Table of Contents

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Title of each class |

Trading symbol |

Name of each exchange on which registered | ||

| |

|

|||

| 5,000 per share |

|

| ☒ |

☐ Accelerated Filer |

☐ Non-accelerated filer |

|

| ☐ U.S. GAAP |

☒ by the International Accounting Standards Board |

☐ Other |

| Auditor Name: |

Auditor Location: |

Auditor Firm ID: |

Table of Contents

TABLE OF CONTENTS

i

Table of Contents

ii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

The financial statements included in this annual report are prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or the IASB.

Unless expressly stated otherwise, all financial data included in this annual report are presented on a consolidated basis.

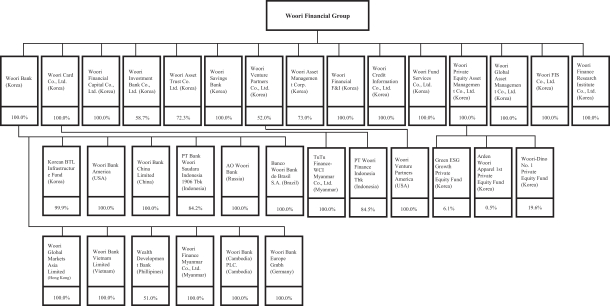

We were established on January 11, 2019 pursuant to a “comprehensive stock transfer” under Korean law, whereby holders of the common stock of Woori Bank and certain of its subsidiaries transferred all of their shares to us, a new financial holding company, and in return received shares of our common stock. As a result of the stock transfer, Woori Bank and certain of its former wholly-owned subsidiaries, Woori FIS Co., Ltd., Woori Finance Research Institute Co., Ltd., Woori Credit Information Co., Ltd., Woori Fund Services Co., Ltd. and Woori Private Equity Asset Management Co., Ltd., became our direct and wholly-owned subsidiaries. Accordingly, our overall business and operations after the stock transfer, on a consolidated basis, are identical to those of Woori Bank on a consolidated basis immediately prior to the stock transfer. See “Item 4.A. History and Development of the Company—Establishment of Woori Financial Group.”

The stock transfer constituted a succession for purposes of Rule 12g-3(a) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), such that our common stock was deemed registered under Section 12(b) of the Exchange Act by operation of Rule 12g-3(a). Following the stock transfer, we file reports under the Exchange Act as the successor issuer to Woori Bank.

In our consolidated financial statements for financial reporting periods beginning on or after January 1, 2019, the stock transfer is accounted for as a transaction among entities under common control applying the pooling of interests method of accounting (book value accounting). We initially recognized the transferred assets and liabilities at their book value as of the date of the stock transfer in such consolidated financial statements, and no goodwill was recognized in connection with the transaction.

The consolidated financial statements included in this annual report as of dates and for periods prior to the date of our establishment in January 2019 pursuant to the stock transfer were prepared based on the consolidated financial statements for Woori Bank and its subsidiaries, except that Woori FIS Co., Ltd., Woori Finance Research Institute Co., Ltd., Woori Credit Information Co., Ltd., Woori Fund Services Co., Ltd. and Woori Private Equity Asset Management Co., Ltd. were consolidated on a line-by-line basis instead of being presented as assets and liabilities held for sale. Unless expressly stated otherwise, historical financial data included in this annual report as of dates and for periods prior to our establishment are for Woori Bank and its subsidiaries, on a consolidated basis, with the foregoing modification. For further information regarding the accounting treatment of the stock transfer, see Note 1 of the notes to our consolidated financial statements included elsewhere in this annual report.

Unless otherwise indicated or required by the context, “we,” “us,” “our” and similar terms used in this annual report refer to Woori Financial Group and its subsidiaries (including Woori Bank) and, for periods prior to our establishment, refer to Woori Bank and its subsidiaries.

In this annual report:

| • | references to “Korea” are to the Republic of Korea; |

| • | references to the “government” are to the government of the Republic of Korea; |

| • | references to “Won” or “₩” are to the currency of Korea; |

| • | references to “U.S. dollars,” “$” or “US$” are to the currency of the United States; and |

| • | references to “Euros” or “EUR” are to the currency of the European Economic and Monetary Union. |

Discrepancies between totals and the sums of the amounts contained in any table may be a result of rounding.

For your convenience, this annual report contains conversions of Won amounts into U.S. dollars at the noon buying rate of the Federal Reserve Bank of New York for Won in effect on December 30, 2022, which was ₩1,260.2= US$1.00.

1

Table of Contents

FORWARD-LOOKING STATEMENTS

The U.S. Securities and Exchange Commission encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. This annual report contains forward-looking statements.

Words and phrases such as “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “estimate,” “expect,” “future,” “goal,” “intend,” “may,” “objective,” “plan,” “positioned,” “predict,” “project,” “risk,” “seek to,” “shall,” “should,” “will likely result,” “will pursue” and words and terms of similar substance used in connection with any discussion of future operating or financial performance or our expectations, plans, projections or business prospects identify forward-looking statements. In particular, the statements under the headings “Item 3.D. Risk Factors,” “Item 4.B. Business Overview” and “Item 5. Operating and Financial Review and Prospects” regarding our financial condition and other future events or prospects are forward-looking statements. All forward-looking statements are management’s present expectations of future events and are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements.

In addition to the risks related to our business discussed under “Item 3.D. Risk Factors,” other factors could cause actual results to differ materially from those described in the forward-looking statements. These factors include, but are not limited to:

| • | our ability to successfully implement our strategy; |

| • | future levels of non-performing loans; |

| • | our growth and expansion; |

| • | the adequacy of allowances for credit and other losses; |

| • | technological changes; |

| • | interest rates; |

| • | investment income; |

| • | availability of funding and liquidity; |

| • | our exposure to market risks; and |

| • | adverse market and regulatory conditions. |

By their nature, certain disclosures relating to these and other risks are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains, losses or impact on our income or results of operations could materially differ from those that have been estimated. For example, revenues could decrease, costs could increase, capital costs could increase, capital investment could be delayed and anticipated improvements in performance might not be fully realized.

In addition, other factors that could cause actual results to differ materially from those estimated by the forward-looking statements contained in this annual report could include, but are not limited to:

| • | general economic and political conditions in Korea or other countries that have an impact on our business activities or investments; |

| • | the monetary and interest rate policies of Korea; |

| • | inflation or deflation; |

| • | unanticipated volatility in interest rates; |

| • | foreign exchange rates; |

| • | prices and yields of equity and debt securities; |

2

Table of Contents

| • | the performance of the financial markets in Korea and globally; |

| • | changes in domestic and foreign laws, regulations and taxes; |

| • | changes in competition and the pricing environment in Korea; and |

| • | regional or general changes in asset valuations. |

For further discussion of the factors that could cause actual results to differ, see the discussion under “Item 3.D. Risk Factors” contained in this annual report. We caution you not to place undue reliance on the forward-looking statements, which speak only as of the date of this annual report. Except as required by law, we are not under any obligation, and expressly disclaim any obligation, to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise.

All subsequent forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this annual report.

| Item 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not Applicable

| Item 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not Applicable

| Item 3. | KEY INFORMATION |

| Item 3.A. | [Reserved] |

| Item 3.B. | Capitalization and Indebtedness |

Not Applicable

| Item 3.C. | Reasons for the Offer and Use of Proceeds |

Not Applicable

| Item 3.D. | Risk Factors |

Risks relating to our corporate credit portfolio

The largest portion of our exposure is to small- and medium-sized enterprises, and financial difficulties experienced by companies in this segment may result in a deterioration of our asset quality and have an adverse impact on us.

