As filed with the Securities and Exchange Commission on April 28, 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number

Controladora Vuela Compañía de Aviación, S.A.B. de C.V. |

(Exact name of Registrant as specified in its charter) |

Volaris Aviation Holding Company |

(Translation of Registrant’s name into English) |

(Jurisdiction of incorporation or organization) |

(Address of principal executive offices) |

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

| ||||

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None |

(Title of Class) |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None |

(Title of Class) |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. | |

Ordinary Participation Certificates (Certificados de Participación Ordinarios): | |

Series A shares of common stock, no par value per share: | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Accelerated filer ☐ | Non-accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

TABLE OF CONTENTS

i

FORWARD-LOOKING STATEMENTS AND ASSOCIATED RISKS

This annual report on Form 20-F or our “annual report,” contains various forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which represent the Company’s expectations, beliefs or projections concerning future events and financial trends affecting the financial condition of our business. When used in this annual report, the words “expects,” “intends,” “estimates,” “predicts,” “plans,” “anticipates,” “indicates,” “believes,” “forecast,” “guidance,” “potential,” “outlook,” “may,” “continue,” “will,” “should,” “seeks,” “targets” and similar expressions are intended to identify forward-looking statements. Similarly, statements that describe the Company’s objectives, plans or goals, or actions the Company may take in the future, are forward-looking statements. Forward-looking statements include, without limitation, statements regarding the Company’s intentions and expectations regarding the delivery schedule of aircraft on order, announced new service routes and customer savings programs. Forward-looking statements should not be read as a guarantee or assurance of future performance or results and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time those statements are made and/or management’s good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Forward-looking statements are subject to a number of factors that could cause the Company’s actual results to differ materially from the Company’s expectations, including the competitive environment in the airline industry; the Company’s ability to keep costs low; changes in fuel costs; the impact of worldwide economic conditions on customer travel behavior; the Company’s ability to generate non-passenger revenues; and government regulation. Additional information concerning these, and other factors is contained in the Company’s Securities and Exchange Commission filings. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth above. Forward-looking statements speak only as of the date of this annual report. You should not put undue reliance on any forward-looking statements. We assume no obligation to update forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable law. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements. These risks and uncertainties include, but are not limited to, those described below under “Summary Risk Factors” and Part I, Item 3D. Risk Factors, Part I, Item 5. Operating and Financial Review and Prospects and other risks and uncertainties listed from time to time in our filings with the SEC. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this annual report may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements.

All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth above. Additionally, our discussion herein, particularly of ESG initiatives and related issues, are informed by various standards and frameworks (including standards for the measurement of underlying data) and the interests of various stakeholders, which may be more expansive than certain requirements under the federal securities laws. In particular, certain such information may not be “material” under the federal securities laws definition of materiality for SEC reporting purposes. Furthermore, much of this information is subject to assumptions, estimates, or third-party information that is still evolving and subject to change. For example, our disclosures may change due to revisions in framework requirements, availability of information, changes in our business or applicable government policies, changing stakeholder focus, or other factors, some of which may be beyond our control. Given the uncertainties, estimates, and assumptions involved, the materiality of some of this information is inherently difficult to assess far in advance. Forward-looking statements speak only as of the date of this annual report. You should not put undue reliance on any forward-looking statements. We assume no obligation to update forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable law. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

1

INTRODUCTION AND USE OF CERTAIN TERMS

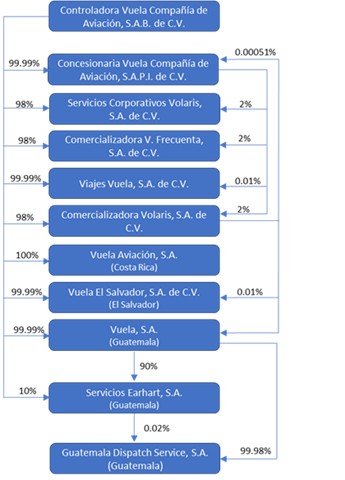

In this annual report, we use the term “Volaris” to refer to Controladora Vuela Compañía de Aviación, S.A.B. de C.V., “Volaris Opco” to refer to Concesionaria Vuela Compañía de Aviación, S.A.P.I. de C.V., “Comercializadora” to refer to Comercializadora Volaris, S.A. de C.V., “Servicios Corporativos” to refer to Servicios Corporativos Volaris, S.A. de C.V., “Servicios Administrativos” to refer to Servicios Administrativos Volaris, S.A. de C.V., “Servicios Earhart” to refer to Servicios Earhart, S.A., “Vuela” to refer to Vuela, S.A. and “Vuela Aviación” to refer to Vuela Aviación, S.A., “Viajes Vuela” to refer to Viajes Vuela, S.A. de C.V., “Comercializadora Frecuenta” to refer to Comercializadora V. Frecuenta, S.A. de C.V., “Vuela El Salvador” to refer to Vuela El Salvador, S.A. de C.V., and “GDS” to refer to Guatemala Dispatch Service, S.A., Volaris Opco, Comercializadora, Servicios Corporativos, Servicios Administrativos, Vuela, Vuela Aviación, Viajes Vuela, Comercializadora Frecuenta and Vuela El Salvador are wholly-owned subsidiaries of Volaris. The terms “we,” “our” and “us” in this annual report refer to Volaris, together with its subsidiaries, and to properties and assets that they own or operate, unless otherwise specified. References to “Series A shares” refer to Series A shares of Volaris.

2

SUMMARY OF RISK FACTORS

An investment in our securities and ADSs is subject to a number of risks, including risks related to Mexico, risks related to the countries in which we operate, risks related to the airline industry, risks related to our business, and risks related to our securities and the ADSs. The following list summarizes some, but not all, of these risks. Please read the information in the section entitled “Risk Factors” for a more thorough description of these and other risks.

Risks related to Mexico and the other countries in which we operate

| ● | Economic, political and social events and changes in Mexican government policy: The Mexican federal government has exercised, and continues to exercise, significant influence over the Mexican economy. As a result, governmental actions and policies concerning air transportation and similar services could have a significant impact on our operations. |

| ● | Adverse economic conditions in Mexico and the other countries in which we operate: Our business may be affected by unfavorable economic conditions in Mexico and the other countries in which we operate, including a slowdown or recession in the economy, as well as higher inflation rates. These factors may result in decreased demand for our flights, lower fares, or a shift towards alternative ground transportation options such as long-distance buses. |

| ● | Currency fluctuations: Fluctuations in the value of the U.S. dollar in relation to the peso have historically been significant, and the potential for such fluctuations to persist in the future remains. If the peso depreciates against the U.S. dollar, it could potentially lead to reduced demand for our services and adversely our business operations and financial performance. |

| ● | Developments in other countries: Changes in immigration or trade policies, can adversely affect our financial condition and results of operations. For example, changes in government regulations related to airline safety and security could increase our costs and decrease our profitability. In addition, shifts in political leadership and economic policies could impact the demand for our flights. |

| ● | Downgrade of IASA rating: The FAA regularly conducts audits of foreign aviation regulatory authorities and assigns an IASA rating to each country. In May 2021, Mexico’s IASA rating was downgraded from Category 1 to Category 2. Currently, the AFAC is taking steps to address the findings of the FAA. However, this downgrade has prevented us from adding new aircraft, services, or routes to the United States. If the IASA rating of Mexico is not upgraded in the future or if the IASA ratings of Mexico or the other Central and South American countries in which we operate were to be downgraded in the future, it could restrict our ability to maintain or increase service to the United States and incorporate aircraft registered in the United States into our fleet, which would in turn adversely affect our business, results of operations and financial condition. |

