investment income, plus (f) share-based payments, plus (g) income taxes on share-based payments, plus (h) depreciation and amortization, except for depreciation and amortization relating to each segment’s investments, less (i) contingent consideration (earn-out) gain (loss) (after tax) (which expenses were added to the calculation of Distributable Earnings beginning in the year ended December 31, 2022 in light of a new line item in our financial statements, contingent consideration (earn-out) gain (loss), which may become payable in future periods a result of our acquisition of SPS Capital in the year ended December 31, 2022 (see “Item 4. Information on the Company—A. History and Development of the Company—Our History—Acquisition of SPS Capital”)). Distributable Earnings Margin is calculated as Distributable Earnings divided by sum of net revenue from fund management, net revenue from performance fees, net revenue from advisory services and realized gain from investment income.

FRE, FRE Margin, PRE, PRE Margin, Distributable Earnings and Distributable Earnings Margin as described in this annual report are non-GAAP measures that are not a substitute for the IFRS Accounting Standards measures of earnings. Additionally, our calculation of these measures may be different from the calculation used by other companies, including our competitors in the financial services industry, and therefore, our measures may not be comparable to those of other companies.

In addition, this annual report presents our Adjusted Distributable Earnings, Adjusted Distributable Earnings Margin, Adjusted Profit for the year, and Adjusted Profit Margin for the year, which are non-GAAP financial measures, and their reconciliations to the nearest measure as defined by IFRS Accounting Standards, for the convenience of investors. Our Distributable Earnings, Distributable Earnings Margin, profit for the year and profit margin differ for the years ended December 31, 2023 and 2022 differ from our Adjusted Distributable Earnings, Adjusted Distributable Earnings Margin, Adjusted Profit and Adjusted Profit Margin, respectively, as a result of the adjustments described in this annual report.

We present Adjusted Distributable Earnings as a reference point by our board of directors for determining the amount of earnings available to distribute to shareholders as dividends. Adjusted Distributable Earnings is calculated as Distributable Earnings, less non-operational expenses, which are comprised of expenses relating to professional services rendered in connection with acquisitions and our international corporate organization (including income tax related to realized expense). Beginning in the year ended December 31, 2022, management updated the definition of Adjusted Distributable Earnings previously reported in our annual report on Form 20-F in light of certain non-operational expenses relating to professional services rendered in connection with our acquisitions and our international corporate organization, in order to ensure the metric’s usefulness as a tool to assess our ability to generate profits from revenues and expenses arising out of our normal course of operations. Adjusted Distributable Earnings Margin is calculated as Adjusted Distributable Earnings divided by the sum of net revenue from fund management, net revenue from performance fees, and net revenue from advisory services and realized gain from investment income.

2

Table of Contents

We present Adjusted Profit for the year because management evaluates this measure and we believe it can provide useful information to investors and analysts regarding the net results of our business. We calculate Adjusted Profit for the year as profit for the year less (a) non-operational expenses, which are comprised of expenses relating to professional services rendered in connection with acquisitions and our international corporate organization (including income tax related to realized expense), and (b) contingent consideration (earn-out) gain (loss) (after tax). Beginning in the year ended December 31, 2022, management updated the definition of Adjusted Distributable Earnings previously reported in our annual report on Form 20-F in light of (i) certain non-operational expenses relating to professional services rendered in connection with our acquisitions and our international corporate organization, in order to ensure the metric’s usefulness as a tool to assess our ability to generate profits from revenues and expenses arising out of our normal course of operations, and (ii) a new line item in our financial statements, contingent consideration (earn-out) gain (loss), which may become payable in future periods a result of our acquisition of SPS Capital in the year ended December 31, 2022. See “Item 4. Information on the Company—A. History and Development of the Company—Our History—Acquisition of SPS Capital.” Adjusted Profit Margin for the year is calculated as Adjusted Profit for the year divided by the sum of net revenue from fund management and net revenue from advisory services.

Adjusted Distributable Earnings, Adjusted Distributable Earnings Margin, Adjusted Profit, and Adjusted Profit Margin for the year as described in this annual report are non-GAAP measures that are not a substitute for the IFRS Accounting Standards measures of earnings. Additionally, our calculation of these measures may be different from the calculation used by other companies, including our competitors in the financial services industry, and therefore, our measures may not be comparable to those of other companies. See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Non-GAAP Financial Measures and Reconciliations” for the reconciliation of our non-GAAP financial measures.

Market Share and Other Information

This annual report contains data related to economic conditions in the market in which we operate. The information contained in this annual report concerning economic conditions is based on publicly available information from third-party sources that we believe to be reasonable. Market data and certain industry forecast data used in this annual report were obtained from internal reports and studies, where appropriate, as well as estimates, market research, publicly available information (including information available from the United States Securities and Exchange Commission website) and industry publications. We obtained the information included in this annual report relating to the industry in which we operate, as well as the estimates concerning market shares, through internal research, public information and publications on the industry prepared by official public sources, such as the Brazilian Central Bank or the World Bank, as well as private sources, such as the Brazilian Financial and Capital Markets Association (Associação Brasileira das Entidades dos Mercados Financeiro e de Capitais), or ANBIMA, B3 S.A. – Brasil, Bolsa Balcão, or the B3 , Bloomberg, the National Economic and Social Development Bank (Banco Nacional de Desenvolvimento Econômico e Social), or BNDES, CVM, Inter.B Consultoria Internacional de Negócios, McKinsey & Company, Oliver Wyman, and Reuters, among others.

Industry publications generally state that the information they include has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Although we have no reason to believe any of this information or these reports are inaccurate in any material respect and believe and act as if they are reliable, neither we nor our agents have independently verified it. Governmental publications and other market sources, including those referred to above, generally state that their information was obtained from recognized and reliable sources, but the accuracy and completeness of that information is not guaranteed. In addition, the data that we compile internally, and our estimates have not been verified by an independent source. Except as disclosed in this annual report, none of the publications, reports or other published industry sources referred to in this annual report were commissioned by us or prepared at our request. Except as disclosed in this annual report, we have not sought or obtained the consent of any of these sources to include such market data in this annual report.