Our loans to small- and medium-sized enterprises amounted to ₩112,696 billion, or 33.4% of our total loans, as of December 31, 2021, and ₩122,925 billion, or 35.6% of our total loans, as of December 31, 2022. As of December 31, 2022, Won-denominated loans to small- and medium-sized enterprises that were classified as substandard or below were ₩399 billion, representing 0.3% of such loans to those enterprises. See “Item 4.B. Business Overview—Corporate Banking—Small and Medium-Sized Enterprise Banking.” We recorded charge-offs of ₩117 billion in respect of our Won-denominated loans to small- and medium-sized enterprises in 2022, compared to charge-offs of ₩158 billion in 2021 and ₩219 billion in 2020. According to data compiled by the Financial Supervisory Service, the industry-wide delinquency ratios for Won-denominated loans to small- and medium-sized enterprises decreased in 2021 but increased in 2022, and was 0.32% as of December 31, 2022. The delinquency ratio for small- and medium-sized enterprises is calculated as the ratio of (1) the outstanding balance of such loans in respect of which either principal or interest payments are overdue by one month or more to (2) the aggregate outstanding balance of such loans. Our delinquency ratio for such loans denominated in Won was 0.3% as of December 31, 2021 and 0.3% as of December 31, 2022. Our delinquency ratio may increase in 2023 as a result of, among other things, adverse changes in economic conditions in Korea and globally. See

3

Table of Contents

“—Other risks relating to our business—Unfavorable changes in the global financial markets could adversely affect our results of operations and financial condition.” Accordingly, we may be required to take measures to decrease our exposures to these customers.

In light of the impact on the financial condition and liquidity position of small- and medium-sized enterprises in Korea as a result of the global financial crisis occurring in 2008, the Korean government introduced measures intended to encourage Korean banks to provide financial support to small- and medium-sized enterprise borrowers. For example, the Korean government requested that Korean banks, including Woori Bank, establish a “fast track” program to provide liquidity assistance to small- and medium-sized enterprises on an expedited basis. Under the “fast track” program established by Woori Bank, liquidity assistance is provided to small- and medium-sized enterprise borrowers applying for such assistance, in the form of new short-term loans or maturity extensions or interest rate adjustments with respect to existing loans, after expedited credit review and approval. The aggregate amount of outstanding small- and medium-sized enterprise loans made by us under the “fast track” program was ₩86 billion as of December 31, 2022, which represented 0.07% of our total small- and medium-sized enterprise loan portfolio as of such date. Furthermore, loans made by us under the “fast track” program are partially guaranteed by the Korean government’s public financial institutions, including the Korea Credit Guarantee Fund and the Korea Technology Finance Corporation.

The overall prospects for the Korean economy in 2023 and beyond remain uncertain, especially in light of the COVID-19 pandemic affecting many countries worldwide, including Korea, and the Korean government may extend or renew existing or past policies and initiatives or introduce new policies or initiatives to encourage Korean banks to provide financial support to small- and medium-sized enterprises. See “—Other risks relating to our business—The COVID-19 pandemic has adversely affected and may continue to adversely affect our business, financial condition or results of operations.” For example, the Financial Services Commission requested that 15 Korean banks, including Woori Bank, extend special low-rate loans to small merchants affected by the COVID-19 pandemic beginning in April 2020. Such Korean banks, including Woori Bank, provided new loans under such program until January 3, 2022. In addition, Korean financial regulatory authorities, including the Financial Services Commission and the Financial Supervisory Service, adopted guidelines for Korean banks to extend loan terms and defer interest payments with respect to small- and medium sized enterprises and small merchants affected by the COVID-19 pandemic starting from April 2020, but such measures ceased to be effective in September 2022. As of December 31, 2022, the aggregate amount of loans affected by such measures provided by the four major commercial Korean banks, including Woori Bank, Kookmin Bank, KEB Hana Bank and Shinhan Bank, was ₩36.8 trillion, of which ₩11.2 trillion was provided by Woori Bank. In October 2022, the Korean government also launched the New Start Fund, a debt adjustment program, under which pandemic-hit micro-enterprises and self-employed business owners can apply for debt adjustment, and once accepted, will be supported through customized debt adjustment plans according to their respective credit conditions and types of loans. Under the New Start Fund program, the Korean government may purchase the loan directly and then make adjustment, or if the relevant financial institution agrees, allow the relevant financial institution to restructure the loan directly. We believe that, to date, our participation in such government-led initiatives has not caused us to extend a material amount of credit that we would not have otherwise extended nor materially impacted our results of operations and financial condition in general. However, there can be no assurance that our future participation in such government-led initiatives would not lead us to extend credit to small- and medium-sized enterprise borrowers that we would not otherwise extend, or offer terms for such credit that we would not otherwise offer, in the absence of such initiatives. Furthermore, there is no guarantee that the financial condition and liquidity position of our small- and medium-sized enterprise borrowers benefiting from such initiatives will improve sufficiently for them to service their debt on a timely basis, or at all. Accordingly, increases in our exposure to small- and medium-sized enterprises resulting from such government-led initiatives may have a material adverse effect on our results of operations and financial condition.

On October 4, 2022, Woori Bank started to operate a deferment program similar to the “COVID-19 SME and Small Merchant Financial Support Program”, which had been established by the Korean government for small- and medium-sized enterprises and small merchants that have been negatively impacted by the COVID-19 pandemic. Under this deferment program, with respect to loans made to borrowers which have been adversely

4

Table of Contents

impacted by the COVID-19 pandemic (excluding loans related to the sale or lease of real property and loans made to borrowers engaged in certain unwholesome businesses), Woori Bank may extend their maturity date up until September 30, 2025, and may defer the borrowers’ payment obligation for the interests and principal of such loans up until September 2023.

Many small- and medium-sized enterprises represent sole proprietorships or very small businesses dependent on a relatively limited number of suppliers or customers and tend to be affected by fluctuations in the Korean and global economy to a greater extent than large corporate borrowers. In addition, small- and medium-sized enterprises often maintain less sophisticated financial records than large corporate borrowers. Therefore, it is generally more difficult for us to judge the level of risk inherent in lending to these enterprises, as compared to large corporations. However, in light of the COVID-19 pandemic, the Bank of Korea early implemented the Basel III final reforms in September 2020, which lowered the average risk weight of loans extended to small- and medium-sized enterprises with no credit rating from 100% to 85% in an effort to boost such lending.

In addition, many small- and medium-sized enterprises have close business relationships with large corporations in Korea, primarily as suppliers. Any difficulties encountered by those large corporations would likely harm the liquidity and financial condition of related small- and medium-sized enterprises, including those to which we have exposure, also resulting in an impairment of their ability to repay loans.

Financial difficulties experienced by small- and medium-sized enterprises as a result of, among other things, adverse changes in domestic and global economic conditions, could have an adverse impact on the ability of small- and medium-sized enterprises to make payments on their loans. For example, the COVID-19 pandemic has had a significant adverse impact on the Korean and global economy, including disruptions in supply chains, declines in the sales and deterioration in the financial conditions of small- and medium-sized enterprises. See “—Other risks relating to our business—The COVID-19 pandemic has adversely affected and may continue to adversely affect our business, financial condition or results of operations.” In addition, aggressive marketing and competition among banks to lend to this segment may lead to a deterioration in the asset quality of our loans to this segment in the future. Any such deterioration would result in increased charge-offs, higher provisioning and reduced interest and fee income from this segment, which would have an adverse impact on our financial condition and results of operations.