Risks related to the airline industry

| ● | Competition: We operate in an extremely competitive industry and face significant competition with respect to routes, fares, services, and airport slots. Our competition includes not only other airlines but also bus services on many of our routes. Decisions by our competitors that increase industry capacity, or capacity dedicated to a particular region, market, or route, have the potential to negatively impact our business. |

| ● | Economic Conditions: The airline industry is highly sensitive to changes in economic conditions. Unfavorable economic conditions have the potential to negatively impact our ability to offset increased fuel, labor, or other costs through price increases. Such impacts, if significant, may result in a material adverse effect on our business, financial condition, and results of operations. |

| ● | Regulations: The airline industry is highly regulated, and it is essential that we maintain the necessary concessions and authorizations from U.S., Mexican, Central American, and South American governmental bodies to operate successfully. Failure to do so could have a significant negative impact on our financial condition and results of operations. |

3

| ● | Fixed Costs: The airline industry is characterized by low gross profit margins and high fixed costs. As a result, as an airline we face significant challenges in quickly reducing costs in response to unexpected revenue shortfalls. This could have a material adverse effect on our financial condition and results of operations. |

| ● | Fuel Costs: Fuel costs have a significant impact on the airline industry, as it represents a considerable portion of operating expenses for airlines. Recent events, such as the conflict between Russia and Ukraine, have led to surging fuel prices and concerns about supply availability in global fuel markets. Our ability to pass on such fuel cost increases to our customers is limited by our ultra-low-cost business model. As a result, any significant fluctuations or disruptions in the supply of fuel could result in a material adverse effect on our business, financial condition, and results of operations. |

| ● | Public health threats: Infectious disease outbreaks, such as COVID-19 and other highly contagious diseases, have led to the suspension of both domestic and international flights in the past, as well as changes in travel behavior. These threats could also have a significant negative impact on the economies of the countries in which we operate, as well as the reputation of the airline industry as a whole. As a result, an infectious disease outbreak could have a material adverse effect on our business, results of operations, and financial condition. |

Risks related to our business

| ● | Ultra-Low-Cost Structure: Our competitive advantage lies in our ultra-low-cost structure, which is subject to various factors that may impact our ability to control costs, some of which are beyond our control. Our success relies on maintaining a high daily aircraft utilization rate, leaving us susceptible to flight delays, cancellations, and aircraft unavailability. Our non-passenger revenue is crucial for profitability, but it may not remain stable or increase. If our cost structure rises, and we can no longer maintain a cost advantage over competitors, it could negatively affect our business, results of operations, financial condition and prospects. |

| ● | Maintenance Costs: Our fleet has a relatively young average age of 5.4 years, as of December 31, 2022. Our newer aircraft, which constitute a significant portion of the fleet, presently require lower maintenance costs. However, as our fleet ages, we expect an increase in maintenance costs. Any significant surge in maintenance and repair expenses would have a material adverse effect on our margins, results of operations, and financial condition. |

| ● | Dependence on Certain Airports: Our business relies heavily on our routes to and from major airports in Mexico City, Tijuana, Guadalajara, and Cancun, which represent a significant portion of our overall routes. In addition, the Mexico City International Airport is at full capacity, and we cannot guarantee that we will be able to maintain or obtain additional slots. Any major increase in competition, loss of any of our slots, a decrease in demand for air travel, or disruptions in airport services or fuel supply could potentially have a negative impact on our business, financial condition, and operating results. |

| ● | Limited suppliers: We rely on a limited number of suppliers for fuel, aircraft, and engines. |

Risks related to our securities and the ADSs

| ● | CPO Trust: Non-Mexican investors may not hold our Series A shares directly and must have them held in a CPO trust, which releases CPOs underlying Series A shares, at all times. If the current trust is terminated, a new trust similar to the CPO trust may not be created. |

| ● | Voting Rights: Holders of the ADSs and CPOs are not entitled to vote the underlying Series A shares. As a result, holders of the ADSs and CPOs do not have any influence over the decisions made relating to our company’s business or operations, nor are they protected from the results of any such corporate action taken by our holders of Series A shares and Series B shares. |

4

GLOSSARY OF AIRLINES AND AIRLINE TERMS

Set forth below is a glossary of industry terms used in this annual report:

“Aeroméxico” | means Aerovías de México, S.A. de C.V. |

“AFAC” | means the Mexican Federal Civil Aviation Agency (Agencia Federal de Aviación Civil). |

“AirAsia” | means AirAsia Berhad. |

“Airbus” | means Airbus S.A.S. |

“Alaska” | means Alaska Air Group, Inc. |

“Allegiant” | means Allegiant Travel Company. |

“Aeroméxico Connect” | means Aerolitoral, S.A. de C.V. |

“American” | means American Airlines Group. |

“Available seat miles” or “ASMs” | means the number of seats available for passengers multiplied by the number of miles the seats are flown. |

“Average daily aircraft utilization” | means flight hours or block hours, as applicable, divided by number of days in the period divided by average aircraft in the period. |

“Average economic fuel cost per gallon” | means total fuel expense net of hedging effect, divided by the total number of fuel gallons consumed. |

“Average passenger revenue per booked passenger” | means total passenger revenue divided by booked passengers. |

“Average stage length” | means the average number of miles flown per passenger flight segment. |

“Avianca” | means Avianca Holdings S.A. |

“Azul” | means Azul Linhas Aéreas Brasileiras S.A. |

“Block hours” | means the number of hours during which the aircraft is in revenue service, measured from the time it leaves the gate until the time it arrives to the gate at destination. |

“Booked passengers” | means the total number of passengers booked on all flight segments. |

“CASM” or “unit costs” | means total operating expenses, net divided by ASMs. |

“CASM ex fuel” | means total operating expenses, net excluding fuel expenses divided by ASMs. |

“CBP” | means U.S. Customs and Border Protection. |

“CEO” | means current engine option. |

“Copa” | means Copa Holdings, S.A. |

“Delta” | means Delta Air Lines, Inc. |

“DHS” | means the U.S. Department of Homeland Security. |

5

“DOT” | means the U.S. Department of Transportation. |

“EPA” | means the U.S. Environmental Protection Agency. |

“ESG” | means Environmental, Social and Governance matters. |

“FAA” | means the U.S. Federal Aviation Administration. |

“FCC” | means the U.S. Federal Communications Commission. |

“Flight hours” | means the number of hours during which the aircraft is in revenue service, measured from the time it takes off until the time it lands at the destination. |

“Frontier” | means Frontier Airlines, Inc. |

“Gol” | means Gol Linhas Aéreas Inteligentes, S.A. |

“Grupo Aeroméxico” | means Grupo Aeroméxico, S.A.B. de C.V., which includes Aeroméxico and Aeroméxico Connect. |