3

Table of Contents

Rounding

We have made rounding adjustments to some of the figures included in this annual report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

4

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this annual report can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate” and “potential,” among others.

Forward-looking statements appear in a number of places in this annual report and include, but are not limited to, statements regarding our intent, belief or current expectations. Forward-looking statements are based on our management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to various factors, including, but not limited to, those identified under the section entitled “Item 3. Key Information—D. Risk Factors” in this annual report. These risks and uncertainties include factors relating to:

| • | general economic, financial, political, demographic and business conditions in Brazil, as well as any other countries we may invest and attract investors from in the future and their impact on our business; |

| • | fluctuations in interest, inflation and exchange rates in Brazil and any other countries we may serve in the future; |

| • | competition in the investment advisory and financial services industry; |

| • | our ability to implement our business strategy; |

| • | the investment performance of investment funds managed by our asset managers or by third parties; |

| • | the availability of government authorizations on terms and conditions and within periods acceptable to us; |

| • | our ability to continue attracting and retaining new appropriately skilled employees; |

| • | our capitalization and ability to fund new investments or integrate new acquisitions, including our pending business combination with Compass (see “Item 4. Information on the Company—A. History and Development of the Company—Recent Events—Business Combination with Compass”); |

| • | our ability to adapt to the rapid pace of technological changes in the financial services industry; |

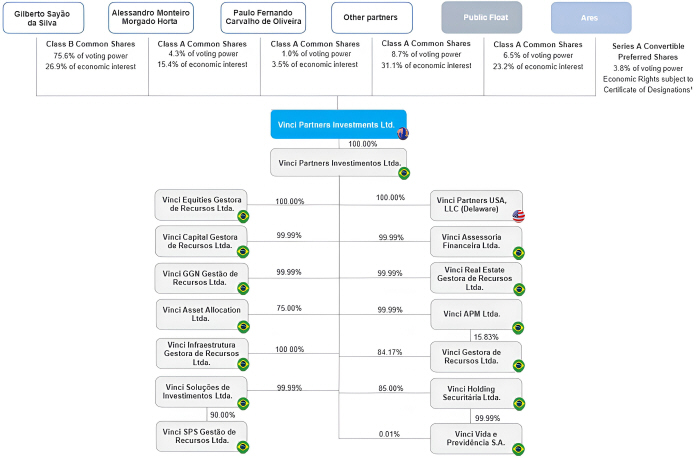

| • | the interests of our controlling shareholder, Gilberto Sayão da Silva, who owns 100% of our outstanding Class B common shares, which represents approximately 75.6% of the voting power of our issued share capital; |

| • | changes in government regulations applicable to the financial services and insurance industries in Brazil and elsewhere; |

| • | our ability to compete and conduct our business in the future; |

| • | the success of operating initiatives, including advertising and promotional efforts and new product, service and concept development by us and our competitors; |

| • | changes in investors’ demands regarding investment products, customer experience related to investments and technological advances, and our ability to innovate to respond to such changes; |

| • | changes in labor, distribution and other operating costs; |

| • | our compliance with, and changes to, government laws, regulations and tax matters that currently apply to us; |

| • | the actual and potential effects of health crises and their potential to have an ongoing adverse impact on global, regional and national economies; |

5

Table of Contents

| • | other factors that may affect our financial condition, liquidity, and results of operations; and |

| • | other risk factors discussed under “Item 3. Key Information—D. Risk Factors.” |

Forward-looking statements speak only as of the date they are made, and we do not undertake any obligation to update them in light of new information or future developments or to release publicly any revisions to these statements in order to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

6

Table of Contents

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | Directors and Senior Management |

Not applicable.

| B. | Advisers |

Not applicable.

| C. | Auditors |

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

| A. | Offer Statistics |

Not applicable.

| B. | Method and Expected Timetable |

Not applicable.

ITEM 3. KEY INFORMATION

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

This section is intended to be a summary of more detailed discussions contained elsewhere in this annual report. You should carefully read and consider the following risks, along with the other information included in this annual report. The risks described below are not the only ones we face. Additional risks that we do not presently consider material, or of which we are not currently aware, may also affect us. Our business, results of operations or financial condition could be impacted if any of these risks materialize and, as a result, the market price of our common shares could be affected. The risks described below are organized by risk category and these categories are not presented in order of importance. However, within each category, the risk factors are presented in descending order of importance, as determined by us as of the date of this annual report. We may change our vision about their relative importance at any time, especially if new internal or external events arise.

Summary of Risk Factors

Risks Relating to Our Business and Industry

| • | Adverse market and economic conditions could reduce the value or performance of our funds. |

Our business and the businesses of the companies in which our funds invest are materially affected by financial markets and economic conditions or events throughout the world, such as interest rates, availability of credit, inflation rates, economic uncertainty, changes in laws, trade barriers and trade tension, commodity prices, currency exchange rates and controls and national and international political circumstances. Future market conditions may be less favorable compared to current and historical market conditions and we could suffer a decrease in our performance and management fees, and a decrease in investment income we earn from our proprietary investments.

7

Table of Contents

| • | Fluctuations in interest rates, exchange rates and benchmark indices could have an adverse effect on us. |

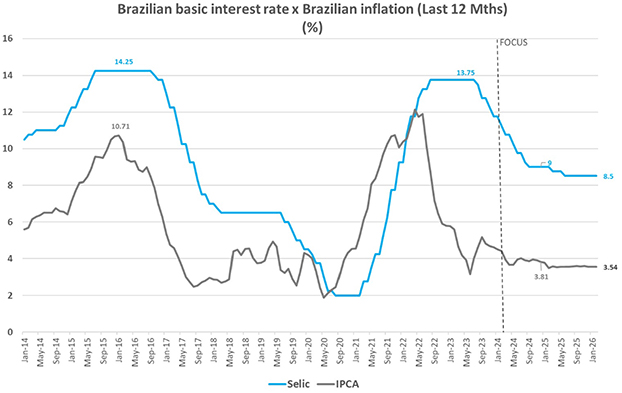

Certain of our funding costs and the returns on certain of our investment funds are tied to certain interest rate indices or other benchmark indices, such as the Brazilian long-term interest rates (taxa de juros de longo prazo or taxa de longo prazo), or the TJLP/TLP rates, the Brazilian interbank deposit rate (taxa de depósito interbancário), or the CDI Rate, the Brazilian basic interest rate (taxa SELIC), or the SELIC Rate, certain inflation indices and certain B3 indices. In addition, carrying costs and the returns on certain of our investment funds based in the United States are tied to or denominated in U.S. dollars, exposing us to risks associated with fluctuations in rate of exchange of U.S. dollars for Brazilian reais. We may not be able to adequately manage our exposure to these benchmarks, which could lead to increased funding costs, carrying costs or decreased returns for our funds, with a consequent adverse effect on our business, financial condition and results of operations.