We have exposure to companies in certain troubled industries, and financial difficulties of these companies may adversely impact us.

As of December 31, 2022, the total amount of loans provided by us to construction, shipbuilding and shipping companies in Korea amounted to ₩6,022 billion, ₩253 billion and ₩193 billion, or 1.7%, 0.1% and 0.1% of our total loans, respectively. We also have other exposures to Korean construction, shipbuilding and shipping companies, including in the form of guarantees extended for the benefit of such companies and debt and equity securities of such companies held by us. In the case of construction companies, we have potential exposure in the form of guarantees provided to us by general contractors with respect to financing extended by us for residential and commercial real estate development projects, as well as commitments to purchase asset-backed securities secured by the assets of companies in the construction industry and other commitments we enter into relating to project financing for such real estate projects which may effectively function as guarantees. In the case of shipbuilding companies, such exposures include refund guarantees extended by us on behalf of shipbuilding companies to cover their obligation to return a portion of the ship order contract amount to customers in the event of performance delays or defaults under shipbuilding contracts.

The construction industry in Korea has undergone significant fluctuations in recent years. Following a period of growth from 2015 to 2018, the construction industry had stagnated from 2019 to 2020, caused mainly by the uncertainty resulting from the Korean government’s strengthening of mortgage and other lending regulations to control the rising real property prices. After a brief period of recovery in 2021, the construction industry has again experienced a downturn starting in 2022, caused by the rise in interest rates and the resulting decline in demand for residential property throughout Korea, as well as drastic changes in the price and availability of construction materials due to disruptions in global supply chains caused by the ongoing

5

Table of Contents

invasion of Ukraine by Russia. While the shipbuilding industry has experienced rapid growth in recent years led by an increase in global demand for liquefied natural gas carriers resulting from stronger environmental regulations and global energy security concerns, the prospects for this industry currently remain uncertain given the slowdown in the global economy and a rise in shipbuilding costs and resulting prices. In the case of shipping companies in Korea, the COVID-19 pandemic and the ensuing global lockdown caused a severe downturn in the industry in 2020. Although the industry subsequently showed signs of recovery from the pandemic as the levels of consumer spending and global trade began to rise, the industry currently faces difficulties, among others arising from a deteriorating global economy and disruptions in the global supply chain due to port congestions and the continuing COVID-19 lockdowns in China.

In addition, we have significant exposures to companies in the hotel, leisure and transportation industries, which have been adversely impacted by the COVID-19 pandemic. As of December 31, 2022, the total amount of loans provided by us to companies in the hotel, leisure and transportation industries amounted to an aggregate ₩11,244 billion, or 3.3% of our total loans. While the business activities, results of operations and financial condition of companies in such industries may recover as the impact of the pandemic decreases, the timeline for such recovery remains uncertain, and we may be required to record substantial additional allowances relating to such companies.

The allowance for credit losses that we have established against our credit exposures to companies in the Korean construction, shipbuilding and shipping industries as well as the hotel, leisure and transportation industries may not be sufficient to cover all future losses arising from these and other exposures. If the credit quality of our exposures to such companies declines further, we may incur substantial additional provisions for credit loss, which could adversely impact our results of operations and financial condition. Furthermore, although a portion of our loans to companies in the construction, shipbuilding and shipping industries as well as the hotel, leisure and transportation industries are secured by collateral, such collateral may not be sufficient to cover uncollectible amounts in respect of such loans.

A large portion of our exposure is concentrated in a relatively small number of large corporate borrowers, which increases the risk of our corporate credit portfolio.

As of December 31, 2022, our 20 largest exposures to corporate borrowers (including loans, debt and equity securities, credit-related commitments and other exposures) totaled ₩66,929 billion, which represented 12.1% of our total exposures. As of that date, our single largest corporate exposure was to Korea Development Bank, to which we had outstanding credits in the form of debt securities of ₩14,123 billion and loans in Won of ₩165 billion, representing 2.6% of our total exposures in the aggregate. Aside from exposure to the Korean government and government-related agencies, our next largest exposure was to Kookmin Bank, to which we had outstanding exposure of ₩1,028 billion representing 0.2% of our total exposures. Any deterioration in the financial condition of our large corporate borrowers, including those in industries particularly affected by the COVID-19 pandemic or to which we have significant exposures such as the hotel, leisure and transportation industries, the retail and wholesale industries and the manufacturing industry, may require us to record substantial additional allowances and may have a material adverse impact on our results of operations and financial condition.

We have exposure to the largest Korean commercial conglomerates, known as “chaebols,” and, as a result, financial difficulties of chaebols may have an adverse impact on us.

Of our 20 largest corporate exposures as of December 31, 2022, 3 were to companies that were members of the 40 largest chaebols in Korea. As of that date, the total amount of our exposures to these chaebols was ₩21,622 billion, or 3.9% of our total exposures. If the credit quality of our exposures to chaebols declines as a result of financial difficulties they experience or for other reasons, we could incur additional provisions for credit loss, which would adversely impact our results of operations and financial condition. See “Item 4.B. Business Overview—Assets and Liabilities—Loan Portfolio—Exposure to Chaebols.”

6

Table of Contents

The allowances we have established against these exposures may not be sufficient to cover all future losses arising from these exposures. In addition, in the case of any of these companies that are currently in or in the future may enter into workout, restructuring, reorganization or liquidation proceedings, our recoveries from those companies may be limited. We may, therefore, experience future losses with respect to these exposures.

We have exposure to companies that are currently or may in the future be put in restructuring and may suffer losses as a result of additional provisions for credit loss required or the adoption of restructuring plans with which we do not agree.

As of December 31, 2022, our credit exposures to companies that were in workout or corporate restructuring amounted to ₩186 billion or 0.03% of our total credit exposures, of which ₩127 billion or 68.3% was classified as substandard or below and substantially all of which was classified as impaired. As of the same date, our allowance for credit losses on these credit exposures amounted to ₩65 billion, or 34.9% of these exposures. These allowances may not be sufficient to cover all future losses arising from our credit exposure to these companies. Furthermore, we have other exposure to such companies in the form of debt and equity securities of such companies held by us (including equity securities we acquired as a result of debt-to-equity conversions). Including such securities, our exposures as of December 31, 2022 to companies in workout or restructuring amounted to ₩186 billion, or 0.03% of our total exposures. Our exposures to such companies may also increase in the future, including as a result of adverse conditions in the Korean economy. In addition, in the case of borrowers that are or become subject to workout, we may be forced to restructure our credits pursuant to restructuring plans approved by other creditor financial institutions of the borrower, or to dispose of our credits to other creditors on unfavorable terms, which may adversely affect our results of operations and financial condition.

Risks relating to our consumer credit portfolio

We may experience increases in delinquencies in our consumer loan and credit card portfolios.

In recent years, consumer debt has increased rapidly in Korea. Our portfolio of consumer loans amounted to ₩148,361 billion as of December 31, 2021 and ₩143,940 billion as of December 31, 2022. Our credit card portfolio amounted to ₩9,757 billion as of December 31, 2021 and ₩10,370 billion as of December 31, 2022. As of December 31, 2022, our consumer loans and credit card receivables represented 41.7% and 3.0% of our total lending, respectively. See “Item 4.B. Business Overview—Consumer Banking—Lending Activities” and “Item 4.B. Business Overview—Credit Cards—Products and Services.”