“Grupo Mexicana” | means Grupo Mexicana de Aviación, S.A. de C.V., which is the holding company for three airlines, Compañía Mexicana de Aviación, Mexicana Click and Mexicana Link. |

“Grupo TACA” | means Taca International Airlines, S.A. |

“IASA” | means International Aviation Safety Assessment. |

“IATA” | means the International Air Transport Association. |

“INEGI” | means the Mexican Institute of Statistics and Geography (Instituto Nacional de Estadística y Geografía). |

“Interjet” | means ABC Aerolíneas, S.A. de C.V. |

“JetSMART” | means JetSMART Airlines SpA. |

“LATAM” | means LATAM Airlines Group S.A. |

“Latin America” | means, collectively, Mexico, the Caribbean, Central America and South America. |

“Latin American publicly traded airline carriers” | means, collectively, Azul, Copa and Gol. |

“Legacy carrier” | means an airline that typically offers scheduled flights to major domestic and international routes (directly or through membership in an alliance) and serves numerous smaller cities, operates mainly through a “hub-and-spoke” network route system and has higher cost structures than low-cost carriers due to higher labor costs, flight crew and aircraft scheduling inefficiencies, concentration of operations in higher cost airports and multiple classes of services. |

“LMV” | means the Mexican Securities Market Law (Ley del Mercado de Valores). |

“Load factor” | means RPMs divided by ASMs and expressed as a percentage. |

6

“Low-cost carrier” | means an airline that typically flies direct, point-to-point flights, often serves major markets through secondary, lower cost airports in the same regions as major population centers, provides a single class of service, thereby increasing the number of seats on each flight and avoiding the significant and incremental cost of offering premium-class services, and tends to operate fleets with only one or two aircraft families, in order to maximize the utilization of flight crews across the fleet, improve aircraft scheduling efficiency and flexibility and minimize inventory and aircraft maintenance costs. |

“NEO” | means new engine option. |

“NYSE” | means the New York Stock Exchange. |

“On-time” | means flights arriving within 15 minutes of the scheduled arrival time. |

“Other Latin American publicly traded airlines” | means, collectively, Azul, Copa, and Gol. |

“Passenger flight segments” | means the total number of passengers flown on all flight segments. |

“RASM” | means passenger revenue divided by ASMs. |

“RNV” | means the Securities National Registry (Registro Nacional de Valores). |

“Revenue passenger miles” or “RPMs” | means the number of seats sold to passengers divided by the number of miles the seats are flown. |

“Ryanair” | means Ryanair Holdings plc. |

“SICT” | means the Mexican Infrastructure, Communications and Transportation Ministry (Secretaría de Infraestructura, Comunicaciones y Transportes). |

“Southwest” | means Southwest Airlines Co. |

“Spirit” | means Spirit Airlines, Inc. |

“Tiger” | means Tiger Airways Holdings Limited. |

“Total operating revenue per ASM” or “TRASM” | means total revenue divided by ASMs. |

“TSA” | means the U.S. Transportation Security Administration. |

“ULCC” | means an airline that belongs to a subset of low-cost carriers, which distinguishes itself by using a business model with an intense focus on low-cost, efficient asset utilization, unbundled revenue sources aside from the base fares with multiple products and services offered for additional fees. In the United States, Frontier, and Spirit Airlines, Inc. define themselves as ULCCs and Volaris and VivaAerobus follow the ULCC model in Mexico. |

“United” | means United Airlines Holdings, Inc. |

“U.S.-based publicly traded target market competitors” | means Alaska, Allegiant, American, Delta, Frontier, Spirit, JetBlue, Southwest and United. |

“VFR” | means passengers who are visiting friends and relatives. |

“VivaAerobus” | means Aeroenlaces Nacionales, S.A. de C.V. |

“Wizz” | means Wizz Air Holdings Plc. |

7

PRESENTATION OF FINANCIAL INFORMATION AND OTHER INFORMATION

This annual report includes our audited consolidated financial statements at January 1, 2021, December 31, 2021 and 2022, and for each of the three years ended December 31, 2020, 2021 and 2022, which have been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. These audited consolidated financial statements are included elsewhere in this annual report. Unless otherwise specified and for presentation purposes of this annual report all references to December 31, 2020, relate to the audited consolidated statements of financial position as of January 1, 2021.

Unless otherwise specified, all references to “U.S. dollars,” “dollars,” “U.S. $” or “$” are to United States dollars, the legal currency of the United States, and references to “Mexican pesos,” “pesos” or “Ps.” Are to Mexican Pesos, the legal currency of Mexico. Amounts presented in this annual report may not add up due to rounding.

Effective January 1, 2022, and for all subsequent periods, as permitted by IFRS international Accounting Standard 21 “The effects of changes in Foreign Exchange Rates,” or IAS 21, and with the authorization of our board of directors, considering the favorable opinion of audit and corporate governance committee, we determined that our presentation currency had changed from Mexican peso to the U.S. dollar.

The change in presentation currency was applied retrospectively. All periods presented on our consolidated financial statements have been re-presented into the U.S. dollar. We believe the change in presentation currency accurately reflects our financial performance aligned to the economic environment in which we operate. We believe that the change in presentation currency provides our investors and other stakeholders with greater comparability of our financial information with our industry peers. The use of the U.S. dollar as presentation currency will also improve the comparison of our consolidated financial statements with those of other global entities. See Note 1 to our consolidated financial statements included elsewhere in this annual report.

As of December 31, 2021, and for all subsequent periods, as permitted by IAS 21 and with the authorization of our board of directors, after considering the favorable opinion of our audit and corporate governance committee, we determined that our functional currency had changed from the Mexican peso to the U.S. dollar.

During the second half of 2021, we identified in the primary economic environment in which Volaris Opco operates (i) an increase in Volaris Opco’s international market transactions during 2021, (ii) changes in the determination of rates and (iii) that most of Volaris Opco’s representative costs are determined and denominated in U.S. dollars. As a result, we evaluated the functional currency of Volaris Opco in accordance with the regulatory provisions contained in IAS 21 and determined that Volaris Opco’s functional currency changed from the Mexican peso to the U.S. dollar as of December 31, 2021.

In addition, considering the dependency of our operations on Volaris Opco, our management determined that our functional currency also changed from the Mexican peso to the U.S. dollar as of December 31, 2021.

As of December 31, 2022, the presentation currency of our consolidated financial statements, including comparative amounts and the accompanying notes is the U.S. dollar. The consolidated financial statements are presented as if the new presentation currency had always been our presentation currency. The comparative financial statements and their related notes were re-presented for the change in presentation currency by applying the methodology set out in IAS 21. All amounts disclosed in this annual report are presented in U.S. dollars, which may not be comparable with the information presented in our annual report for the year ended December 31, 2021.

Industry and Market Data

We obtained the industry and market data used in this annual report from research, surveys or studies conducted by third parties on our behalf, information contained in third-party publications, such as the INEGI, reports from the AFAC, reports from the Mexican Central Bank and other publicly available sources. Third-party publications generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. Although we believe that this data and information is reliable, we have not independently verified it. Additionally, certain market share data is based on published information available for the Mexican states. There is no comparable data available relating to the particular cities we serve. In presenting market share estimates for these cities, we have estimated the size of the market on the basis of the published information for the state in which the particular city is located. We believe this method is reasonable, but the results have not been verified by any independent source.