| • | Substantial and increasingly intense competition within our industry may harm our business. |

The financial services market is highly competitive. Many of our competitors may have substantially greater resources than we do. These competitors may be able to offer more attractive fees to our current and prospective clients, especially our competitors that are affiliated with financial institutions. Competition could cause us to reduce the performance and management fees and financial services advisory fees we charge for our services and could also result in a loss of existing clients, and greater difficulty in attracting new clients.

| • | We may not be able to keep pace with rapid developments in our industry. |

The financial services market is characterized by rapid technological change, new product and service introductions, evolving industry standards, changing client needs and the entrance of non-traditional competitors. There can be no assurance that we will have the funds available to maintain the levels of investment required to support our projects, and if we are unable to develop, adapt to or take advantage of technological changes or evolving industry standards, our business, financial condition and results of operations could be materially adversely affected.

| • | We have identified material weaknesses in our internal control over financial reporting. |

In connection with the preparation of our consolidated financial statements for the years ended December 31, 2023 and 2022, we identified a number of material weaknesses in our internal control over financial reporting as of December 31, 2023 and 2022. The material weaknesses identified refer to our insufficient accounting processes necessary to comply with the reporting and compliance requirements of IFRS Accounting Standards and the U.S. Securities and Exchange Commission, or the SEC. We have a remediation plan to improve our internal control over financial reporting, but there is no assurance that our efforts will be effective or prevent any future material weaknesses in our internal control over financial reporting.

Risks Relating to the Compass Transaction

| • | We are subject to risks relating to the pending Compass Transaction. |

The risks arising out of our pending business combination with Compass include the following: our shareholders having reduced ownership and voting interest in and less influence over the combined company; disruptions in business relationships; prohibitions from entering into certain transactions and taking certain actions that might otherwise be beneficial to us until completion of the Compass Transaction; third parties terminating existing relationships with us or Compass; obtaining required approvals and satisfying closing conditions; potential termination of the Compass Transaction; difficulty attracting, motivating and retaining key employees; the incurrence of significant expenses; and the adequacy of our due diligence investigation of Compass.

| • | We are subject to risks relating to the combined company following closing of the Compass Transaction. |

The risks relating to the combined company following our business combination with Compass include the following: our failure to realize the anticipated benefits of the Compass Transaction; the incurrence of significant integration-related costs and realizing the synergies of the combined company; and different factors affecting the market price for our Class A common shares following the completion of the Compass Transaction.

8

Table of Contents

Risks Relating to Brazil and Latin America

| • | The Brazilian federal government has exercised significant influence over the Brazilian economy. |

The Brazilian federal government frequently exercises significant influence over the Brazilian economy and occasionally makes significant changes in policy and regulations. We have no control over and cannot predict what measures or policies the Brazilian government may take in the future. We and the market price of our Class A common shares may be harmed by changes in Brazilian government policies, as well as general economic factors.

| • | Economic uncertainty and political instability in Brazil may harm us. |

Brazil’s political environment has historically influenced, and continues to influence, the performance of the country’s economy. Political crises have affected and continue to affect the confidence of investors and the general public, which have historically resulted in economic deceleration and heightened volatility in the securities offered by companies with significant operations in Brazil. Ongoing political uncertainty could harm the Brazilian economy and, consequently, our business and the value of our investments, and could adversely affect our financial condition, results of operations and the price of our Class A common shares.

Risks Relating to Our Class A Common Shares

| • | The concentration of our ownership and voting power with Gilberto Sayão da Silva limits your ability to influence corporate matters. |

Gilberto Sayão da Silva controls our company through his beneficial ownership of all of our outstanding Class B common shares, representing 75.6% of the combined voting power of our issued share capital. So long as Mr. Sayão da Silva beneficially owns a sufficient number of Class B common shares, even if he beneficially owns significantly less than 50% of our outstanding share capital, he will be able to effectively control our decisions.

| • | As a Cayman Islands exempted company with limited liability, the rights of our shareholders may be different from the rights of shareholders governed by the laws of U.S. jurisdictions. |

Our corporate affairs are governed by our Articles of Association and by the laws of the Cayman Islands. The rights of shareholders and the responsibilities of members of our board of directors may be different from the rights of shareholders and responsibilities of directors in companies governed by the laws of U.S. jurisdictions. In particular directors of a Cayman Islands company owe fiduciary duties to the company and separately a duty of care, diligence and skill to the company, whereas under Delaware corporate law, a director has a fiduciary duty to the corporation and its stockholders.

Certain Risks Relating to Our Business and Industry

Difficult market and economic conditions can adversely affect our business in many ways, including by reducing the value or performance of the investments that we manage or by reducing the ability of our funds to raise or deploy capital, each of which could negatively impact our net income and cash flow and adversely affect our financial prospects and condition.

Our business and the businesses of the companies in which our funds invest are materially affected by financial markets and economic conditions or events throughout the world, such as interest rates, availability of credit, inflation rates, economic and political uncertainty, such as those deriving from the Brazilian government, changes in laws (including laws relating to taxation), trade barriers and trade tension (including between the United States and China), commodity prices, currency exchange rates and controls and national and international political circumstances (including wars, such as the ongoing war between Ukraine and Russia, the ongoing war between Israel and Hamas, terrorist acts or security operations). Future market conditions may be less favorable compared to current and historical market conditions. Adverse conditions in financial markets and the economy can adversely impact our results of operations and financial condition by decreasing our AUM (both directly through a decline in market value or through clients withdrawing investments) and thereby decrease our performance and management fees, as well as by decreasing the investment income we earn from our proprietary investments.