The growth in our consumer loan portfolio in recent years, together with adverse changes in economic conditions in Korea and globally, may lead to increasing delinquencies and a deterioration in asset quality. The amount of our consumer loans classified as substandard or below was ₩354 billion (or 0.2% of our consumer loan portfolio) as of December 31, 2021 and ₩392 billion as of December 31, 2022 (or 0.3% of our consumer loan portfolio). We charged off consumer loans amounting to ₩161 billion in 2022, as compared to ₩173 billion in 2021 and ₩182 billion in 2020, and recorded provisions for credit loss in respect of consumer loans of ₩206 billion in 2022, as compared to ₩168 billion in 2021 and ₩131 billion in 2020. Within our consumer loan portfolio, the outstanding balance of general purpose household loans, which, unlike mortgage or home equity loans, are often unsecured and therefore tend to carry a higher credit risk, amounted to ₩32,003 billion, or 21.6% of our total outstanding consumer loans, as of December 31, 2021 and ₩28,694 billion, or 19.9% of our total outstanding consumer loans, as of December 31, 2022.

In our credit card segment, outstanding balances overdue by more than one month amounted to ₩79 billion, or 0.8% of our credit card receivables, as of December 31, 2021 and ₩143 billion, or 1.4% of our credit card receivables, as of December 31, 2022. In line with industry practice, we have restructured a portion of our delinquent credit card account balances as loans. As of December 31, 2022, these restructured loans amounted to ₩134 billion, or 1.3% of our credit card balances. Because these restructured loans are not initially recorded as being delinquent, our delinquency ratios do not fully reflect all delinquent amounts relating to our credit card balances. Including all restructured loans, outstanding balances overdue by more than one month accounted

7

Table of Contents

for 2.6% of our credit card balances as of December 31, 2022. We charged off credit card balances amounting to ₩220 billion in 2022, as compared to ₩220 billion in 2021 and ₩246 billion in 2020, and recorded provisions for credit loss in respect of credit card balances of ₩222 billion in 2022, as compared to ₩177 billion in 2021 and ₩188 billion in 2020. Delinquencies may increase in the future as a result of, among other things, adverse economic conditions in Korea, additional government regulation or the inability of Korean consumers to manage increased household debt.

A deterioration of the asset quality of our consumer loan and credit card portfolios would require us to record increased provisions for credit loss and charge-offs and adversely affect our financial condition and results of operations. In addition, our large exposure to consumer loans means that we are exposed to changes in economic conditions affecting Korean consumers. Accordingly, economic difficulties in Korea that harm those consumers could result in further deterioration in the credit quality of our consumer loan and credit card portfolios. For example, the severe impact of the COVID-19 pandemic on Korea’s economy may disrupt the business, activities and operations of our consumers, which in turn could result in a significant decrease in the number of financial transactions or the inability of our consumers to meet existing payment or other obligations to us. In addition, a rise in unemployment or an increase in interest rates in Korea could adversely affect the ability of consumers to make payments and increase the likelihood of potential defaults. See “Risks relating to Korea—Unfavorable financial and economic developments in Korea may have an adverse effect on us.”

In addition, we are exposed to changes in regulations and policies on consumer lending by the Korean government, which may adopt measures to restrict consumer lending or encourage financial institutions to provide financial support to certain types of retail borrowers. In 2014 and 2015, the Korean government implemented several measures to encourage consumer spending and revive the housing market in Korea, including loosening regulations on mortgage lending, which contributed to an increase in our portfolio of consumer loans. However, the Korean government introduced various measures from the second half of 2016 to 2021 to tighten regulations on mortgage and other lending and housing subscription in response to the rapid growth in consumer debt and concerns over speculative investments in real estate in certain areas. Although the Korean government has since begun to reverse some of these measures by introducing a number of policy measures that seek to sustain housing prices and activity levels in the Korean real estate market over the course of 2022, the impact of such policy measures are not yet clear. A decrease in housing prices, together with the high level of consumer debt and rising interest rate levels, could result in declines in consumer spending and reduced economic growth, which may lead to increases in delinquency levels of our consumer loan and credit card portfolios.

Under a pre-workout program established by Korean banks for retail borrowers with outstanding short-term debt, including Woori Bank, which has been in operation since April 2009, maturity extensions and/or interest reductions are provided to retail borrowers with total loans of ₩1.5 billion or less (consisting of no more than ₩500 million of unsecured loans and ₩1 billion of secured loans) who are in arrears on their payments for more than 30 days but less than 90 days or for retail borrowers with an annual income of ₩40 million or less who have been in arrears on their payments for 30 days or more on an aggregate basis for the 12 months prior to their application, among others. The aggregate amount of consumer credit (including credit card receivables) we provided which became subject to the pre-workout program in 2022 was ₩53 billion. While we believe that our operation of the pre-workout program has not had a material impact on the overall credit quality of our consumer loan and credit card portfolios to date, our participation in such government-led initiatives to provide financial support to retail borrowers may lead us to offer credit terms for such borrowers that we would not otherwise offer in the absence of such initiatives, which may have an adverse effect on our results of operations and financial condition.

A decline in the value of the collateral securing our consumer loans and our inability to realize full collateral value may adversely affect our consumer credit portfolio.

A substantial portion of our consumer loans is secured by real estate, the values of which have fluctuated significantly in recent years. Although it is our general policy to lend up to 70% of the appraised value of collateral (except in certain regulated areas designated by the government where we generally limit our lending

8

Table of Contents

to 50% of the appraised value of collateral, and for first-time homebuyers, we may lend up to 80% of the appraised value of collateral) and to periodically re-appraise our collateral, a downturn in the real estate markets in Korea may result in a decline in the value of the collateral securing our mortgage and home equity loans. If collateral values decline in the future, they may not be sufficient to cover uncollectible amounts in respect of secured loans extended by us. Any declines in the value of the real estate or other collateral securing our consumer loans, or our inability to obtain additional collateral in the event of such declines, could result in a deterioration in our asset quality and may require us to record additional allowances for credit losses.

In Korea, foreclosure on collateral generally requires a written petition to a court. An application, when made, may be subject to delays and administrative requirements that may decrease the value of such collateral. We cannot guarantee that we will be able to realize the full value on our collateral as a result of, among other factors, delays in foreclosure proceedings and defects in the perfection of our security interest in collateral. Our failure to recover the expected value of collateral could expose us to potential losses.

Risks relating to our financial holding company structure and strategy

We may not succeed in implementing our strategy to take advantage of, or fail to realize the anticipated benefits of, our financial holding company structure.

We were established as a new financial holding company in January 2019 pursuant to a “comprehensive stock transfer” under Korean law, following the completion of which Woori Bank, Woori FIS Co., Ltd., Woori Finance Research Institute Co., Ltd., Woori Credit Information Co., Ltd., Woori Fund Services Co., Ltd. and Woori Private Equity Asset Management Co., Ltd. became our wholly-owned subsidiaries. See “Item 4A. History and Development of the Company—Establishment of Woori Financial Group.”