8

PART I.

ITEM 1 IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2 OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3 KEY INFORMATION

| A. | Selected Consolidated Financial Data |

SELECTED CONSOLIDATED FINANCIAL INFORMATION AND OPERATING DATA

The following tables summarize selected financial and operating data for our business for the periods presented. You should read this selected consolidated financial data in conjunction with Item 5: “Operating and Financial Review and Prospects” and our audited consolidated financial statements, including the related notes thereto, all included elsewhere in this annual report. We prepare our consolidated financial statements in accordance with IFRS.

9

We derived the selected consolidated statements of operations data for the years ended December 31, 2020, 2021 and 2022, and the selected consolidated statements of financial position data as of January 1, 2021 and December 31, 2021 and 2022, from our audited financial statements included in this annual report. See Item 18: “Financial Statements.” Our historical results are not necessarily indicative of the results to be expected in the future.

For the Years ended December 31, |

| ||||||

| 2020 (1) |

| 2021 (1) |

| 2022 |

| |

(in thousand of dollars) |

| ||||||

CONSOLIDATED STATEMENTS OF OPERATIONS DATA |

| ||||||

Operating revenues: | |||||||

Passenger revenues: |

|

|

| ||||

Fare revenues | 626,909 |

| 1,265,980 |

| 1,661,176 | ||

Other passenger revenues | 415,997 | 866,944 | 1,078,251 | ||||

Non-passenger revenues: | |||||||

Other non-passenger revenues | 41,841 | 76,872 | 92,977 | ||||

Cargo | 9,647 | 11,882 | 14,786 | ||||

Non-derivative financial instruments | (19,408) | (21,378) | — | ||||

| 1,074,986 |

| 2,200,300 | 2,847,190 | |||

Other operating income |

| (33,619) |

| (10,758) |

| (25,066) | |

Fuel expense, net | 321,541 |

| 609,390 |

| 1,299,254 | ||

Landing, take-off and navigation expenses | 195,989 |

| 296,831 |

| 379,108 | ||

Depreciation of right of use assets | 236,417 |

| 269,351 |

| 320,443 | ||

Salaries and benefits | 163,776 |

| 239,215 |

| 283,089 | ||

Aircraft and engine variable lease expenses | 85,957 | 83,373 | 124,532 | ||||

Sales, marketing and distribution expenses | 86,705 |

| 96,705 |

| 124,287 | ||

Other operating expenses | 54,413 | 65,858 | 102,585 | ||||

Maintenance expenses (2) | 55,227 |

| 96,256 |

| 97,783 | ||

Depreciation and amortization (3) | 42,098 |

| 57,049 |

| 97,486 | ||

1,208,504 | 1,803,270 | 2,803,501 | |||||

Operating (loss) income | (133,518) |

| 397,030 |

| 43,689 | ||

Finance income | 4,784 |

| 3,531 |

| 12,902 | ||

Finance cost | (138,320) |

| (139,374) |

| (192,535) | ||

Foreign exchange gain (loss), net | 13,601 |

| (124,161) |

| 3,581 | ||

(Loss) income before income tax | (253,453) |

| 137,026 |

| (132,363) | ||

Income tax benefit (expense) | 61,731 |

| (30,573) |

| 52,139 | ||

Net (loss) income | (191,722) |

| 106,453 |

| (80,224) | ||

Weighted average shares outstanding: | |||||||

Basic | 1,004,964,804 |

| 1,152,256,138 |

| 1,155,029,942 | ||

Diluted | 1,021,286,357 |

| 1,165,612,152 |

| 1,165,135,294 | ||

(Loss) earnings per share Basic (4) | (0.19) | 0.09 | (0.07) | ||||

(Loss) earnings per share Diluted (4) | (0.19) | 0.09 | (0.07) | ||||

(Loss) earnings per ADS Basic (5) | (1.91) |

| 0.92 |

| (0.69) | ||

(Loss) earnings per ADS Diluted (5) | (1.88) | 0.91 | (0.69) | ||||

CONSOLIDATED STATEMENT OF FINANCIAL POSITION DATA |

|

| |||||

Cash, cash equivalents and restricted cash (11) | 506,468 | 741,122 | 711,853 | ||||

Accounts receivable, net (11) | 101,630 |

| 106,084 |

| 240,126 | ||

Guarantee deposits-current portion (11) | 57,245 | 78,990 | 64,357 | ||||

Total current assets (11) | 721,968 |

| 978,980 |

| 1,066,078 | ||

Total assets (11) | 3,418,223 | 3,984,568 | 4,467,653 | ||||

Total current liabilities (11) | 1,050,994 |

| 1,251,534 |

| 1,419,740 | ||

Total non-current liabilities (11) | 2,227,061 |

| 2,419,897 |

| 2,813,176 | ||

Total liabilities (11) | 3,278,055 | 3,671,431 | 4,232,916 | ||||

Capital stock (11) | 248,278 |

| 248,278 |

| 248,278 | ||

Total equity (11) | 140,168 |

| 313,137 |

| 234,737 | ||

CASH FLOW DATA |

|

| |||||

Net cash flows provided by operating activities | 213,749 |

| 785,356 |

| 613,602 | ||

Net cash flow used in investing activities | (3,152) |

| (134,645) |

| (130,694) | ||

Net cash flow used in financing activities | (129,568) |

| (435,184) |

| (513,088) | ||

OPERATING DATA (8) (9) | |||||||

Aircraft at end of period | 86 | 101 |

| 117 | |||

Average daily aircraft utilization (block hours) | 11.30 | 12.53 | 13.28 | ||||

Average daily aircraft utilization (flight hours) | 9.73 | 10.77 |

| 11.29 | |||

Average pesos/U.S. dollar exchange rate | 21.50 | 20.28 |

| 20.12 | |||

End of period pesos/U.S. dollar exchange rate | 19.95 | 20.58 |

| 19.36 | |||

Airports served at end of period | 68 | 69 | 72 | ||||

Departures (6) | 97,819 | 153,913 |

| 193,050 | |||

Passenger flight segments (thousands) (6) | 13,153 | 22,560 |

| 29,064 | |||

Booked passengers (thousands) (6) | 14,712 | 24,405 |

| 31,051 | |||

Revenue passenger miles (RPMs) (thousands) (6) | 14,596,745 | 23,802,381 | 30,191,210 | ||||