9

Table of Contents

Fluctuations in financial markets and economic conditions are outside our control and may affect the level and volatility of securities prices and liquidity and as a result, the value of our investments and our financial results. In addition, we may not be able to or may choose not to manage our exposure to these conditions and/or events. If not otherwise offset, declines in the equity, commodity and debt in the markets would likely cause us to write down our investments and the investments of our funds. Our profitability may also be materially and adversely affected by our fixed costs and the possibility that we would be unable to scale back other costs within a time frame sufficient to match any decreases in net income relating to a downturn in market and economic conditions.

Unfavorable market and economic conditions may reduce opportunities for our funds to make, exit and realize value from their investments. Challenging market and economic conditions, including those caused by changes in tax laws and other regulatory restrictions, may make it difficult for us to find suitable investments for our funds or secure financing for investments on attractive terms. Such conditions may also result in reduced opportunities for our funds to exit and realize value from their existing investments and lower-than-expected returns on existing investments. Throughout our history, we have exited our portfolio companies through a combination of routes, including selling to strategic buyers, carrying out sponsor to sponsor transactions and through public market exits, including through initial public offerings, or IPOs, and reverse mergers into listed companies. In challenging equity markets, our funds may experience greater difficulty in realizing value from investments. In addition, when financing is not available or becomes too costly, it is difficult for potential buyers to raise sufficient capital to purchase our funds’ investments. Consequently, we may earn lower-than-expected returns on investments, which could cause us to realize diminished or no performance fees, which are typically determined by reference to performance in excess of one or more specified benchmarks.

We generally raise capital for a successor fund following the substantial and successful deployment of capital from the existing fund. In the event of poor performance by existing funds, our ability to raise new funds is impaired. Our fundraising may also be negatively impacted by any change in or rebalancing of fund investors’ asset allocation policies. During periods of unfavorable fundraising conditions, fund investors may negotiate for lower fees, different fee sharing arrangements for transaction or other fees, and other concessions. The outcome of such negotiations could result in our agreement to terms that are materially less favorable to us than for prior funds we have managed. Our current funds, including all our recent private equity funds, have performance hurdles, which require us to generate a specified return on investment prior to our right to receive performance fees. This requirement will likely be in all our future funds, and the hurdle rate could increase for our future funds. In addition, successor funds raised by us when such unfavorable circumstances exist would also likely result in smaller funds than our comparable predecessor funds. Fund investors may also seek to redeploy capital away from certain of our credit or other non-private equity investment vehicles, which permit redemptions on relatively short notice, in order to meet liquidity needs or invest in other asset classes or with other managers. Any of these developments could materially and adversely affect our future revenues, net income, cash flow, financial condition or ability to retain our employees.

In addition, our ability to raise capital could be adversely affected by general conditions in the global economy and in the global financial markets, including as a result of the turmoil caused in the banking sector by current macroeconomic conditions. For example, on March 10, 2023, Silicon Valley Bank was closed by the California Department of Financial Protection and Innovation and the Federal Deposit Insurance Corporation was appointed receiver of Silicon Valley Bank. On March 11, 2023, Signature Bank was similarly closed and placed into receivership. Although we did not hold deposits at these financial institutions, our banking relationships and cash deposits could be adversely affected by the volatility in the U.S. banking system and our capital raising ability may be impacted by any downturn caused in the availability of liquidity caused by disruptions to the U.S. banking system or the banking system globally.

During periods of difficult market or economic conditions or slowdowns (which may occur across one or more industries, sectors or geographies), companies or assets in which we have invested may experience decreased revenues, financial losses, credit rating downgrades, difficulty in obtaining access to financing and increased funding costs. These companies may also have difficulty in expanding their businesses and operations or be unable to meet their debt service obligations or pay other expenses as they become due, including amounts payable to us. Negative financial results in our funds’ portfolio companies may result in lower investment returns for our

10

Table of Contents

investment funds, which could materially and adversely affect our operating results and cash flow. To the extent the operating performance of such portfolio companies (as well as valuation multiples) deteriorate or do not improve, our funds may sell those assets at values that are less than we projected or even at a loss, thereby significantly affecting those funds’ performance and consequently our operating results and cash flow and resulting in lower or no performance fees being paid to us. Adverse conditions may also increase the risk of default with respect to private equity, credit and other investments that we manage or the abandonment or foreclosure of our real asset investments. Even if economic and market conditions do improve broadly, adverse conditions in particular sectors may also cause our performance to suffer. In addition, low interest rates related to monetary stimulus, economic stagnation or deflation may negatively impact expected returns on all types of investments as the demand for relatively higher return assets increases and the supply decreases. As a result, adverse conditions in financial markets as described above, as well as lower level of transaction activities involving our funds’ investments, which can be unpredictable and outside our control, may negatively impact both the frequency and size of fees generated by our business.

Our performance is subject to the risks of the industries and businesses in which the portfolio companies of our investment funds operate.

Our performance directly ties-in to the payment of fund management and performance fees by our investment funds, which, in turn, are subject to a number of risks inherent to their operations and also to the risk of the businesses and industries in which the portfolio companies of such investment funds operate, as well as fees for advisory services, which are subject to transaction closings and realization of IPOs advised by Vinci Partners. Some of these industries are particularly noteworthy for the inherent risks therewith associated, such as infrastructure and real estate. These risks include but are not limited to, those associated with the burdens of ownership of real property, general and local economic conditions, changes in supply of and demand for competing properties in an area (as a result, for instance, of overbuilding), operating income, the financial resources of tenants, changes in building, environmental, zoning and other laws, casualty or condemnation losses, energy and supply shortages, various uninsured or uninsurable risks, natural disasters, changes in government regulations (such as rent control or operational licenses), changes in real property tax rates, changes in income tax rates, changes in interest rates, the reduced availability of mortgage funds which may render the sale or refinancing of properties difficult or impracticable, increased mortgage defaults, increases in borrowing rates, changes to the taxation of business entities and the deductibility of corporate interest expense or other applicable tax exemptions or benefits, negative developments in the economy that depress travel activity, environmental liabilities, contingent liabilities on disposition of assets, acts of god, terrorist attacks, war and other factors that are beyond our control. In addition, the acquisition of direct or indirect interests in undeveloped land or underdeveloped real property, which may often be non-income producing, is subject to the risks normally associated with such assets and development activities, including risks relating to the availability and timely receipt of zoning and other regulatory or environmental approvals and licenses, the cost and timely completion of construction (including risks beyond the control of our fund, such as weather or labor conditions or material shortages) and the availability of both construction and permanent financing on favorable terms. Additionally, the investment in energy, manufacturing, transportation, water and sanitation, and other infrastructure capital-intensive projects, as well as the development and operation of assets associated with real estate and certain other assets, may expose our investment funds, and, consequently, us, to increased environmental liabilities that are inherent in the ownership of such assets, which under the applicable laws may be imposed regardless of fault.