One of our principal strategies is to take advantage of our financial holding company structure to become a comprehensive financial services provider capable of developing and cross-selling a diverse range of products and services to our large existing base of retail and corporate banking customers. An intended benefit of our financial holding company structure is that it enhances our ability to engage in mergers and acquisitions which we may decide to pursue as part of our strategy. Accordingly, we may consider acquiring or merging with other financial institutions, particularly in the non-banking sector, to achieve more balanced growth and further diversify our revenue base. We may also continue to seek opportunities to expand our operations in markets outside Korea. See “Item 4.B. Business Overview—Strategy” and “—We may not be able to successfully execute our overseas expansion strategy.”

The integration of companies we may acquire or merge with in the future under our financial holding company structure could require a significant amount of time, financial resources and management attention. Moreover, that process could place a burden on our operations (including our risk management operations) or information technology systems, reduce employee morale, produce unintended inconsistencies in our standards, controls, procedures or policies, and affect our relationships with customers and our ability to retain key personnel. The realization of the anticipated benefits of our financial holding company structure may be blocked, delayed or reduced as a result of many factors, some of which may be outside our control. These factors include:

| • | competition from other financial institutions, as well as private equity firms and other potential acquirers, in Korea and elsewhere in terms of identifying and winning bids for attractive merger and acquisition targets in the financial industry, including the non-banking sector, which may make it challenging for us to successfully acquire, or which may require us to pay a high acquisition price for, such targets; |

| • | difficulties in integrating the diverse activities and operations of our subsidiaries or any companies we may acquire, including risk management operations and information technology systems, personnel, policies and procedures; |

| • | difficulties in reorganizing or reducing overlapping personnel, branches, networks and administrative functions; |

9

Table of Contents

| • | restrictions under the Financial Holding Company Act and other regulations on transactions between a financial holding company and, or among, its subsidiaries; |

| • | failure to leverage our financial holding company structure to realize operational efficiencies and to cross-sell multiple products and services; |

| • | unforeseen contingent risks, including lack of required capital resources, increased tax liabilities or restrictions in our overseas operations, relating to our financial holding company structure; |

| • | unexpected business disruptions; |

| • | failure to attract, develop and retain personnel with necessary expertise; |

| • | loss of customers; and |

| • | labor unrest. |

Accordingly, we may not be able to realize the anticipated benefits of our financial holding company structure, and our business, results of operations and financial condition may suffer as a result.

We depend on limited forms of funding to fund our operations at the holding company level.

We are a financial holding company with no significant assets other than the shares of our subsidiaries. Our primary sources of funding and liquidity are dividends from our subsidiaries, sales of interests in our subsidiaries and direct borrowings and issuances of equity or debt securities at the holding company level. In addition, as a financial holding company, we are required to meet certain minimum financial ratios under Korean law, including with respect to liquidity and capital adequacy. Our ability to meet our obligations to our direct creditors and employees and our other liquidity needs and regulatory requirements at the holding company level depends on timely and adequate distributions from our subsidiaries and our ability to sell our securities or obtain credit from our lenders.

The ability of our subsidiaries to pay dividends to us depends on their financial condition and operating results. In the future, our subsidiaries may enter into agreements, such as credit agreements with lenders or indentures relating to high-yield or subordinated debt instruments, that impose restrictions on their ability to make distributions to us, and the terms of future obligations and the operation of Korean law could prevent our subsidiaries from making sufficient distributions to us to allow us to make payments on our outstanding obligations. See “—As a financial holding company, we largely depend on receiving dividends from our subsidiaries to pay dividends on our common stock.” Any delay in receipt of or shortfall in payments to us from our subsidiaries could result in our inability to meet our liquidity needs and regulatory requirements, including minimum liquidity and capital adequacy ratios, which may disrupt our operations at the holding company level.

In addition, our creditors will generally not be able to assert claims on the assets of our subsidiaries. Furthermore, our inability to sell our securities or obtain funds from our lenders on favorable terms, or at all, could also result in our inability to meet our liquidity needs and regulatory requirements and may disrupt our operations at the holding company level.

As a financial holding company, we largely depend on receiving dividends from our subsidiaries to pay dividends on our common stock.

Since our principal assets at the holding company level are the shares of our subsidiaries, our ability to pay dividends on our common stock largely depends on dividend payments from those subsidiaries. Those dividend payments are subject to the Korean Commercial Code, the Bank Act and regulatory limitations, generally based on capital levels and retained earnings, imposed by the various regulatory agencies with authority over those entities. The ability of our subsidiaries to pay dividends may be subject to regulatory restrictions to the extent that paying dividends would impair their respective non-consolidated profitability, financial condition or other cash flow needs. For example:

| • | under the Korean Commercial Code, dividends may only be paid out of distributable income, an amount which is calculated by subtracting the aggregate amount of a company’s paid-in capital and certain |

10

Table of Contents

| mandatory legal reserves as well as certain unrealized profits from its net assets, in each case as of the end of the prior fiscal period; |

| • | under the Bank Act, a bank also must credit at least 10% of its net profit to a legal reserve each time it pays dividends on distributable income until that reserve equals the amount of its total paid-in capital; and |

| • | under the Bank Act and the requirements of the Financial Services Commission, if a bank fails to meet its required capital adequacy ratio or otherwise becomes subject to management improvement measures imposed by the Financial Services Commission, then the Financial Services Commission may restrict the declaration and payment of dividends by that bank. |

Our subsidiaries may not continue to meet the applicable legal and regulatory requirements for the payment of dividends in the future. If they fail to do so, they may stop paying or reduce the amount of the dividends they pay to us, which would have an adverse effect on our ability to pay dividends on our common stock.

The implementation of the Korean government’s privatization plan may have an adverse effect on us and your interests as a shareholder.

In June 2013, the Korean government, through the Public Funds Oversight Committee of the Financial Services Commission, announced an updated plan to privatize Woori Finance Holdings, Woori Bank’s former parent company, and its former subsidiaries. The privatization plan provided for the segregation of such entities into three groups and the disposal of the Korean government’s interest in these entities held through the Korea Deposit Insurance Corporation, or the KDIC, in a series of transactions, most of which have been completed. Such transactions included the following:

| • | Kwangju Bank and Kyongnam Bank. In May 2014, Woori Finance Holdings established KJB Financial Group and KNB Financial Group through a spin-off of its businesses related to the holding of the shares and thereby controlling the business operations of Kwangju Bank and Kyongnam Bank, respectively. As a result of such spin-off, KJB Financial Group became the owner of the shares of Kwangju Bank previously held by Woori Finance Holdings and KNB Financial Group became the owner of the shares of Kyongnam Bank previously held by Woori Finance Holdings. Woori Finance Holdings no longer owned any shares of Kwangju Bank or Kyongnam Bank, and neither they nor their new holding companies were its subsidiaries, after the spin-off. Following such spin-off, each of these banks was merged with its holding company, and in October 2014, the KDIC sold its 56.97% ownership interest in Kwangju Bank and Kyongnam Bank to JB Financial Group and BNK Financial Group (formerly known as BS Financial Group), respectively. |

| • | Woori Investment & Securities and Other Subsidiaries. In March 2014, Woori Finance Holdings sold its 52.0% ownership interest in Woori Financial to KB Financial Group. In May 2014, Woori Finance Holdings sold its 100.0% ownership interest in Woori Asset Management to Kiwoom Securities and sold its 100.0% ownership interest in Woori F&I to Daishin Securities. In June 2014, Woori Finance Holdings sold its 37.9% ownership interest in Woori Investment & Securities, its 51.6% ownership interest in Woori Aviva Life Insurance and its 100.0% ownership interest in Woori FG Savings Bank to NongHyup Financial Group in a collective sale. As a result of such sales, Woori Investment & Securities, Woori Asset Management, Woori Aviva Life Insurance, Woori FG Savings Bank, Woori F&I and Woori Financial were no longer subsidiaries of Woori Finance Holdings, and it no longer owned any shares in such former subsidiaries. |

| • | Woori Bank. In November 2014, Woori Finance Holdings merged with and into Woori Bank. As a result of the merger, the other former subsidiaries of Woori Finance Holdings, including Woori Card, Woori Private Equity, Woori FIS, Woori Investment Bank and Woori Finance Research Institute, became Woori Bank’s subsidiaries. In December 2014, the KDIC sold 40,143,022 shares of Woori Bank’s common stock (representing 5.9% of its outstanding common stock) through a bidding process in Korea. In addition, in December 2016 and January 2017, the KDIC sold an aggregate of 200,685,395 |

