UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

COMMISSION FILE NUMBER 001-12307

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||

Registrant’s telephone number, including area code: (801 ) 844-8208

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbols | Name of Each Exchange on Which Registered | ||||||

| Depositary Shares each representing a 1/40th ownership interest in a share of: | ||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Number of common shares outstanding at April 30, 2024 147,654,732 shares

1

ZIONS BANCORPORATION, NATIONAL ASSOCIATION AND SUBSIDIARIES

Table of Contents

| Page | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

Table of Contents

ZIONS BANCORPORATION, NATIONAL ASSOCIATION AND SUBSIDIARIES

GLOSSARY OF ACRONYMS AND ABBREVIATIONS

| ACL | Allowance for Credit Losses | HECL | Home Equity Credit Line | ||||||||

| AFS | Available-for-Sale | HTM | Held-to-Maturity | ||||||||

| ALLL | Allowance for Loan and Lease Losses | IPO | Initial Public Offering | ||||||||

| Amegy | Amegy Bank, a division of Zions Bancorporation, National Association | LIHTC | Low-income Housing Tax Credit | ||||||||

| AOCI | Accumulated Other Comprehensive Income or Loss | Municipalities | State and Local Governments | ||||||||

| ASC | Accounting Standards Codification | NAICS | North American Industry Classification System | ||||||||

| ASU | Accounting Standards Update | NASDAQ | National Association of Securities Dealers Automated Quotations | ||||||||

| BOLI | Bank-Owned Life Insurance | NBAZ | National Bank of Arizona, a division of Zions Bancorporation, National Association | ||||||||

| bps | Basis Points | NIM | Net Interest Margin | ||||||||

| BTFP | Bank Term Funding Program | NM | Not Meaningful | ||||||||

| CB&T | California Bank & Trust, a division of Zions Bancorporation, National Association | NSB | Nevada State Bank, a division of Zions Bancorporation, National Association | ||||||||

| CLTV | Combined Loan-to-Value Ratio | OCC | Office of the Comptroller of the Currency | ||||||||

| CODM | Chief Operating Decision Maker | OCI | Other Comprehensive Income or Loss | ||||||||

| CRE | Commercial Real Estate | OREO | Other Real Estate Owned | ||||||||

| DTA | Deferred Tax Asset | PAM | Proportional Amortization Method | ||||||||

| DTL | Deferred Tax Liability | PEI | Private Equity Investment | ||||||||

| EaR | Earnings at Risk | PPNR | Pre-provision Net Revenue | ||||||||

| EPS | Earnings per Share | ROU | Right-of-Use | ||||||||

| EVE | Economic Value of Equity | RULC | Reserve for Unfunded Lending Commitments | ||||||||

| FASB | Financial Accounting Standards Board | S&P | Standard & Poor's | ||||||||

| FDIC | Federal Deposit Insurance Corporation | SBA | U.S. Small Business Administration | ||||||||

| FHLB | Federal Home Loan Bank | SBIC | Small Business Investment Company | ||||||||

| FICO | Fair Isaac Corporation | TCBW | The Commerce Bank of Washington, a division of Zions Bancorporation, National Association | ||||||||

| FRB | Federal Reserve Board | U.S. | United States | ||||||||

| FTP | Funds Transfer Pricing | Vectra | Vectra Bank Colorado, a division of Zions Bancorporation, National Association | ||||||||

| GAAP | Generally Accepted Accounting Principles | Zions Bank | Zions Bank, a division of Zions Bancorporation, National Association | ||||||||

| GCF | General Collateral Funding | ||||||||||

3

PART I. FINANCIAL INFORMATION

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FORWARD-LOOKING INFORMATION

This quarterly report includes “forward-looking statements” as that term is defined in the Private Securities Litigation Reform Act of 1995. These statements are based on management’s current expectations and assumptions regarding future events or determinations, all of which are subject to known and unknown risks, uncertainties, and other factors that may cause our actual results, performance or achievements, industry trends, and results or regulatory outcomes to differ materially from those expressed or implied. Forward-looking statements include, among others:

•Statements with respect to the beliefs, plans, objectives, goals, targets, commitments, designs, guidelines, expectations, anticipations, and future financial condition, results of operations and performance of Zions Bancorporation, National Association and its subsidiaries (collectively “Zions Bancorporation, N.A.,” “the Bank,” “we,” “our,” “us”); and

•Statements preceded or followed by, or that include the words “may,” “might,” “can,” “continue,” “could,” “should,” “would,” “believe,” “anticipate,” “estimate,” “forecasts,” “expect,” “intend,” “target,” “commit,” “design,” “plan,” “projects,” “will,” and the negative thereof and similar words and expressions.