Changes in the debt financing markets may negatively impact the ability of our investment funds’ portfolio companies and strategies pursued with our balance sheet assets to obtain attractive financing for their investments or to refinance existing debt and may increase the cost of such financing or refinancing if it is obtained, which could lead to lower-yielding investments and potentially decrease our net income.

In the event that our portfolio companies regularly utilize the corporate debt markets in order to obtain financing for their operations, to the extent that credit markets render such financing difficult to obtain or more expensive, this may negatively impact the operating performance of those portfolio companies and, therefore, the investment returns on our funds. In addition, to the extent that conditions in the credit markets impair the ability of our portfolio companies to refinance or extend maturities on their outstanding debt, either on favorable terms or at all, the operating performance of those portfolio companies may be negatively impacted, which could impair the value of our investment in those portfolio companies and lead to a decrease in the investment income earned by us. In some cases, the inability of our portfolio companies to refinance or extend maturities may result in the inability of those companies to repay debt at maturity or pay interests when due, and may cause the companies to sell assets, undergo a recapitalization or seek bankruptcy protection, any of which would also likely impair the value of our investment and lead to a decrease in investment income earned by us.

11

Table of Contents

Our failure to comply with investment guidelines set by our clients could result in damage awards against us or a reduction in AUM, either of which would cause our earnings to decline and adversely affect our business and financial condition.

When clients retain us to manage assets on their behalf, they specify certain guidelines regarding investment allocation and strategy that we are required to observe in the management of their portfolios. Our failure to comply with these guidelines and other limitations could result in clients terminating their investment management agreement with us and forcing an early redemption of their investments in our funds, as these investment agreements generally are terminable without cause on 30 days’ notice, and/or permit our clients to force an early redemption of their investment without prior notice or on relatively short notice. Clients could also sue us for breach of contract and seek to recover damages from us. In addition, such guidelines may restrict our ability to pursue certain allocations and strategies on behalf of our clients that we believe are economically desirable, which could similarly result in losses to a client, early redemption of a client’s quota, or termination of the asset management agreement and a corresponding reduction in AUM. Even if we comply with all applicable investment guidelines, a client may be dissatisfied with its investment performance or our services or fees, and may terminate their asset management agreements, redeem their quotas or be unwilling to commit new capital to our specialized funds or separate management accounts. Any of these events could cause our earnings to decline and materially and adversely affect our business, financial condition and results of operations.

Fluctuations in interest rates, exchange rates and certain benchmark indices could impact our funding costs and the value of our funds, and fluctuations in these rates and benchmarks could adversely affect our funding costs and the returns on certain of our funds, which could have a material adverse effect on our funds’ liquidity, results of operations and financial condition.

Certain of our funding costs and the returns on certain of our investment funds are tied to certain interest rate indices or other benchmark indices, such as the TJLP/TLP rates, the CDI Rate, the SELIC Rate, certain inflation indices and certain B3 indices. In addition, carrying costs and the returns on certain of our investment funds based in the United States are tied to or denominated in U.S. dollars, exposing us to risks associated with fluctuations in rate of exchange of U.S. dollars for reais. We have no control over fluctuations in interest rates, market indices or exchange rates and we may not be able to adequately manage our exposure to these benchmarks, which could lead to increased funding costs, carrying costs or decreased returns for our funds, which would have a material adverse effect on our business, financial condition and results of operations. See “—Certain Risks Relating to Brazil—Inflation and certain measures by the Brazilian government to curb inflation have historically harmed the Brazilian economy and Brazilian capital markets, and high levels of inflation in the future would harm our business and the price of our Class A common shares” and “—We are exposed to fluctuations in foreign currency exchange rates and may enter into derivatives transactions to manage our exposure to exchange rate risk.”

We have significant liquidity requirements, and adverse market and economic conditions may adversely affect our sources of liquidity, which could adversely affect our financial condition and results of operations.

We expect that our primary liquidity needs will consist of cash required to:

| • | continue to grow our business lines, including seeding new strategies, funding our capital commitments made to existing and future funds (which, as of December 31, 2023, amounted to R$630.5 million), and otherwise supporting investment vehicles that we sponsor; |

| • | service any contingent liabilities that may give rise to future cash payments; and |

| • | fund cash operating expenses and contingencies, including for litigation matters. |

These liquidity requirements are significant and, in some cases, may require cash outlays over time or involve capital that will remain invested for extended periods of time. In the event that our liquidity requirements were to exceed available liquid assets for the reasons specified above or for any other reasons, there can be no assurance that we will be able to generate sufficient cash flows from realizations of investments to fund them, which could force us to sell assets or seek to raise debt or equity capital on unfavorable terms. For further discussion of our liquidity needs, see “Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources.”

12

Table of Contents

Our earnings and cash flow are highly variable due to the nature of our business and we do not intend to provide earnings guidance, each of which may cause the value of interests in our business to be volatile.

Our earnings are highly variable from quarter to quarter due to the volatility of investment returns of most of our funds, other investment vehicles and our balance sheet assets and the transaction and other fees earned from our businesses. We recognize earnings on investments in our funds based on our allocable share of realized and unrealized gains (or losses) reported by such funds and for certain of our recent funds, when a performance hurdle is achieved. During times of market volatility, the fair value of our funds and our balance sheet assets are more variable, and as publicly traded equity securities currently represent a proportion of the assets of many of our funds and balance sheet assets, volatility in the equity markets may have a significant impact on our reported results. A decline in realized or unrealized gains, a failure to achieve a performance hurdle or an increase in realized or unrealized losses, would adversely affect our profit for the period.