11

Table of Contents

| shares of Woori Bank’s common stock (representing 29.7% of its outstanding common stock) in stakes ranging from 3.7% to 6.0% to seven financial companies through a bidding process. In 2017, pursuant to a series of transactions related to call options previously granted in connection with the KDIC’s sale of Woori Bank’s common stock in December 2014, the KDIC sold an aggregate of 19,852,364 shares of Woori Bank’s common stock (representing 2.9% of its outstanding common stock). As a result of such transactions, the KDIC’s ownership interest in Woori Bank was reduced to 18.4%. |

| • | Woori Financial Group. In connection with our establishment in January 2019 as a new financial holding company pursuant to a “comprehensive stock transfer” under Korean law, the KDIC received 124,604,797 shares of our outstanding common stock in exchange for the common stock of Woori Bank it owned. In June 2019, the Financial Services Commission approved the KDIC’s plan to sell all such common stock in multiple transactions by 2022. In April 2021, pursuant to this plan, the KDIC sold an aggregate of 14,445,354 shares of our common stock (representing 2.0% of our outstanding common stock) in a block trade. In December 2021, the KDIC sold an aggregate 9.3% of our outstanding common stock in stakes ranging from 1.0% to 4.0% to four companies and 1.0% to our employee stock ownership association. In February 2022, the KDIC sold an aggregate of 15,860,000 shares of our common stock (representing 2.2% of our outstanding common stock) in a block trade. The KDIC further sold an aggregate of 17,000,000 shares, or 2.3%, of Woori Financial Group’s outstanding common stock in a block trade in May 2022. As a result of such transactions, the KDIC currently owns 1.3% of our outstanding common stock. |

See “Item 4.A. History and Development of the Company—Privatization Plan.”

The implementation of the Korean government’s privatization plan, including the expected sale of the KDIC’s remaining ownership interest in us to third parties, may have an adverse effect on us and your interest as a shareholder. Although the KDIC has already disposed of most of its ownership interest in us, the KDIC’s sale of its remaining interest to third parties may affect our business, management, strategy, capital structure and assets and liabilities and lead to diversion of management attention, a loss of customers and labor unrest. There is also no guarantee that prior sales by KDIC of its ownership interest in us will not result in unintended adverse tax consequences for us and our subsidiaries, as well as our shareholders. See “—Risks relating to our common stock and ADSs—Prior sales by the KDIC of shares of our common stock may result in adverse Korean tax consequences for you.” Accordingly, the implementation of the privatization plan may have a material adverse effect on the trading price of our common stock and American depositary shares, or ADSs, and your interests as a shareholder.

We may not be able to successfully execute our overseas expansion strategy.

As part of our business strategy, we have been seeking opportunities to expand our operations in markets outside Korea, including through the opening of additional overseas branches and offices as well as strategic acquisitions and investments, particularly in South and Southeast Asia. For example, Woori Bank expanded its network of branches to India, where it established branches in Chennai, Gurgaon and Mumbai from 2012 to 2017. In October 2016, Woori Bank acquired a 51% equity interest in Wealth Development Bank, a thrift bank in the Philippines. In November 2016, Woori Bank obtained a banking license to establish a local subsidiary in Vietnam, Woori Bank Vietnam, which commenced operations in January 2017 and currently operates 20 branches throughout the country. In June 2018, Woori Bank acquired VisionFund (Cambodia) Ltd., a microfinance deposit-taking institution in Cambodia, and renamed it WB Finance Co., Ltd. In February 2020, WB Finance Co., Ltd. merged with Woori Finance (Cambodia) Plc., a Cambodian microfinance institution, and in November 2021, it obtained a commercial banking license from the Cambodian financial authorities and began its nationwide operations as Woori Bank (Cambodia) PLC. Notwithstanding the foregoing, the expansion of our operations abroad may be difficult due to the presence of established competitors in the relevant local markets. In addition, overseas expansion and the management of international operations may require significant financial expenditures as well as management attention, and will subject us to the challenges of operating in an unfamiliar business environment with different regulatory, legal and taxation systems and political, economic and social

12

Table of Contents

risks. Accordingly, there is no guarantee that we will be successful in executing our overseas expansion strategy. The failure of our overseas expansion strategy could have an adverse impact on our business, results of operations and financial condition.

We may not generate sufficient additional fees to achieve our revenue diversification strategy.

An important element of our overall strategy is increasing our fee income in order to diversify our revenue base. Historically, our primary source of revenues has been net interest income from our banking operations at Woori Bank. Our current sources of fee income include our investment banking, asset management, assets trustee, currency transfers and lending businesses. However, to date, except for fees collected in connection with certain of our services including investment banking, asset management and currency transfers (including foreign exchange-related commissions), we have not generated substantial fee income. We intend to continue to develop new sources of fee income as part of our business strategy, including through our current investment banking, asset management, assets trustee and lending businesses, as well as through merger with or acquisition of non-banking businesses which we may decide to pursue. For example, in March 2023, we acquired a 52% equity interest as well as the management rights in Daol Investment, which is a venture capital company with ₩1.4 trillion of assets under its management. See “Item 4.B. Business Overview—Strategy.” However we may not be successful in our efforts to develop new sources of fee income, and the new sources of fee income we have developed may not generate sufficient additional fees to achieve our revenue diversification strategy. Although we, like many other Korean financial institutions, have begun to charge fees to our customers more regularly, customers may prove unwilling to pay additional fees, even in exchange for more attractive value-added services, and their reluctance to do so would adversely affect the implementation of our strategy to increase our fee income. Furthermore, the fees that we charge to customers are subject to regulation by Korean financial regulatory authorities, which may seek to implement regulations or measures that may have an adverse impact on our ability to achieve this aspect of our strategy.

Risks relating to competition

Competition in the Korean financial industry is intense, and we may lose market share and experience declining margins as a result.

Competition in the Korean financial market has been and is likely to remain intense. Some of the financial institutions that we compete with are larger in terms of asset size and customer base and have longer operating histories as financial holding companies, greater financial resources or more specialized capabilities than us and our subsidiaries. In addition, in the area of our core banking operations, most Korean banks have been focusing on retail customers and small- and medium-sized enterprises in recent years, although they have begun to generally increase their exposure to large corporate borrowers, and have been focusing on developing fee income businesses as increasingly important sources of revenue. In the area of credit cards, increased competition in the payments market and the resulting increase in our marketing activities, as well as the general trend towards lower merchant fees, are adversely affecting profits in the segment. In our new capital segment, our profitability may be adversely affected by increasing competition in the automobile finance and lease finance markets. The competition and market saturation resulting from this common focus may make it more difficult for us to secure retail, small- and medium-sized enterprise and large corporate customers with the credit quality and on credit terms necessary to maintain or increase our income and profitability.