Forward-looking statements are not guarantees, nor should they be relied upon as representing management’s views as of any subsequent date. Actual results and outcomes may differ materially from those presented. Although the following list is not comprehensive, important factors that may cause material differences include:

•The quality and composition of our loan and securities portfolios and the quality and composition of our deposits;

•Changes in general industry, political and economic conditions, including elevated inflation, economic slowdown or recession, or other economic challenges; changes in interest and reference rates, which could adversely affect our revenue and expenses, the value of assets and liabilities, and the availability and cost of capital and liquidity; deterioration in economic conditions that may result in increased loan and leases losses;

•The effects of newly enacted and proposed regulations affecting us and the banking industry, as well as changes and uncertainties in applicable laws, and fiscal, monetary, regulatory, trade, and tax policies, and actions taken by governments, agencies, central banks, and similar organizations, including those that result in decreases in revenue; increases in capital standards; and increases in insurance assessments and other bank expenses;

•Competitive pressures and other factors that may affect aspects of our business, such as pricing and demand for our products and services, and our ability to recruit and retain talent;

•The impact of technological advancements, digital commerce, artificial intelligence, and other innovations affecting the banking industry;

•Our ability to complete projects and initiatives and execute on our strategic plans, manage our risks, control compensation and other expenses, and achieve our business objectives;

•Our ability to develop and maintain technology, information security systems and controls designed to guard against fraud, cybersecurity, and privacy risks;

•Our ability to provide adequate oversight of our suppliers or prevent inadequate performance by third parties upon whom we rely for the delivery of various products and services;

•Natural disasters, pandemics, catastrophic events and other emergencies and incidents and their impact on our and our customer’s operations and business and communities, including the increasing difficulty in, and the expense of, obtaining adequate insurance at reasonable prices;

4

•Governmental and social responses to environmental, social, and governance issues, including those with respect to climate change;

•Securities and capital markets behavior, including volatility and changes in market liquidity and our ability to raise capital;

•The possibility that our recorded goodwill could become impaired, which may have an adverse impact on our earnings and shareholders’ equity, but not on our regulatory capital;

•The impact of bank closures or adverse developments at other banks on general investor sentiment regarding the stability and liquidity of banks;

•Adverse news and other expressions of negative public opinion whether directed at us, other banks, the banking industry, or otherwise that may adversely affect our reputation and that of the banking industry generally;

•Protracted congressional negotiations and political stalemates regarding government funding and other issues, including those that increase the possibility of government shutdowns, downgrades in United States (“U.S.”) credit ratings, or other economic disruptions; and

•The effects of wars and geopolitical conflicts, such as the ongoing war between Russia and Ukraine, the war in the Middle East, and other local, national, or international disasters, crises, or conflicts that may occur in the future.

We caution against the undue reliance on forward-looking statements, which reflect our views only as of the date they are made. Except to the extent required by law, we specifically disclaim any obligation to update any factors or to publicly announce the revisions to any forward-looking statements to reflect future events or developments.

RESULTS OF OPERATIONS

Comparisons noted below are calculated for the current quarter compared with the same prior year period unless otherwise specified. Growth rates of 100% or more are considered not meaningful (“NM”) as they generally reflect a low starting point.

First Quarter 2024 Financial Performance

| Net Earnings Applicable to Common Shareholders (in millions) | Diluted EPS | Adjusted PPNR (in millions) | Efficiency Ratio | |||||||||||||||||

5

Executive Summary

Our financial results in the first quarter of 2024 reflected low net charge-offs, reduced net interest income, loan growth, and sequential improvement of the net interest margin (“NIM”). Diluted earnings per share (“EPS”) was $0.96, compared with $1.33 in the first quarter of 2023, as lower revenue and slightly higher noninterest expense was partially offset by a lower provision for credit losses.

•Net interest income decreased $93 million, or 14%, relative to the prior year period, as higher funding costs more than offset higher earning asset yields. The net interest margin was 2.94%, compared with 3.33%, and was up from 2.91% in the fourth quarter of 2023. Net interest income was also impacted by reduced interest-earning assets and an increase in interest-bearing liabilities.

◦Average interest-earning assets decreased $2.2 billion, or 3%, driven by declines in average securities and average money market investments, partially offset by an increase in average loans and leases.

◦Total loans and leases increased $1.8 billion, or 3%, primarily due to growth in the consumer 1-4 family residential mortgage and commercial real estate (“CRE”) multi-family and industrial construction loan portfolios.

◦Average interest-bearing liabilities increased $6.0 billion, or 12%, driven by an increase in average interest-bearing deposits, partially offset by a decline in average borrowed funds.