Net revenue from fund management, net revenue from performance fees and net revenue from advisory services, which we recognize when contractually earned, can vary due to fluctuations in AUM, the number of investment transactions made by our funds, the number of portfolio companies we manage, the fee provisions contained in our funds and other investment products and transactions by our advisory services. In any particular quarter, fee income may vary significantly due to the variances in size and frequency of management and performance fees, or fees received for our advisory services. We may create new funds or investment products or vary the terms of our funds or investment products (for example our funds now include performance hurdles), which may alter the composition or mix of our income from time to time.

We may also experience fluctuations in our results from quarter to quarter, including our net revenue from services rendered and profit for the period, due to a number of other factors, including changes in the values of our funds’ investments, changes in the amount of distributions or interest earned in respect of investments, changes in the number of completed transactions (such as merger and acquisition, or M&A, transactions and/or initial public offerings, or IPOs) for our financial advisory clients, changes in our operating expenses, the degree to which we encounter competition and general market and economic conditions. Such fluctuations may lead to variability in the value of interests in our business and cause our results for a particular period not to be indicative of our performance in future periods. It may be difficult for us to achieve steady growth in net income and cash flow on a quarterly basis, which could in turn lead to large adverse movements in the value of interests in our business.

We are entitled to receive performance fees when the return on assets under management, over a given period established in each fund’s private memorandum, exceeds certain return benchmarks or other performance benchmarks. The timing and receipt of performance fees from our investment funds are unpredictable and will contribute to the volatility of our cash flows. Performance fee payments from investments depend on our funds’ performance and opportunities for realizing gains, which may be limited. It takes a substantial period of time to identify attractive investment opportunities, to raise all the funds needed to make an investment and then to realize the cash value (or other proceeds) of an investment through a sale, public offering or other exit. To the extent an investment is not profitable, no performance fees will be received from our funds with respect to that investment and, to the extent such investment remains unprofitable, we will only be entitled to a management fee on that investment. Furthermore, certain vehicles and separately managed accounts may not provide for the payment of any performance fees at all. Even if an investment proves to be profitable, it may be several years before any profits can be realized in cash. Performance allocations and incentive fees could be significantly reduced as a result of our inability to maximize the value of investments by an investment fund during the liquidation process or in the event of the triggering of a “clawback” obligation. We cannot predict when, or if, any realization of investments will occur. In addition, if finance providers, such as commercial and investment banks, make it difficult for potential purchasers to secure financing to purchase companies in our investment funds’ portfolio, it may decrease potential realization events and the potential to earn performance fees. A downturn in the equity markets would also make it more difficult to exit investments by selling equity securities. If we were to have a realization event in a particular quarter, the event may have a significant impact on our cash flows during the quarter that may not be replicated in subsequent quarters. A decline in realized or unrealized gains, or an increase in realized or unrealized losses, would adversely affect our investment income, which could further increase the volatility of our quarterly results.

13

Table of Contents

The timing and receipt of performance fees also vary with the life cycle of certain of our funds. Our performance-paying funds that have completed their investment periods and are able to realize mature investments, sometimes referred to as being in a “harvesting period,” are more likely to make larger distributions than our performance-paying funds that are in their fundraising or investment periods that precede the harvesting period. During times when a significant portion of our AUM is attributable to performance-paying funds that are not in their harvesting periods, we may receive substantially lower performance fee distributions.

Our investment management activities may involve investments in relatively high-risk, illiquid assets, and we and our clients may lose some or all of the amounts invested in these activities or fail to realize any profits from these activities for a considerable period of time.

The investments made by our funds may include high-risk, illiquid assets. We have made and expect to continue to make investments alongside our investors, as the general partner, in our existing funds and certain customized separate accounts and in any new private markets funds we may establish in the future. The private markets funds in which we invest capital generally invest in securities that are not publicly traded. Even if such securities are publicly traded, many of these funds may be prohibited by contract or applicable securities laws from selling such securities for a period of time. Such funds will generally not be able to sell these securities publicly unless their sale is registered under applicable securities laws, or unless an exemption from such registration requirements is available. Accordingly, the private markets funds in which we invest our clients’ capital may not be able to sell securities when they desire and therefore may not be able to realize the full value of such securities. The ability of private markets funds to dispose of investments is dependent in part on the public equity and debt markets, to the extent that the ability to dispose of an investment may depend upon the ability to complete an IPO of the portfolio company in which such investment is held or the ability of a prospective buyer of the portfolio company to raise debt financing to fund its purchase. Furthermore, large holdings of publicly traded equity securities can often be disposed of only over a substantial period of time, exposing the investment returns to risks of downward movement in market prices during the disposition period. Contributing capital to these funds is risky, and we may lose some or the entire amount of our specialized funds and our clients’ investments.

The portfolio companies in which private markets funds have invested or may invest will sometimes involve a high degree of business and financial risk. These companies may be in an early stage of development, may not have a proven operating history, may be operating at a loss or have significant variations in operating results, may be engaged in a rapidly changing business with products subject to a substantial risk of obsolescence, may be subject to extensive regulatory oversight, may require substantial additional capital to support their operations, to finance expansion or to maintain their competitive position, may have a high level of leverage, or may otherwise have a weak financial condition.

In addition, these portfolio companies may face intense competition, including competition from companies with greater financial resources, more extensive development, manufacturing, marketing, and other capabilities, and a larger number of qualified managerial and technical personnel. Our portfolio companies may be subject to additional risks, including changes in currency exchange rates, exchange control regulations, risks associated with different types (and lower quality) of available information, expropriation or confiscatory taxation and adverse political developments, which risks may be exacerbated for any portfolio companies that may be organized in jurisdictions outside of Brazil. In addition, during periods of difficult market conditions or slowdowns in a particular investment category, industry or region, portfolio companies may experience decreased revenues, financial losses, difficulty in obtaining access to financing and increased costs. During these periods, these companies may also have difficulty in expanding their businesses and operations and may be unable to pay their expenses as they become due. A general market downturn or a specific market dislocation may result in lower investment returns for the private markets funds or portfolio companies in which our specialized funds and customized separate accounts invest, which consequently would materially and adversely affect investment returns for our specialized funds and customized separate accounts. Furthermore, if the portfolio companies default on their indebtedness, or otherwise seek or are forced to restructure their obligations or declare bankruptcy, we could lose some or all of our investment and also suffer reputational harm.