Available seat miles (ASMs) (thousands) (6) | 18,274,946 | 28,096,701 |

| 35,280,830 | |||

Load factor (7) | 80 | % | 85 | % | 86 | % | |

Average fare revenue per booked passenger (7) | 43 | 52 | 54 | ||||

Average other passenger revenue per booked passenger (6) (8) | 28 | 36 |

| 35 | |||

Total ancillary revenue per booked passenger (6) (8) | 32 |

| 39 |

| 38 | ||

Total operating revenue per ASM (TRASM) (cents) (6) (8) | 6.0 |

| 7.9 |

| 8.1 | ||

Passenger revenue per ASM (RASM) (cents) (6) (8) | 3.4 |

| 4.5 |

| 4.7 | ||

Operating expenses per ASM (CASM) (cents) (6) (8) | 6.7 |

| 6.4 |

| 7.9 | ||

CASM ex fuel (cents) (6) (8) | 4.8 |

| 4.2 |

| 4.3 | ||

Fuel gallons consumed (thousands) | 176,645 |

| 273,515 |

| 340,053 | ||

Average economic fuel cost per gallon (8) | 39.9 |

| 45.9 | 75.0 | |||

Average of employees per aircraft at end of period (12) | 54 |

| 63 |

| 60 | ||

10

| (1) | Effective January 1, 2022, we changed our presentation currency from the Mexican peso to the U.S. dollar. The change in presentation currency was applied retrospectively effective January 1, 2020. All periods presented on our consolidated financial statements have been re-presented into the U.S. dollar. |

| (2) | Includes routine and ordinary maintenance expenses only. See Item 5: “Operating and Financial Review and Prospects—Operating Results.” |

| (3) | Includes, among other things, major maintenance expenses, which are capitalized and subsequently amortized. See Item 5: “Operating and Financial Review and Prospects—Operating Results.” |

| (4) | Basic and diluted earnings per share amounts are calculated by dividing the net (loss), income, for the year attributable to ordinary equity holders of the parent by the weighted average number of ordinary shares in accordance with IAS 33 “Earnings per share.” |

| (5) | The basis used for the computation of the information is to multiply the earnings per basic and diluted share obtained pursuant to footnote (4) above by ten, which is the number of CPOs represented by each ADS. Each CPO, in turn, represents a financial interest in one Series A share of common stock of Volaris. |

| (6) | Includes scheduled and charter. |

| (7) | Includes scheduled. |

| (8) | Excludes non-derivative financial instruments. |

| (9) | See “Glossary of Airlines and Airline Terms” elsewhere in this annual report for definitions of terms used in this table. |

| (10) | See detail of other current assets in Item 17: “Financial Statements”. |

| (11) | The consolidated statement of financial position as of December 31, 2020, relates to the balances as of January 1, 2021, included in our consolidated financial statements included elsewhere in this annual report. |

| (12) | Traffic agents are considered on a 60% FTE (Full-Time Equivalent) basis for this calculation, as they are part-time employees. |

A. | Key Performance Indicators |

The following measures are often provided, and utilized by our management, analysts, and investors to enhance comparability of year-over-year results, as well as to compare results to other airlines: Revenue passenger miles, or RPMs; Average passenger revenue per booked passenger; Average non-passenger revenue per booked passenger, Total operating revenue per ASM, or TRASM; Passenger Revenue per ASMS, or RASM; Operating expenses per ASM, or CASM; CASM ex fuel, and average economic fuel cost per gallon. Average passenger revenue per booked passenger represents the total passenger revenue divided by booked passengers. The CASM ex fuel represents total operating expenses, net excluding fuel expense divided by ASMs. Average economic fuel cost per gallon represents total fuel expense net of hedging effect, divided by the total number of fuel gallons consumed. We believe this operating data is useful in reporting the operating performance of our business, however, these measures may differ from similarly titled measures reported by other companies and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS.

B. | Capitalization and Indebtedness |

Not Applicable.

C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

D. | Risk Factors |

You should carefully consider all of the information set forth in this annual report and the risks described below before making an investment decision. Our business, results of operations and financial condition could be materially and adversely affected by any of these risks. The trading price of the ADSs could decline due to any of these risks or other factors, and you may lose all or part of your investment.

11

The risks described below are those that we currently believe may adversely affect us or the ADSs. In general, investing in the securities of issuers in emerging market countries, such as Mexico, involves risks that are different from the risks associated with investing in the securities of U.S. companies and companies located in other countries with developed capital markets. Any of these risks could materially and adversely affect our business and results of operations.

To the extent that information relates to, or is obtained from sources related to, the Mexican government or Mexican macroeconomic data, the following information has been extracted from official publications of the Mexican government and has not been independently verified by us.

Risks related to Mexico and the other countries in which we operate

Economic political and social developments in Mexico as well as changes in Mexican federal governmental policies may have an adverse effect on our business, results of operations, financial condition and prospects.

Our business, results of operations and financial condition are affected by economic, political or social developments in Mexico, including, among others, any political or social instability in Mexico, changes in the rate of economic growth or contraction, changes in the exchange rate between the peso and the U.S. dollar, an increase in inflation or interest rates, changes in Mexican taxation and any amendments to existing Mexican laws, federal governmental policies and regulations.

Adverse social or political developments in or affecting Mexico could negatively affect us and Mexican financial markets generally, thereby affecting our ability to obtain financing. Presidential and federal congressional elections in Mexico were held on July 1, 2018. Mr. Andrés Manuel López Obrador, a member of the National Regeneration Movement (Movimiento Regeneración Nacional), was elected President of Mexico and took office on December 1, 2018. The President’s party and its allies currently hold the majority of the Chamber of Deputies and the Senate. We cannot provide any assurance that the current political situation or any future developments in Mexico will not have a material adverse effect on our business, results of operations, financial condition, or prospects.

In addition, the Mexican federal government has exercised, and continues to exercise, significant influence over the Mexican economy. In particular, Mexican governmental actions and policies concerning air transportation and similar services could have a significant impact on us. In 2022, the Mexican government implemented subsidies to offset the sharp increase in oil prices, specifically for diesel, which is the primary fuel used in buses and goods transportation. These subsidies are not applicable to jet fuel. As a result, the subsidies benefit the bus market, but do not provide any benefit to us or the airline industry.

In December 2022, President Andrés Manuel López Obrador announced plans to create a new airline owned and operated by the Mexican government, to that effect in April 2023, the Chamber of Deputies approved amendments to the Mexican Civil Aviation Law (Ley de Aviación Civil) and Mexican Airports Law (Ley de Aeropuertos) that, among other things, would allow governmental entities to have concessions to operate both, civil airlines and airports. Such proposals, if adopted, would further increase our competition. On February 2, 2023, the Mexican federal governmental published a decree ordering the termination of domestic and international air cargo transport operations, both regularly scheduled and unscheduled flights, at the Mexico City International Airport.

We cannot assure you that changes in Mexican laws, regulations and policies, including those recently adopted, currently proposed and any changes that may be adopted in the future, will not adversely affect our business, results of operations, financial condition and prospects or the price of the ADSs.

Adverse economic conditions in Mexico and the other countries in which we operate may adversely affect our business, results of operations and financial condition.

We are a Mexican corporation and most of our operations are conducted in Mexico. For the year ended December 31, 2022, 67% of our total revenues were attributable to our Mexican domestic operations. As a result, our business is affected by the performance of the Mexican economy. In 2020, 2021 and 2022, the Mexican economy contracted 8.4%, grew 5.1% and grew 3.1%, respectively, in terms of gross domestic product, or GDP, according to the INEGI. Moreover, in the past, Mexico has experienced prolonged periods of economic crises, caused by internal and external factors, over which we have no control. Those periods have been characterized by exchange rate instability, high inflation, high domestic interest rates, economic contraction, a reduction of international capital flows, a reduction of liquidity in the banking sector and high unemployment rates.