◦Total deposits increased $5.0 billion, or 7%, as an increase in interest-bearing deposits was partially offset by a decrease in noninterest-bearing demand deposits. Customer deposits (excluding brokered deposits) totaled $69.9 billion, compared with $63.8 billion at March 31, 2023, and included approximately $7.5 billion of reciprocal deposits at March 31, 2024.

•The provision for credit losses was $13 million, compared with $45 million in the prior year period.

•Customer-related noninterest income remained flat at $151 million, as an increase in capital markets fees was offset by a decrease in loan-related fees and income. Decreases in noncustomer-related noninterest income were due largely to higher mark-to-market valuation adjustments related to servicing rights in the prior year quarter, a decrease in dividends on Federal Home Loan Bank (“FHLB”) stock, and a valuation loss associated with one of our equity investments in the current period.

•Noninterest expense increased $14 million, or 3%, driven largely by an increase in deposit insurance and regulatory expense, which included a $13 million accrual associated with an updated special assessment estimate by the Federal Deposit Insurance Corporation (“FDIC”) during the quarter. This increase was partially offset by a decrease in salaries and employee benefits expense, primarily due to a decline in incentive compensation accruals.

•Net loan and lease charge-offs totaled $6 million, or 0.04% of average loans, compared with zero net charge-offs in the prior year quarter. Classified loans increased $54 million, or 6%. Nonperforming assets increased to $254 million, or 0.44%, compared with $173 million, or 0.31%, of loans and leases, primarily due to a small number of loans in the commercial and industrial and term commercial real estate portfolios.

•Total borrowed funds, consisting primarily of secured borrowings, decreased $7.3 billion, or 57%, from the prior year quarter, due largely to an increase in interest-bearing deposits and a decrease in interest-earning assets.

6

Net Interest Income and Net Interest Margin

NET INTEREST INCOME AND NET INTEREST MARGIN

| Three Months Ended March 31, | Amount change | Percent change | |||||||||||||||||||||

| (Dollar amounts in millions) | 2024 | 2023 | |||||||||||||||||||||

Interest and fees on loans 1 | $ | 865 | $ | 726 | $ | 139 | 19 | % | |||||||||||||||

| Interest on money market investments | 47 | 57 | (10) | (18) | |||||||||||||||||||

| Interest on securities | 142 | 137 | 5 | 4 | |||||||||||||||||||

Total interest income | 1,054 | 920 | 134 | 15 | |||||||||||||||||||

| Interest on deposits | 376 | 82 | 294 | NM | |||||||||||||||||||

| Interest on short- and long-term borrowings | 92 | 159 | (67) | (42) | |||||||||||||||||||

Total interest expense | 468 | 241 | 227 | 94 | |||||||||||||||||||

Net interest income | $ | 586 | $ | 679 | $ | (93) | (14) | % | |||||||||||||||

| Average interest-earning assets | $ | 81,613 | $ | 83,832 | $ | (2,219) | (3) | % | |||||||||||||||

| Average interest-bearing liabilities | $ | 55,043 | $ | 49,012 | $ | 6,031 | 12 | % | |||||||||||||||

| bps | |||||||||||||||||||||||

Yield on interest-earning assets 2 | 5.25 | % | 4.49 | % | 76 | ||||||||||||||||||

Rate paid on total deposits and interest-bearing liabilities 2 | 2.34 | % | 1.17 | % | 117 | ||||||||||||||||||

Cost of total deposits 2 | 2.06 | % | 0.47 | % | 159 | ||||||||||||||||||

Net interest margin 2 | 2.94 | % | 3.33 | % | (39) | ||||||||||||||||||

1 Includes interest income recoveries of $2 million for both the three months ended March 31, 2024, and 2023.

2 Taxable-equivalent rates used where applicable.

Net interest income accounted for approximately 79% of our net revenue (net interest income plus noninterest income) for the current quarter and decreased $93 million, or 14%, relative to the prior year quarter, as higher funding costs more than offset higher earning asset yields. The NIM was 2.94%, compared with 3.33%, and was up from 2.91% in the fourth quarter of 2023.

The yield on average interest-earning assets was 5.25% in the first quarter of 2024, an increase of 76 basis points (“bps”), reflecting higher interest rates and a favorable mix change to higher-yielding assets. The yield on average loans and leases increased 76 bps to 6.06%, and the yield on average securities increased 38 bps to 2.84% in the first quarter of 2024.

The rate paid on total deposits and interest-bearing liabilities was 2.34%, compared with 1.17% in the prior year quarter, and the cost of total deposits was 2.06%, compared with 0.47%, also reflecting the higher interest rate environment as well as reduced noninterest-bearing deposits.