In addition, the introduction of Internet-only banks in Korea is expected to increase competition in the Korean banking industry. Internet-only banks generally operate without branches and conduct most of their operations through electronic means, which enable them to minimize costs and offer customers higher interest rates on deposits or lower lending rates. In April 2017, Kbank, the first Internet-only bank in Korea, in which Woori Bank owns 12.6% of the equity with voting rights as of December 31, 2022, commenced operations. Kakao Bank and Toss Bank, both mobile-only banks, commenced operations in July 2017 and October 2021, respectively.

13

Table of Contents

Furthermore, the following general regulatory reforms in the Korean financial industry have increased competition among banks and other financial institutions in Korea:

| • | In the second half of 2015, the Korean government implemented measures to facilitate bank account portability of retail customers by requiring commercial banks to establish systems that allow retail customers to easily switch their bank accounts at one commercial bank to another and automatically transfer the automatic payment settings of their former accounts to the new ones. |

| • | In March 2016, the Financial Services Commission introduced an individual savings account scheme in Korea, which enables individuals to efficiently manage a wide range of retail investment vehicles, including cash deposits, investment funds and securities investment products, from a single integrated account with one financial institution and offers tax benefits on investment returns. Since the scheme backed by the Korean government allows only one individual savings account per person, financial institutions have been competing to retain existing customers and attract new customers since the launch of the individual savings account scheme. Over 30 financial institutions, including banks, securities companies and insurance companies, have registered with the Financial Services Commission to sell their individual savings account products, and we expect fierce competition among these institutions. |

| • | In April 2019, the Financial Services Commission approved and is currently conducting test procedures for a financial regulatory sandbox, a framework set up to allow financial services providers to test new business models in a less regulated environment, as part of its efforts to work closely with the fintech sector and provide support to facilitate its development. A variety of financial services have been similarly approved for such testing under the financial regulatory sandbox. |

| • | In December 2019, the Financial Services Commission launched an “open banking” system, which allows customers to view banking account information and make wire transfers, regardless of institution, through a single mobile application. This integrated system is expected to allow fintech firms to share payment networks with banks, thereby lowering transaction fees and encouraging the development of new payment services. |

| • | In August 2020, amendments to the Credit Information Use and Protection Act established the framework for MyData services in Korea, which allow the collection of customers’ personal credit information from credit information providers/users or public institutions upon the customer’s request and subject to compliance requirements, so that customers may access such collected personal credit information in whole or in part. In January 2021, the Financial Services Commission granted licenses to 28 companies to operate as MyData service providers, 14 of which were fintech firms. Competition between traditional financial institutions and fintech firms is expected to intensify, particularly with respect to the relevant asset management services. As of December 31, 2022, 64 companies, including 23 fintech companies, have been granted a MyData license. MyData services are currently offered through Woori WON Banking, Woori Bank’s main mobile banking application, as well as through Woori Card’s mobile application. |

| • | In March 2023, the Financial Services Commission and the Financial Supervisory Service jointly hosted the initial working group meeting of a task force committed to improving the management and operating practices of banks and banking system. One of the goals of the task force is to promoting competition in the banking sector. During the initial working group meeting, authorities discussed ways to allow entry of new banks and boost competition between banks and nonbanks. These measures under discussion include, without limitation, (1) introducing small licensing units and small-scale specialized banks, (2) allowing entry of additional internet-only banks, regional banks and nation-wide banks, (3) converting mutual savings banks into regional banks and regional banks into nation-wide banks, (4) allowing credit card companies to provide comprehensive payment settlement services, (5) allowing securities firms to provide payment settlement services to corporate entities, (6) permitting insurance companies to concurrently operate payment settlement services, (7) expanding banks’ loans to small and medium-sized enterprises and small-loans to lower-income groups, and (8) extending nonbanks’ scope of services in handling policy fund loans and policy mortgages. The task force has held and will hold |

14

Table of Contents

| future working group meetings to discuss these issues and we expect that they will develop specific measures to increase competition in the banking sector in the near future. In addition, in February 2023, the Korea Fair Trade Commission conducted on-site examinations of the major banks, including us, to determine whether the banks have engaged in unfair trade practices. |

Overall, we expect that such measures may not only intensify competition among traditional financial institutions in Korea, but also allow new market participants such as fintech firms to potentially gain market share in certain areas in which we operate.

The Korean financial industry is undergoing significant consolidation through which the number of nationwide commercial banks in Korea has significantly decreased since the financial crisis in Korea in the late 1990s. A number of significant mergers and acquisitions in the financial industry have also taken place in Korea in recent years, including the merger of Hana Bank into Korea Exchange Bank in 2015, KB Financial Group’s acquisition of Hyundai Securities Co., Ltd. in 2016 and the subsequent merger of Hyundai Securities with and into KB Investment & Securities Co., Ltd. in 2016. In 2016, Mirae Asset Securities Co., Ltd. acquired a 43% interest in KDB Daewoo Securities Co., Ltd., and subsequently merged with and into Mirae Asset Securities. In 2014, pursuant to the implementation of the Korean government’s privatization plan with respect to Woori Finance Holdings and its former subsidiaries, Woori Financial, Woori Asset Management and Woori F&I were acquired by KB Financial Group, Kiwoom Securities and Daishin Securities, respectively, and Woori Investment & Securities, Woori Aviva Life Insurance and Woori FG Savings Bank were acquired by NongHyup Financial Group. In addition, in October 2014, the KDIC’s ownership interest in Kwangju Bank and Kyongnam Bank were acquired by JB Financial Group and BNK Financial Group (formerly known as BS Financial Group), respectively. See “Item 4.A. History and Development of the Company—Privatization Plan.” In 2020, Hana Financial Group acquired The-K Non-Life Insurance Co., Ltd. to form Hana Insurance Co., Ltd. Orange Life Insurance, Ltd. (formerly known as ING Life Insurance Korea, Ltd.) became a wholly-owned subsidiary of Shinhan Financial Group following the acquisition of equity interests by Shinhan Financial Group in February 2019 and January 2020, which subsequently merged with and into Shinhan Life Insurance Co., Ltd. in July 2021. In 2020, Shinhan Financial Group acquired the venture capital firm Neoplux. In January 2022, Shinhan Financial Group’s subsidiary, Shinhan Asset Management Co., Ltd., merged with Shinhan Alternative Investment Management Inc. In July 2022, Shinhan Financial Group acquired BNP Paribas Cardif General Insurance, and established Shinhan EZ General Insurance. In 2020, KB Financial Group acquired The Prudential Life Insurance Company of Korea Ltd., which merged with KB Life Insurance in January 2023, with the surviving entity’s name changed to KB Life Insurance Co., Ltd.

We expect that consolidation in the Korean financial industry will continue. Other financial institutions may seek to acquire or merge with other entities, and the financial institutions resulting from such consolidation may, by virtue of their increased size and business scope, provide significantly greater competition for us. We also believe that foreign financial institutions, many of which have greater experience and resources than we do, may seek to compete with us in providing financial products and services either by themselves or in partnership with existing Korean financial institutions. Increased competition and continuing consolidation may lead to decreased margins, resulting in a material adverse impact on our future profitability. Accordingly, our results of operations and financial condition may suffer as a result of increasing competition in the Korean financial industry.