14

Table of Contents

We may pursue investment opportunities that involve business, regulatory, legal or other complexities.

We may pursue investment opportunities that have unusually complex business, regulatory and/or legal aspects to them. This complexity presents risks, as such transactions can be more difficult, expensive and time-consuming to finance and execute, it can be more difficult to manage or realize value from the assets acquired in such transactions and such transactions sometimes involve a higher level of regulatory scrutiny or a greater risk of contingent liabilities. Any of these risks could materially and adversely affect our business, financial condition and results of operations.

Our funds may face risks relating to undiversified investments.

While we have a policy of maintaining diversification in accordance with fund objectives and, where applicable, mandatory fund allocation rules, there can be no assurance as to the degree of diversification, if any, that will be achieved in any fund investments. Difficult market conditions or slowdowns affecting a particular asset class, geographic region or other category of investment could have a significant adverse impact on a given fund if its investments are concentrated in that area, which would result in lower investment returns. Accordingly, a lack of diversification on the part of a fund could adversely affect its investment performance and, as a result, our business, financial condition and results of operations.

Investments by our funds may in many cases rank junior to investments made by other investors.

In many cases, the companies in which our funds invest have indebtedness or equity securities, or may be permitted to incur indebtedness or to issue equity securities, that rank senior to our clients’ investments in our specialized funds, customized separate accounts or advisory accounts. By their terms, these instruments may provide that their holders are entitled to receive payments of dividends, interest or principal on or before the dates on which payments are to be made in respect of our clients’ investments. Also, in the event of bankruptcy or liquidation of a company in which one or more of our funds hold an investment, holders of securities ranking senior to our clients’ investments would typically be entitled to receive payment in full before distributions could be made in respect of our clients’ investments. After repaying senior security holders, the company may not have any remaining assets to use for repaying amounts owed in respect of our clients’ investments. To the extent that any assets remain, holders of claims that rank equally with our clients’ investments would be entitled to share on an equal and ratable basis in distributions that are made out of those assets. Also, during periods of financial distress or following an insolvency, our ability to influence a company’s affairs and to take actions to protect investments by our funds may be substantially less than that of those holding senior interests, which could adversely affect our business, financial condition and results of operations.

Our funds may be forced to dispose of investments at a disadvantageous time.

Our funds may make investments of which they do not advantageously dispose of prior to the date the applicable fund is dissolved, either by expiration of such fund’s term or otherwise. Although we generally expect that our funds will dispose of investments prior to dissolution or that investments will be suitable for in-kind distribution at dissolution, we may not be able to do so. We have only a limited ability to extend the term of the fund with the consent of fund investors or the advisory board of the fund, as applicable, and therefore, we may be required to sell, distribute or otherwise dispose of investments at a disadvantageous time prior to dissolution. This would result in a lower than expected return on the investments and, perhaps, on the fund itself.

A decline in the pace or size of investment by our funds would reduce the revenues we receive from fees.

The performance fees (including realized and unrealized performance fees) and management fees that we earn are driven in part by the pace at which our funds make investments and the size of those investments. Any decline in that pace or the size of investments would reduce our revenue from transaction and management fees. Likewise, during an attractive selling environment, our funds may capitalize on increased opportunities to exit investments. Any increase in the pace at which our funds exit investments, if not offset by new commitments and investments, would reduce future management fees. Additionally, in certain of our funds that derive management fees only on the basis of invested capital, the pace at which we make investments, the length of time we hold such investment and the timing of disposition will directly impact our revenues. Many factors could cause such a decline in the pace of investment or the transaction and management fees we receive, including:

| • | the inability of our investment professionals to identify attractive investment opportunities; |

| • | competition for such opportunities among other potential acquirers; |

15

Table of Contents

| • | unfavorable market and economic conditions; |

| • | decreased availability of capital on attractive terms; |

| • | our failure to consummate identified investment opportunities because of business, regulatory or legal complexities and adverse developments in the Brazilian or global economy or financial markets; |

| • | default by the investors of our investment funds on their contractual obligation to pay-in capital calls as requested by us or the third-party managers with whom we invest, impairing the ability to deploy capital at the intended rate; |

| • | terms we may agree with or provide to our fund investors or investors in separately managed accounts with respect to fees such as increasing the percentage of transaction or other fees we may share with our fund investors; and |

| • | new regulations, guidance or other actions provided or taken by regulatory authorities. |

Given our focus on achieving investment performance that exceeds the performance of our main competitors, and on maintaining and strengthening investor relations, we may reduce our AUM, restrain its growth, reduce our fees or otherwise alter the terms under which we do business when we deem it in the best interests of our investors—even in circumstances where such actions might be contrary to the near-term interests of holders of our Class A common shares.

From time to time if we decide it is in the best interests of all stakeholders, we may take actions that could reduce the profits we could otherwise realize in the short term. While we believe that our commitment to treating our investors fairly is in the long-term interest of us and our shareholders, we may take actions that could adversely impact our short-term profitability, and there is no guarantee that such actions will benefit us in the long term. The means by which we seek to achieve investment performance that exceeds the performance of our main competitors in each of our strategies could include limiting the AUM in our strategies to an amount that we believe can be invested appropriately in accordance with our investment philosophy and current or anticipated economic and market conditions. Additionally, we may voluntarily reduce management fee rates and terms for certain of our funds or strategies when we deem it appropriate, even when doing so may reduce our short-term revenue. For instance, in order to enhance our relationship with certain fund investors, we have reduced management fees or ceased charging management fees on certain funds in specific instances. In certain investment funds, we have agreed to charge management fees based on invested capital or net asset value as opposed to charging management fees based on committed capital.