Net interest income was also impacted by reduced interest-earning assets and an increase in interest-bearing liabilities. Average interest-earning assets decreased $2.2 billion, or 3%, from the prior year quarter, driven by declines of $2.5 billion and $1.5 billion in average securities and average money market investments, respectively. The decrease in average securities was primarily due to principal reductions. These decreases were partially offset by an increase of $1.8 billion in average loans and leases.

Average interest-bearing liabilities increased $6.0 billion, or 12%, from the prior year quarter, driven by an increase of $12.0 billion in average interest-bearing deposits, as customers moved from noninterest-bearing to interest-bearing products in response to the higher interest rate environment. This increase was partially offset by a decrease of $6.0 billion in average borrowed funds.

7

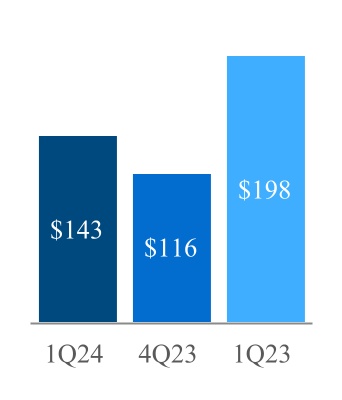

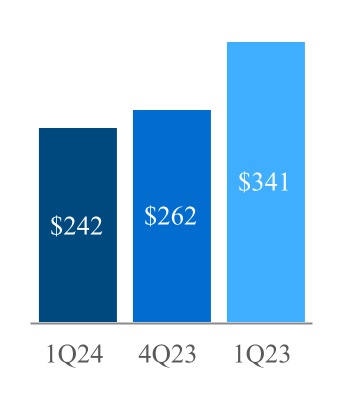

The following charts further illustrate the changes in average interest-earning assets and average interest-bearing liabilities:

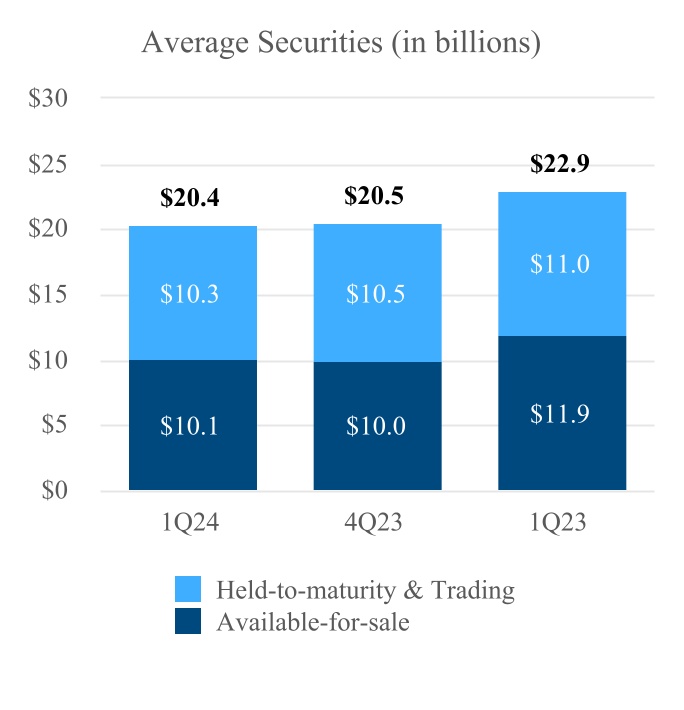

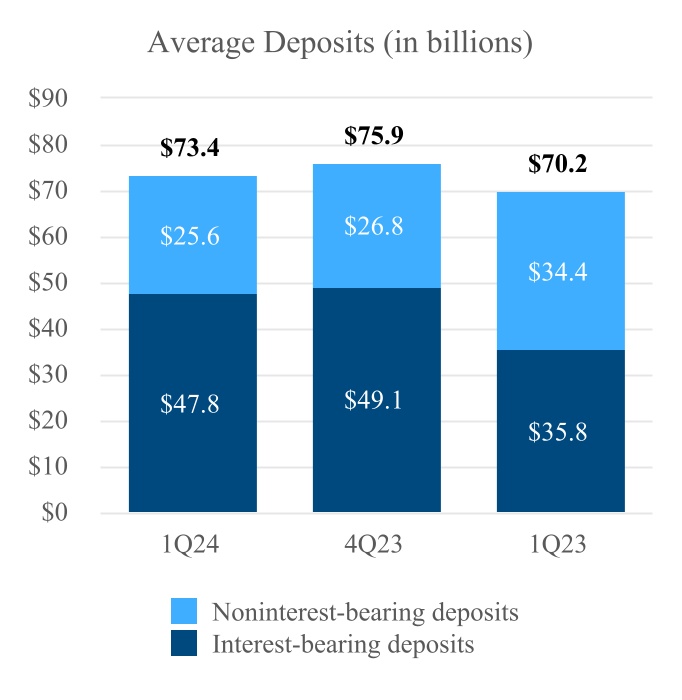

Average loans and leases increased $1.8 billion, or 3%, to $57.9 billion, primarily due to growth in average consumer and commercial real estate loans. Average securities decreased $2.5 billion, or 11%, to $20.4 billion, primarily due to available-for-sale (“AFS”) securities principal reductions.