12

We conduct an important part of our operations in the United States and Central and South America. For the year ended December 31, 2022, 33% of our total revenues were attributable to our operations in the United States and Central and South America. As a result, our results are not only dependent of our domestic operations, but they are also affected by the ones in the United States and Central and South America.

As of the date of this annual report, we believe that the main risk factors for the countries where we operate include, but are not limited to, the following: (i) continuation of persistent supply-demand mismatches, increasing inflation and a faster-than-anticipated monetary policy normalization cycle, and its impact on the global economy, emerging markets, risk aversion, foreign exchange markets, debt, and financial market volatility; (ii) escalation of social unrest; (iii) more adverse climate shocks; (iv) an escalation of trade and technology tensions, notably between the United States and China, could weigh on investment and productivity growth, raising additional roadblocks in the recovery path; (v) rapid growth of cryptocurrencies without clear regulation that could lead to financial instability with negative effects for the global economy; (vi) an increase in the spread and destructiveness of cyberattacks involving critical infrastructure could act as further drags on the recovery, particularly as telework and automation increase; and (vii) other geopolitical risks.

Unfavorable economic conditions in Mexico and the other countries in which we operate, including a slowdown or recession in their economies, as well as higher inflation rates, may result in decreased demand for our flights, lower fares or a shift towards alternative ground transportation options, such as long-distance buses. We cannot assure you that economic conditions in Mexico and the other countries in which we operate will not worsen, or that those conditions will not have an adverse effect on our business, results of operations and financial condition.

Economic, political, or social developments in the United States and the Central and South American countries in which we operate may have an adverse effect on our business, results of operations, financial condition and prospects.

Our business, results of operations and financial condition are affected by economic, political or social developments in the United States and the Central and South American countries in which we operate. Like other companies with international operations, political, economic, geopolitical or social developments in the countries in which we operate, such as elections, new governments, changes in public policy, economic circumstances, laws and/or regulations, trade policies, political agreements or disagreements, civil disturbances and a rise in violence or the perception of violence, could have a material adverse effect in the countries in which we operate or on the global financial markets, and in turn on our business, results of operations, financial condition and prospects.

If inflation rates increase in Mexico and the other countries in which we operate, demand for our services may decrease and our costs may increase.

Mexico has historically experienced levels of inflation that are higher than the annual inflation rates of its main trading partners. The annual rate of inflation, as measured by changes in the Mexican national consumer price index, calculated and published by the Mexican Central Bank and INEGI was 3.15% for 2020, 7.36% for 2021 and 7.82% for 2022. In addition, since the beginning of 2021, inflation, as measured by the consumer price index has increased in advanced and emerging market economies, reaching 40-year record high in the United States, driven mainly by supply chain issues (including input shortages, labor constrains, and rising commodity prices), excess demand for goods and services, and significant increases in energy prices. High inflation rates could adversely affect our business and results of operations by reducing consumer purchasing power, thereby adversely affecting consumer demand for our services, increasing our costs beyond levels that we could pass on to our customers and by decreasing the benefit to us of revenues earned to the extent that inflation exceeds growth in our pricing levels.

13

Currency fluctuations or the devaluation and depreciation of the U.S. dollar could adversely affect our business, results of operations, financial condition and prospects.

Foreign exchange gains or losses included in our total cost of comprehensive financing resulted primarily from the impact of changes in the US dollar-peso exchange rate on our Mexican peso-denominated monetary liabilities (such as Mexican peso-denominated debt, Mexican pesos financial debt, suppliers and other accounts payable) and assets (such Mexican peso-denominated cash, cash equivalents, accounts receivable, guarantee deposits and derivative financial instruments denominated in Mexican pesos). As of December 31, 2020 and 2021, our net monetary liability position denominated in U.S. dollars was U.S. $1.7 billion and U.S. $1.6 billion, respectively. As of December 31, 2022, our net monetary Mexican peso and other currencies liability position denominated in U.S. dollars was U.S. $0.2 billion. As a result of either the appreciation or depreciation of the peso against the U.S. dollar in 2020, 2021, and 2022, and our net U.S. dollar liability position, we recorded a foreign exchange gain (loss), net of U.S. $13.6 million, U.S. $(124.2) million and U.S. $(3.6) million, respectively.

The value of the U.S. dollar has been subject to significant fluctuations with respect to the peso in the past and may be subject to significant fluctuations in the future. This trend in fluctuations has continued as the U.S. dollar appreciated 5.8% in 2020 against the peso in nominal terms. As of December 31, 2021 and 2022, the U.S. dollar appreciated 3.2% and depreciated 5.9%, respectively, against the peso in nominal terms since December 31, 2020.

During the second half of 2021 , we identified in the primary economic environment in which our main subsidiary Volaris Opco operates (i) an increase in its international market transactions during 2021, (ii) a change in the determination of rates, and (iii) that most of Volaris Opco’s representative costs are determined and denominated in U.S. dollars. As a result, management determined that the functional currency of Volaris Opco had changed from Mexican peso to the U.S. dollar as of December 31, 2021.

Furthermore, after considering our dependency on our subsidiary Volaris Opco, management determined that our functional currency also changed from Mexican peso to U.S. dollar as of December 31, 2021. Effective January 1, 2022, and for all subsequent periods, as permitted by IAS 21, and with the authorization of our board of directors, after considering the favorable opinion of our audit and corporate governance committee, we changed our presentation currency from Mexican peso to the U.S. dollar.

A change in presentation currency is a change in accounting policy which is accounted for retrospectively. In making this change in presentation currency, the Company followed the requirements set out in IAS 21 “The Effect of Changes in Foreign Exchanges Rates.”

Devaluation or depreciation of the peso against the U.S. dollar may adversely affect the U.S. dollar value of an investment in the ADSs, as well as the U.S. dollar value of any dividend or other distributions that we may make.

Fluctuations in the exchange rate between the peso and the U.S. dollar, particularly depreciations in the value of the peso, may adversely affect the U.S. dollar equivalent of the peso price of the Series A shares on the Mexican Stock Exchange. Such peso depreciations will likely affect the market price of the ADSs. Exchange rate fluctuations would also affect the U.S. dollar equivalent value of any dividends and other distributions we may elect to make in the future and may affect the timely payment of any peso cash dividends and other distributions to holders of CPOs that we may elect to pay in the future.

Developments in other countries could adversely affect the Mexican economy, the market value of our securities, our financial condition and results of operations.

The market value of securities of Mexican companies is affected by economic and market conditions in developed and other emerging market countries. Although economic conditions in those countries may differ significantly from economic conditions in Mexico, investors’ reactions to developments in any of these other countries, may have an adverse effect on the market value of securities of Mexican issuers. In recent years, for example, prices of both Mexican debt and equity securities have sometimes suffered substantial drops as a result of developments in other countries. In 2008-2009, credit issues in the United States related principally to the sale of sub-prime mortgages resulted in significant fluctuations in securities traded in global financial markets, including Mexico.