Competition for customer deposits may increase, resulting in a loss of our deposit customers or an increase in our funding costs.

In recent years, we have faced increasing pricing pressure on deposit products from our competitors. If we do not continue to offer competitive interest rates to our deposit customers, we may lose their business. In addition, even if we are able to match our competitors’ pricing, doing so may result in an increase in our funding costs, which may have an adverse impact on our results of operations.

15

Table of Contents

Other risks relating to our business

The COVID-19 pandemic has adversely affected and may continue to adversely affect our business, financial condition or results of operations.

COVID-19, an infectious disease caused by severe acute respiratory syndrome coronavirus 2, has spread globally and was declared a “pandemic” by the World Health Organization in March 2020. The global outbreak of COVID-19 has led to global economic and financial disruptions and has adversely affected our business operations. We have been subjected to and remain subject to a number of related risks, including but not limited to:

| • | an increase in defaults on loan payments from our customers who may not be able to meet payment obligations, which may lead to an increase in delinquency ratios and a deterioration in asset quality, resulting in increased charge-offs, higher provisioning and reduced interest and fee income; |

| • | decreases in interest rates followed by recent increases in interest rates worldwide (see “—An increase in interest rates would decrease the value of our debt securities portfolio and raise our funding costs while reducing loan demand and the repayment ability of our borrowers, which could adversely affect us”); |

| • | depreciation of the Won against major foreign currencies, which may increase our costs in servicing foreign currency-denominated debt and result in foreign exchange losses (see “—Unfavorable changes in the global financial markets could adversely affect our results of operations and financial condition”); |

| • | impairments in the fair value of our investments in companies that may be adversely affected by the pandemic; |

| • | disruption in the normal operations of our business resulting from the contraction of the disease by our employees or customers, which may necessitate our employees to be quarantined and/or our offices or branches to be temporarily shut down; and |

| • | disruption resulting from the necessity for social distancing, including, for example, temporary arrangements for employees to work remotely, which may lead to a reduction in labor productivity. |

The impact of the COVID-19 outbreak had a negative impact on our results of operations in 2022 and may continue to do so in the future, but it is not possible to predict the duration or the full magnitude of the overall harm that may result from the COVID-19 outbreak in the long term.

In addition, in response to the outbreak, Korean financial regulatory authorities, including the Financial Services Commission and the Financial Supervisory Service, have adopted policies for Korean banks to provide relief or assistance to customers. For example, the Korean government has implemented policies to extend loan terms and defer payments on interest and principal with respect to certain borrowers. In particular, in April 2020, the Korean government established the “COVID-19 SME and Small Merchant Financial Support Program” for small- and medium-sized enterprises and small merchants that are in good standing and have been negatively impacted by the COVID-19 pandemic (which excludes consumer loans and loans relating to the sale or leasing of real estate). As of December 31, 2022, our total loans (including payment guarantees) subject to this program amounted to ₩2,177 billion. Although the program was originally scheduled to expire in September 2021, it has been extended four times before being terminated in September 2022.

On October 4, 2022, Woori Bank started to operate a deferment program similar to the “COVID-19 SME and Small Merchant Financial Support Program”. Under this deferment program, with respect to loans made to borrowers which have been adversely impacted by the COVID-19 pandemic (excluding loans related to the sale or lease of real property and loans made to borrowers engaged in certain unwholesome businesses), Woori Bank may extend their maturity date up until September 30, 2025, and may defer the borrowers’ payment obligation for the interests and principal of such loans up until September 2023. In October 2022, the Korean government also launched the New Start Fund, a debt adjustment program, under which pandemic-hit micro-enterprises and self-employed business owners can apply for debt adjustment, and once accepted, will be supported through

16

Table of Contents

customized debt adjustment plans according to their respective credit conditions and types of loans. Under the New Start Fund program, the Korean government may purchase the loan directly and then make adjustment, or if the relevant financial institution agrees, allow the relevant financial institution to restructure the loan directly. See “—Risks relating to our corporate credit portfolio—The largest portion of our credit exposure is to small- and medium-sized enterprises, and financial difficulties experienced by companies in this segment may result in a deterioration of our asset quality and have an adverse impact on us.”

We and our subsidiaries have also implemented additional measures, both financial, such as offering discounts on the interest rates of certain loans and waiving ATM transaction fees in certain areas in Korea affected by COVID-19, and non-financial, such as installing acrylic transparent barriers in our branches and distributing masks to protect our customers and workforce. We have also established a group emergency management committee to accurately assess the relevant risks, proactively develop countermeasures and enhance reporting and communication systems on a group-wide basis. Notwithstanding such efforts, in the event that COVID-19 or other types of widespread infectious diseases cannot be effectively and timely contained, our business, financial condition, results of operations and cash flows may continue to be adversely affected.

Unfavorable changes in the global financial markets could adversely affect our results of operations and financial condition.

The overall prospects for the Korean and global economy in 2023 and beyond remain uncertain. In recent years, the global financial markets have experienced significant volatility as a result of, among other things:

| • | the occurrence of severe health epidemics, such as the COVID-19 pandemic; |

| • | hostilities, political or social tensions involving Russia (including the invasion of Ukraine by Russia and ensuing actions that the United States and other countries have taken or may take in the future) and the resulting adverse effects on the global supply of oil and other natural resources and the global financial markets; |

| • | interest rate fluctuations as well as changes in policy rates by the U.S. Federal Reserve and other central banks, a rise in inflation rates and volatility in stock markets and exchange rates worldwide; |

| • | financial and social difficulties affecting many countries worldwide, in particular in Latin America and Europe; |

| • | adverse developments in the financial markets and industry, in particular those faced by several banks in the United States and Europe; |

| • | a deterioration in economic and trade relations between the United States and its major trading partners, including China; |

| • | escalations in trade protectionism globally and geopolitical tensions in East Asia and the Middle East; |

| • | the slowdown of economic growth in China and other major emerging market economies; and |

| • | political and social instability in various countries in the Middle East, including Iran, Syria, Iraq and Egypt. |

In light of the high level of interdependence of the global economy, unfavorable changes in the global financial markets, including as a result of any of the foregoing developments, could have a material adverse effect on the Korean economy and financial markets, and in turn on our business, financial condition and results of operations.

We are also exposed to adverse changes and volatility in the global and Korean financial markets as a result of our liabilities and assets denominated in foreign currencies and our holdings of trading and investment securities, including structured products. The value of the Won relative to major foreign currencies in general and the U.S. dollar in particular has fluctuated widely in recent years and has been subject to significant volatility as a result of the COVID-19 pandemic, the invasion of Ukraine by Russia and the ensuing sanctions against Russia

17

Table of Contents

and, more recently, the widening difference in policy rates between the United States and Korea. A depreciation of the Won will increase our cost of servicing our foreign currency-denominated debt, while continued exchange rate volatility may also result in foreign exchange losses for us. Furthermore, as a result of the deterioration in global and Korean economic conditions, there has been downward pressure on securities prices, including the stock prices of Korean and foreign companies in which we hold an interest. Such developments have resulted in and may lead to further trading and valuation losses on our trading and investment securities portfolio as well as impairment losses on our investments in joint ventures and associates. See “—An increase in interest rates would decrease the value of our debt securities portfolio and raise our funding costs while reducing loan demand and the repayment ability of our borrowers, which could adversely affect us.”

Adverse developments affecting the financial services industry, including events or concerns involving liquidity of financial institutions, could adversely affect our business, financial condition or results of operations.