8

Average deposits increased $3.2 billion, or 5%, to $73.4 billion at an average cost of 2.06%, from $70.2 billion at an average cost of 0.47% in the first quarter of 2023. Average noninterest-bearing deposits as a percentage of total deposits decreased to 35%, compared with 49% during the same prior year period. The loan-to-deposit ratio was 78%, compared with 81% in the prior year quarter.

Average borrowed funds, consisting primarily of secured borrowings, decreased $6.0 billion, or 45%, to $7.2 billion, due largely to an increase in interest-bearing deposits and a decrease in interest-earning assets.

For more information on our investment securities portfolio and borrowed funds and how we manage liquidity risk, refer to the “Investment Securities Portfolio” section on page 15 and the “Liquidity Risk Management” section on page 31. For further discussion of the effects of market rates on net interest income and how we manage interest rate risk, refer to the “Interest Rate and Market Risk Management” section on page 28.

The following schedule summarizes the average balances, the amount of interest earned or paid, and the applicable yields for interest-earning assets and the costs of interest-bearing liabilities:

9

CONSOLIDATED AVERAGE BALANCE SHEETS, YIELDS AND RATES

| (Unaudited) | Three Months Ended March 31, 2024 | Three Months Ended March 31, 2023 | |||||||||||||||||||||||||||||||||

| (Dollar amounts in millions) | Average balance | Interest | Yield/ Rate 1 | Average balance | Interest | Yield/ Rate 1 | |||||||||||||||||||||||||||||

| ASSETS | |||||||||||||||||||||||||||||||||||

| Money market investments: | |||||||||||||||||||||||||||||||||||

| Interest-bearing deposits | $ | 1,447 | $ | 20 | 5.71 | % | $ | 2,724 | $ | 31 | 4.72 | % | |||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell | 1,826 | 27 | 5.89 | 2,081 | 26 | 5.02 | |||||||||||||||||||||||||||||

| Total money market investments | 3,273 | 47 | 5.81 | 4,805 | 57 | 4.85 | |||||||||||||||||||||||||||||

| Securities: | |||||||||||||||||||||||||||||||||||

| Held-to-maturity | 10,277 | 57 | 2.25 | 11,024 | 62 | 2.28 | |||||||||||||||||||||||||||||

| Available-for-sale | 10,067 | 86 | 3.45 | 11,824 | 76 | 2.62 | |||||||||||||||||||||||||||||

| Trading | 33 | — | 4.27 | 21 | — | 4.01 | |||||||||||||||||||||||||||||

Total securities | 20,377 | 143 | 2.84 | 22,869 | 138 | 2.46 | |||||||||||||||||||||||||||||

| Loans held for sale | 56 | 1 | 6.80 | 5 | — | 0.26 | |||||||||||||||||||||||||||||

Loans and leases: 2 | |||||||||||||||||||||||||||||||||||

| Commercial | 30,482 | 451 | 5.95 | 30,678 | 381 | 5.03 | |||||||||||||||||||||||||||||

| Commercial real estate | 13,504 | 245 | 7.29 | 12,876 | 209 | 6.59 | |||||||||||||||||||||||||||||

| Consumer | 13,921 | 177 | 5.10 | 12,599 | 144 | 4.62 | |||||||||||||||||||||||||||||

| Total loans and leases | 57,907 | 873 | 6.06 | 56,153 | 734 | 5.30 | |||||||||||||||||||||||||||||

| Total interest-earning assets | 81,613 | 1,064 | 5.25 | 83,832 | 929 | 4.49 | |||||||||||||||||||||||||||||

| Cash and due from banks | 710 | 543 | |||||||||||||||||||||||||||||||||

| Allowance for credit losses on loans and debt securities | (685) | (576) | |||||||||||||||||||||||||||||||||

| Goodwill and intangibles | 1,058 | 1,064 | |||||||||||||||||||||||||||||||||

| Other assets | 5,274 | 5,624 | |||||||||||||||||||||||||||||||||

| Total assets | $ | 87,970 | $ | 90,487 | |||||||||||||||||||||||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||||||||||||||||||||||||||