14

In addition, the direct correlation between economic conditions in Mexico and the United States has strengthened in recent years because of the North American Free Trade Agreement, or NAFTA, and increased economic activity between the two countries (including increased remittances of U.S. dollars from Mexican workers in the United States to their families in Mexico). On November 30, 2018, Mexico, the United States and Canada signed the USMCA (United States-Mexico-Canada Agreement), which entered into force on July 1, 2020, as a replacement for NAFTA. During his presidency, President Trump implemented immigration policies that have adversely affected United States—Mexico travel behavior, especially in the VFR and leisure markets. President Trump’s immigration policies had a negative impact on our results of operations. In addition, as a result of the COVID-19 pandemic, on April 22, 2020, President Trump signed a Presidential Proclamation entitled: “Suspending Entry of Immigrants Who Present Risk to the U.S. Labor Market During the Economic Recovery Following the COVID-19 Outbreak.” On January 20, 2021, Joseph Biden became the President of the United States. While President Biden reversed many of President Trump’s immigration policies, we can offer no assurance of the extent to which his administration will continue to do so. In addition, even if President Biden continues to reverse President Trump’s immigration policies, subsequent presidential administrations could reimpose them, which could have a material adverse effect on our operations and revenues and affect the market price of our securities, including the ADSs.

Mexican antitrust provisions may affect the fares we are permitted to charge to customers.

The Mexican Aviation Law (Ley de Aviación Civil) provides that in the event that the SICT determines that there is no effective competition among permit and concession holders (required to operate airlines in Mexico), the SICT may request the opinion of the Mexican Antitrust Commission (Comisión Federal de Competencia Económica) and then issue regulations governing the fares that may be charged for air transportation services by airlines operating in Mexico. Such regulations would be in effect only while the conditions that resulted in their establishment remain. The imposition of fare regulations by the SICT could materially affect our business, results of operations and financial condition.

Violent crime in Mexico has adversely impacted, and may continue to adversely impact, the Mexican economy and may have a negative effect on our business, results of operations or financial condition.

Mexico has experienced high levels of violent crime over the past few years relating to illegal drug trafficking, particularly in Mexico’s northern states near the U.S. border. This violence has had an adverse impact on the economic activity in Mexico. In addition, violent crime may further affect travel within Mexico and between Mexico and other countries, including the United States, affect the airports or cities in which we operate, including airports or cities in the north of Mexico in which we have significant operations, and increase our insurance and security costs. We cannot assure you that the levels of violent crime in Mexico or their expansion to a larger portion of Mexico, over which we have no control, will not increase or decrease and will have no further adverse effects on the country’s economy and on our business, results of operations or financial condition.

Risks related to the airline industry

We operate in an extremely competitive industry.

We face significant competition with respect to routes, fares, services and slots in airports. Within the airline industry, we compete with legacy carriers, regional airlines and low-cost airlines on many of our routes. The intensity of the competition we face varies from route to route and depends on a number of factors, including the strength of competing airlines. Our competitors may have better brand recognition and greater financial and other resources than we do. In the event our competitors reduce their fares to levels which we are unable to match while sustaining profitable operations or are more successful in the operation of certain routes (as a result of service or otherwise), we may be required to reduce or withdraw services on the relevant routes, which may cause us to incur losses or may impact our growth, financial condition or results of operations. See Item 4: “Information on the Company—Business Overview—Competition.”

The airline industry is particularly susceptible to price discounting, because once a flight is scheduled, airlines incur only nominal additional costs to provide service to passengers occupying otherwise unsold seats. Increased fare or other price competition could adversely affect our results of operations and financial condition. Moreover, other airlines have begun to unbundle services by charging separate fees for services such as baggage transported, food and beverages consumed onboard and advance seat selection. This unbundling and potential reduction of costs could enable competitor airlines to reduce fares on routes that we serve, which may result in an improvement in their ability to attract customers and may affect our results of operations and financial condition.

15

In addition, airlines increase or decrease capacity in markets based on perceived profitability. Decisions by our competitors that increase overall industry capacity, or capacity dedicated to a particular region, market or route, could have a material adverse impact on our business. Our growth and the success of our ULCC business model could stimulate competition in our markets through our competitors’ development of their own ULCC strategies or new market entrants. Any such competitor may have greater financial resources and access to cheaper sources of capital than we do, which could enable them to operate their business with a lower cost structure than we can. If these competitors adopt and successfully execute a ULCC business model, we could be materially adversely affected, including our business, results of operations and financial condition.

We also face competition from air travel substitutes. On our domestic routes, we face competition from other transportation alternatives, such as bus or automobile. In addition, technology advancements may limit the desire for air travel. For example, video teleconferencing and other methods of electronic communication may reduce the need for in-person communication and add a new dimension of competition to the industry as travelers seek lower cost substitutes for air travel.

In December 2022, President Andrés Manuel López Obrador announced plans to create a new airline owned and operated by the Mexican government, to that effect in April 2023, the Chamber of Deputies approved amendments to the Mexican Civil Aviation Law (Ley de Aviación Civil) and Mexican Airports Law (Ley de Aeropuertos) that, among other things, would allow governmental entities to have concessions to operate both, civil airlines and airports. Such proposals, if adopted, would further increase our competition. If we are unable to adjust rapidly in the event the basis of competition in our markets changes, it could have a material adverse effect on our business, results of operations and financial condition.

The airline industry is heavily impacted by the price and availability of fuel. Continued volatility in fuel costs or significant disruptions in the supply of fuel could have a material adverse effect on our business, results of operations and financial condition.

Fuel is a major cost component for airlines and is our largest operating expense. The cost of fuel accounted for 27%, 34% and 46% (including derivative and non-derivative financial instruments for 2020 and 2021) of our total operating costs in 2020, 2021, and 2022, respectively. As such, our operating results are significantly affected by changes in the cost and availability of fuel. Both the cost and the availability of fuel are subject to economic, social and political factors and other events occurring throughout the world, which we can neither control nor accurately predict. Fuel prices have been subject to high volatility, fluctuating substantially over the past several years. Because Russia is one of the world’s largest oil exporters, we expect recent global developments relating to Russia’s invasion of Ukraine, and resulting export restrictions, will likely lead to decreased global supply and increased fuel prices, which effects could be more acute if the participants of the Organization of the Petroleum Exporting Countries, or OPEC, decide not to, or are unable to, increase their supply production. Due to the large proportion of fuel costs in our total operating cost base, even a relatively small increase in the price of fuel can have a significant negative impact on our operating costs and on our business, results of operations and financial condition. For more information on our cost of fuel, see Item 4: “Information on the Company—Business Overview—Fuel.”

Our inability to renew our concession or the revocation by the Mexican government of our concession would materially adversely affect us.

We hold a concession from the Mexican federal government that authorizes us to provide domestic air transportation services of passengers, cargo and mail within Mexico, or our Concession. Our Concession was granted by the Mexican government through the SICT on May 9, 2005 for an initial term of five years and was extended by the SICT on February 17, 2010 for an additional term of ten years. On February 21, 2020, our Concession was extended for an additional 20-year term starting on May 9, 2020.

Mexican law provides that concessions may be renewed several times. However, each renewal may not exceed 30 years and the law requires the concessionaire to:

| ● | have complied with the obligations set forth in the concession to be renewed; |

| ● | have requested the renewal one year before the expiration of the concession term; |

| ● | have made an improvement in the quality of the services during the term of the concession; and |

| ● | have accepted the new conditions established by the SICT according to the Mexican Aviation Law (Ley de Aviación Civil). |

16

Failure to renew our Concession would have a material adverse effect on our business, results of operations, financial condition and prospects and would prevent us from continuing to conduct our business.