We have increasingly undertaken business initiatives to increase the number and type of investment products we offer to retail investors, which could expose us to new and greater levels of risk.

Although retail investors have been part of our historic distribution efforts, we have increasingly undertaken business initiatives to increase the number and type of investment products we offer to high net worth individuals, family offices and other mass affluent investors. In some cases, we seek to distribute our funds to such retail investors indirectly through feeder funds sponsored by brokerage firms, private banks or third party feeder providers, and in other cases directly to the qualified clients of private banks, independent investment advisors and brokers. In other cases, we create investment funds specifically designed for direct investment by retail investors. Our initiatives to access retail investors entail the investment of resources and our objectives may not be fully realized.

Accessing retail investors and selling retail directed products exposes us to new and greater levels of risk, including heightened litigation and regulatory enforcement risks. To the extent we distribute retail products through new channels, including through unaffiliated firms such as digital distribution platforms, we may not be able to effectively monitor or control the manner of their distribution, which could result in litigation against us, including with respect to, among other things, claims that products distributed through such channels are distributed to customers for whom they are unsuitable or distributed in any other inappropriate manner. Although we seek to ensure through due diligence and onboarding procedures that the channels through which retail investors access our investment products conduct themselves responsibly, to the extent that our investment products are being distributed through third parties, we are exposed to reputation damage and possible legal liability to the extent such third parties

16

Table of Contents

improperly sell our products to investors. Similarly, the hiring of employees to oversee independent advisors and brokers presents risks if they fail to follow training, review and supervisory procedures. In addition, the distribution of retail products through new channels whether directly or through market intermediaries could expose us to additional regulatory risk in the form of allegations of improper conduct and/or actions by regulators against us with respect to, among other things, product suitability, conflicts of interest and the adequacy of disclosure to customers to whom our products are distributed through those channels.

Our inability to raise additional or successor funds (or raise successor funds of a size comparable to our predecessor funds) could have a material adverse impact on our business.

Our current private equity funds and certain other funds and investment vehicles have a finite life and a finite amount of commitments from fund investors. Once a fund nears the end of its investment period, our success depends on our ability to raise additional or successor funds in order to keep making investments and, over the long term, earning management fees (although our funds and investment vehicles continue to earn management fees after the expiration of their investment periods, they are generally at a reduced rate). Even if we are successful in raising successor funds, to the extent we are unable to raise successor funds of a size comparable to our predecessor funds or the extent that we are delayed in raising such successor funds, our revenues may decrease as the investment periods of our predecessor funds expire and associated fees decrease. The performance of our funds also impacts our ability to raise capital, and deterioration in the performance of our funds would result in challenges with regard to future fundraising. The evolving preferences of our fund investors may necessitate that alternatives to the traditional investment fund structure, such as separately managed accounts, smaller funds and co-investment vehicles, become a larger part of our business going forward. This could increase our cost of raising capital at the scale we have historically achieved. Furthermore, in order to raise capital for new strategies and products without drawing capital away from our existing products, we will need to seek new sources of capital such as individual investors.

Our ability to raise new funds could also be hampered if the general appeal of private equity and alternative investments were to decline. An investment in a limited partner interest in a private equity fund is less liquid than an exchange-traded instrument and the returns on such investment may be more volatile than returns on an investment in securities for which there is a more active and transparent market. Private equity and alternative investments could fall into disfavor as a result of concerns about liquidity and short-term performance. Institutional investors in private equity funds that have suffered from decreasing returns, liquidity pressure, increased volatility or difficulty maintaining target asset allocations may materially decrease or temporarily suspend making new investments in private equity funds. Such concerns could be exhibited, in particular, by public pension funds, which have historically been among the largest investors in alternative assets. Many public pension funds are significantly underfunded and their funding problems have been, and may in the future be, exacerbated by economic downturns. Concerns with liquidity could cause such public pension funds to reevaluate the appropriateness of alternative investments, and other institutional investors may reduce their overall portfolio allocations to alternative investments. This could result in a smaller overall pool of available capital in our industry. There is no assurance that the amount of commitments investors are making to alternative investment funds will continue at recent levels or that our ability to raise capital from investors will not be hampered.

In addition, the asset allocation rules or regulations or investment policies to which such third-party investors are subject could inhibit or restrict the ability of third-party investors to make investments in our investment funds. Coupled with a lack of distributions from their existing investment portfolios, many of these investors may have been left with disproportionately outsized remaining commitments to, and invested capital in, a number of investment funds, which may significantly limit their ability to make new commitments to third-party managed investment funds such as those advised by us.

Fund investors may also seek to redeploy capital away from certain of our credit or other non-private equity investment vehicles, which permit redemptions on relatively short notice in order for investors to meet liquidity needs or invest in other asset classes. We believe that our ability to avoid excessive redemption levels primarily depends on our funds’ continued satisfactory performance, although redemptions may also be driven by other factors important to our fund investors, including their need for liquidity and compliance with investment mandates, even if our performance is superior. Investors’ liquidity needs tend to be more pronounced during periods of market volatility. Any such redemptions would decrease our AUM and revenues.

17

Table of Contents

The number of funds raising capital varies from year to year, and in years where relatively few funds are raising capital, the growth of our AUM and associated fees may be significantly lower. There is no assurance that the raising of funds for new strategies or successor funds will experience success similar to our existing or predecessor funds in the future.

If we cannot make the necessary investments to keep pace with rapid developments and change in our industry, the use of our services could decline, reducing our revenues.

The financial services market in which we compete is subject to rapid and significant changes. This market is characterized by rapid technological change, new product and service introductions, evolving industry standards, changing client needs and the entrance of non-traditional competitors. In order to remain competitive and maintain and enhance customer experience and the quality of our services, we must continuously invest in projects to develop new products and features. These projects carry risks, such as cost overruns, delays in delivery, performance problems and lack of client adoption. There can be no assurance that we will have the funds available to maintain the levels of investment required to support our projects, and any delay in the delivery of new services or the failure to differentiate our services or to accurately predict and address market demand could render our services less desirable, or even obsolete, to our clients.