| Interest-bearing deposits: | |||||||||||||||||||||||||||||||||||

| Savings and money market | $ | 38,044 | $ | 259 | 2.73 | % | $ | 32,859 | $ | 62 | 0.77 | % | |||||||||||||||||||||||

| Time | 9,777 | 117 | 4.81 | 2,934 | 20 | 2.68 | |||||||||||||||||||||||||||||

| Total interest-bearing deposits | 47,821 | 376 | 3.16 | 35,793 | 82 | 0.92 | |||||||||||||||||||||||||||||

| Borrowed funds: | |||||||||||||||||||||||||||||||||||

Federal funds and security repurchase agreements | 1,748 | 23 | 5.38 | 5,614 | 64 | 4.65 | |||||||||||||||||||||||||||||

| Other short-term borrowings | 4,931 | 61 | 4.98 | 6,952 | 84 | 4.89 | |||||||||||||||||||||||||||||

| Long-term debt | 543 | 8 | 5.99 | 653 | 11 | 6.85 | |||||||||||||||||||||||||||||

| Total borrowed funds | 7,222 | 92 | 5.15 | 13,219 | 159 | 4.88 | |||||||||||||||||||||||||||||

| Total interest-bearing liabilities | 55,043 | 468 | 3.42 | 49,012 | 241 | 1.99 | |||||||||||||||||||||||||||||

| Noninterest-bearing demand deposits | 25,537 | 34,363 | |||||||||||||||||||||||||||||||||

| Other liabilities | 1,661 | 2,058 | |||||||||||||||||||||||||||||||||

| Total liabilities | 82,241 | 85,433 | |||||||||||||||||||||||||||||||||

| Shareholders’ equity: | |||||||||||||||||||||||||||||||||||

| Preferred equity | 440 | 440 | |||||||||||||||||||||||||||||||||

| Common equity | 5,289 | 4,614 | |||||||||||||||||||||||||||||||||

| Total shareholders’ equity | 5,729 | 5,054 | |||||||||||||||||||||||||||||||||

| Total liabilities and shareholders’ equity | $ | 87,970 | $ | 90,487 | |||||||||||||||||||||||||||||||

| Spread on average interest-bearing funds | 1.83 | % | 2.50 | % | |||||||||||||||||||||||||||||||

| Net impact of noninterest-bearing sources of funds | 1.11 | % | 0.83 | % | |||||||||||||||||||||||||||||||

Net interest margin | $ | 596 | 2.94 | % | $ | 688 | 3.33 | % | |||||||||||||||||||||||||||

Memo: total cost of deposits | 2.06 | % | 0.47 | % | |||||||||||||||||||||||||||||||

| Memo: total deposits and interest-bearing liabilities | $ | 80,580 | 468 | 2.34 | % | $ | 83,375 | 241 | 1.17 | % | |||||||||||||||||||||||||

1 Taxable-equivalent rates used where applicable.

2 Net of unamortized purchase premiums, discounts, and deferred loan fees and costs.

10

Provision for Credit Losses

The allowance for credit losses (“ACL”) is the combination of both the allowance for loan and lease losses (“ALLL”) and the reserve for unfunded lending commitments (“RULC”). The ALLL represents the estimated current expected credit losses related to the loan and lease portfolio as of the balance sheet date. The RULC represents the estimated reserve for current expected credit losses associated with off-balance sheet commitments. Changes in the ALLL and RULC, net of charge-offs and recoveries, are recorded as the provision for loan and lease losses and the provision for unfunded lending commitments, respectively, on the consolidated statement of income. The ACL for debt securities is estimated separately from loans and is included in “Investment securities” on the consolidated balance sheet.

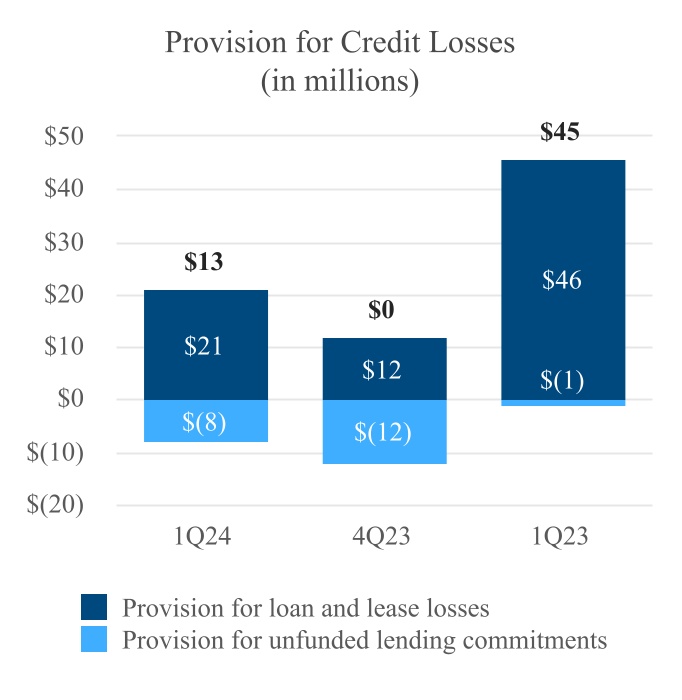

The provision for credit losses, which is the combination of both the provision for loan and lease losses and the provision for unfunded lending commitments, was $13 million, compared with $45 million in the first quarter of 2023.