In addition, we are required under the terms of our Concession to comply with certain ongoing obligations. Failure to comply with these obligations could result in penalties against us. The Mexican government has the right to revoke our Concession and the permits we currently hold for various reasons, including:

| ● | service interruptions; |

| ● | failure to comply with the terms of our Concession; |

| ● | if we assign or transfer rights under our Concession or permits; |

| ● | if we fail to maintain insurance required under applicable law; |

| ● | if we charge fares different from those registered with the SICT; |

| ● | if we violate statutory safety conditions; |

| ● | if we fail to pay statutory indemnification; or |

| ● | if we fail to pay to the Mexican government the required compensation. |

If our Concession or permits are revoked, we will be unable to operate our business as it is currently operated and be precluded from obtaining a new concession or permit for five years from the date of revocation. For more information on the potential causes for revocation of our Concession and permits, see Item 4: “Information of the Company—Regulation.”

Under Mexican law, our assets could be taken or seized by the Mexican government under certain circumstances.

Pursuant to Mexican law and our Concession, the Mexican federal government may take or seize our assets, temporarily or permanently, including our aircraft, in the event of a natural disaster, war, serious changes to public order or in the event of imminent danger to national security, internal peace or the national economy. The Mexican federal government, in all cases, except in the event of international war, must indemnify us by paying the respective losses and damages at market value. In these circumstances, we would not be able to continue with our normal operations. Applicable law is unclear as to how indemnification is determined and the timing of payment thereof. In addition, on March 28, 2023, the Mexican federal government sent an initiative to the Chamber of Deputies proposing amendments to 23 laws that regulate relationships between private parties and the government relating to, among other things, licenses, permits and concessions. Such amendments, if approved, could further limit the concessions and indemnifications that the Mexican federal government would be required to provide in these circumstances. Any seizure of our assets is likely to have a material adverse effect on our business, results of operations and financial condition.

The airline industry is particularly sensitive to changes in economic conditions. A global economic contraction could negatively impact our business, results of operations and financial condition.

Our business and the airline industry in general are affected by changing economic conditions beyond our control, including, but not limited to:

| ● | changes and volatility in general economic conditions, including the severity and duration of any downturn in Mexico, the United States or the global economy and financial markets; |

| ● | changes in consumer preferences, perceptions, spending patterns or demographic trends, including any increased preference for higher-fare carriers offering higher amenity levels, and reduced preferences for low-fare carriers offering more basic transportation, during better economic times or for other reasons; |

| ● | higher levels of unemployment and varying levels of disposable or discretionary income; |

17

| ● | health outbreaks, pandemics and other safety concerns; |

| ● | decreases in housing and stock market prices; |

| ● | lower levels of actual or perceived consumer confidence; |

| ● | high inflation rates; and |

| ● | increases in exchange rate volatility and fuel prices, especially in the context of the conflict between Russia and Ukraine. |

These factors can adversely affect our results of operations and financial condition, our ability to obtain financing on acceptable terms and our liquidity generally. Current unfavorable general economic conditions, such as higher unemployment rates, a constrained credit market, housing-related pressures and increased focus on reducing business operating costs can reduce spending for leisure, VFR and business travel. For many travelers, in particular the leisure and VFR travelers we serve, air transportation is a discretionary purchase that they can eliminate from their spending in difficult economic times.

In addition, adverse economic conditions could affect our ability to raise prices to counteract increased fuel, labor or other costs, which could result in a material adverse effect on our business, results of operations and financial condition. We are currently striving to increase demand for our flights among the portion of the population in Mexico that has traditionally used ground transportation for travel due to price constraints, by offering lower fares that compete with bus fares on similar routes. Unfavorable economic conditions could affect our ability to offer these lower fares and could affect this population segment’s discretionary spending in a more adverse manner than other travelers.

Further, in an inflationary environment, such as the current Mexico and U.S. economic environments, we may be unable to manage through the resulting increases in our operating costs depending on its effects on the airline industry and other economic conditions. We cannot predict how long the current inflationary period will last or if it will re-occur in the future. As such, we cannot guarantee that we will be able to maintain our costs at their current level. If our costs increase and we are no longer able to maintain a competitive cost structure, it could have a material adverse effect on our business, results of operations and financial condition.

The airline industry is heavily regulated and our financial condition and results of operations could be materially adversely affected if we fail to maintain the required U.S., Mexican, Central American and South American governmental concessions or authorizations necessary for our operations.

The airline industry is heavily regulated and we are subject to regulation in Mexico and in the United States for the routes we serve between Mexico and the United States. In order to maintain the necessary concessions or authorizations issued by the SICT, acting through the AFAC, the FAA and some of the aviation authorities in the Central and South American countries in which we operate, including authorizations to operate our routes, we must continue to comply with applicable statutes, rules and regulations pertaining to the airline industry, including any rules and regulations that may be adopted in the future.

We cannot predict which criteria the SICT will apply for awarding rights to landing slots, bi-lateral agreements, and international routes, which may prevent us from obtaining routes that may become available. In addition, international routes are limited by bi-lateral agreements and our expansion plans in the international market will be limited if we are unable to obtain new international routes. Furthermore, we cannot predict or control any actions that the AFAC, FAA or the aviation authorities in the Central and South American countries in which we operate may take in the future, which could include restricting our operations or imposing new and costly regulations.

Furthermore, our fares are subject to review by the AFAC, the FAA and some of the aviation authorities in the Central and South American countries in which we operate, any of which may in the future impose restrictions on our fares. Our business, results of operations and financial condition could be materially adversely affected if we fail to maintain the required U.S., Mexican, Central American and South American governmental concessions or authorizations or slots necessary for our operations.

18

The airline industry is subject to increasingly stringent environmental regulations and non-compliance therewith may adversely affect our financial condition and results of operations.

The airline industry is subject to increasingly stringent federal, state, local and foreign laws, regulations and ordinances relating to the protection of the environment, including those relating to emissions to the air, levels of noise, discharges to surface and subsurface waters, safe drinking water, and the management of hazardous substances, oils and waste materials. Compliance with all environmental laws and regulations can require significant expenditures and any future regulatory developments in Mexico, the United States and other countries in which we operate could adversely affect operations and increase operating costs in the airline industry. For example, some form of federal regulation may be forthcoming in the United States with respect to greenhouse gas emissions (including carbon dioxide, or CO2, and/or ‘cap and trade’ legislation), compliance with which could result in the creation of substantial additional costs to us. The U.S. Congress is considering climate change legislation and the EPA issued a rule that regulates larger emitters of greenhouse gases. Concerns about climate change and greenhouse gases may result in additional regulation or taxation of emissions, including aircraft emissions, in the United States and Mexico. Future operations and financial results may vary as a result of such regulations in the United States and equivalent regulations adopted by other countries, including Mexico, Central and South America. Compliance with these regulations and new or existing regulations that may be applicable to us in the future could increase our cost base and could have a material adverse effect on our business, results of operations and financial condition.