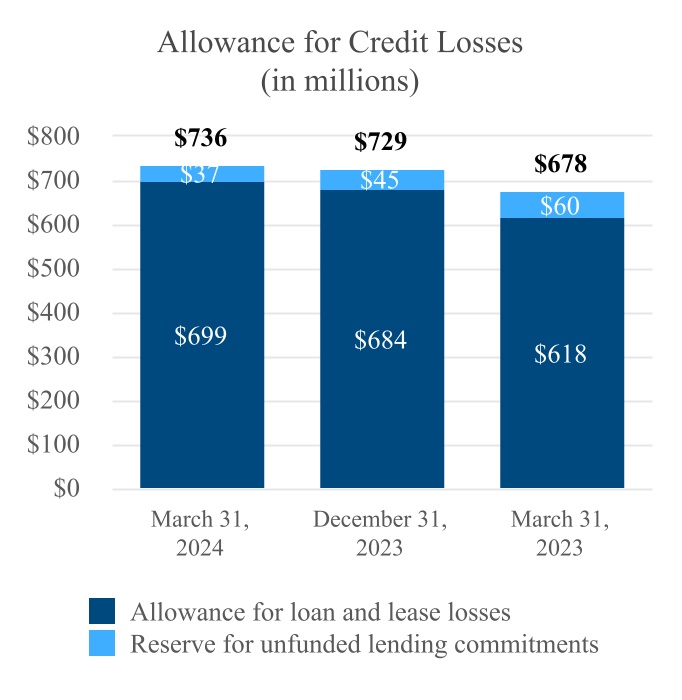

The ACL was $736 million at March 31, 2024, compared with $678 million at March 31, 2023. The increase in the ACL primarily reflects incremental reserves associated with portfolio-specific risks including commercial real estate and modest deterioration in credit quality, partially offset by improvements in economic forecasts. The ratio of ACL to total loans and leases was 1.27% and 1.20% at March 31, 2024 and 2023, respectively. The provision for securities losses was less than $1 million during both the first quarter of 2024 and 2023.

11

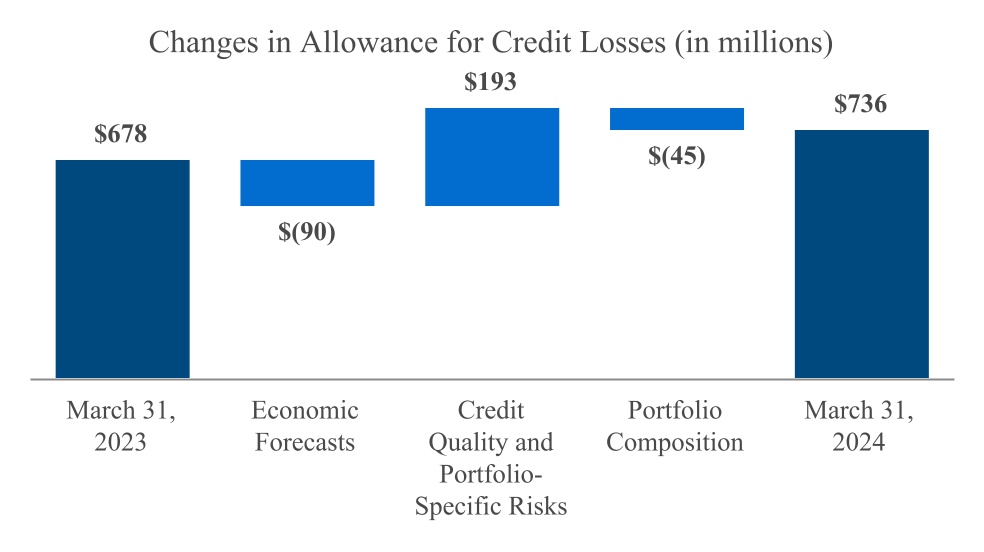

The bar chart above illustrates the broad categories of change in the ACL from the prior year period. To estimate current expected losses, we use econometric loss models that include multiple economic scenarios that reflect optimistic, baseline, and stressed economic conditions. The results derived using these economic scenarios are weighted to produce the credit loss estimate. Management may adjust the weights to reflect their assessment of current conditions and reasonable and supportable forecasts. The second bar represents changes in these economic forecasts and current economic conditions, including management's judgment of the weighting of the economic forecasts. These changes contributed to a $90 million decrease in the ACL from the prior year quarter.

The third bar represents changes in credit quality factors and includes risk-grade migration, portfolio-specific risks, and specific reserves against loans, which, when combined, contributed to a $193 million increase in the ACL, driven largely by an increased focus on certain portfolio-specific risks, including commercial real estate.

The fourth bar represents changes in our loan portfolio composition, including changes in loan balances, the aging of the portfolio, and other qualitative risk factors; all of which contributed to a $45 million decrease in the ACL.

See “Credit Risk Management” on page 20 and Note 6 in our 2023 Form 10-K for more information on how we determine the appropriate level of the ALLL and the RULC.

Noninterest Income

Noninterest income represents revenue earned from products and services that generally have no associated interest rate or yield and is classified as either customer-related or noncustomer-related. Customer-related noninterest income excludes items such as securities gains and losses, dividends, insurance-related income, and mark-to-market adjustments on certain derivatives.

Total noninterest income decreased $4 million, or 3%, relative to the prior year. Noninterest income accounted for approximately 21% and 19% of our net revenue (net interest income plus noninterest income) during the first quarter of 2024 and 2023, respectively. The following schedule presents a comparison of the major components of noninterest income:

12

NONINTEREST INCOME

| Three Months Ended March 31, | Amount change | Percent change | |||||||||||||||||||||

| (Dollar amounts in millions) | 2024 | 2023 | |||||||||||||||||||||

Commercial account fees | $ | 44 | $ | 43 | $ | 1 | 2 | % | |||||||||||||||

Card fees | 23 | 24 | (1) | (4) | |||||||||||||||||||

| Retail and business banking fees | 16 | 16 | — | — | |||||||||||||||||||

| Loan-related fees and income | 15 | 21 | (6) | (29) | |||||||||||||||||||

| Capital markets fees | 24 | 17 | 7 | 41 | |||||||||||||||||||

| Wealth management fees | 15 | 15 | — | — | |||||||||||||||||||

| Other customer-related fees | 14 | 15 | (1) | (7) | |||||||||||||||||||

Customer-related noninterest income | 151 | 151 | — | — | |||||||||||||||||||

| Fair value and nonhedge derivative income | 1 | (3) | 4 | NM | |||||||||||||||||||

| Dividends and other income (loss) | 6 | 11 | (5) | (45) | |||||||||||||||||||

| Securities gains (losses), net | (2) | 1 | (3) | NM | |||||||||||||||||||

| Noncustomer-related noninterest income | 5 | 9 | (4) | (44) | |||||||||||||||||||

Total noninterest income | $ | 156 | $ | 160 | $ | (4) | (3) | % | |||||||||||||||

Customer-related Noninterest Income

Customer-related noninterest income remained flat at $151 million. An increase in capital markets fees, driven largely by improved real estate capital markets and securities underwriting activity, was offset by a decrease in loan-related fees and income, primarily due to higher gains on loan sales in the prior year period and a decline in loan servicing income resulting from the sale of associated mortgage servicing rights in the third quarter of 2023.

Noncustomer-related Noninterest Income

Noncustomer-related noninterest income decreased $4 million from the prior year quarter. Dividends and other income decreased $5 million, primarily due to higher mark-to-market valuation adjustments related to servicing rights in the prior year quarter and a decrease in dividends on FHLB stock. Net securities gains decreased $3 million, due to a $4 million valuation loss associated with one of our equity investments in the current period. These decreases were offset by a $4 million increase in fair value and nonhedge derivative income, primarily due to credit valuation adjustments on client-related interest rate swaps.

Noninterest Expense

The following schedule presents a comparison of the major components of noninterest expense:

NONINTEREST EXPENSE

| Three Months Ended March 31, | Amount change | Percent change | |||||||||||||||||||||

| (Dollar amounts in millions) | 2024 | 2023 | |||||||||||||||||||||

| Salaries and employee benefits | $ | 331 | $ | 339 | $ | (8) | (2) | % | |||||||||||||||

| Technology, telecom, and information processing | 62 | 55 | 7 | 13 | |||||||||||||||||||

| Occupancy and equipment, net | 39 | 40 | (1) | (3) | |||||||||||||||||||

| Professional and legal services | 16 | 13 | 3 | 23 | |||||||||||||||||||

| Marketing and business development | 10 | 12 | (2) | (17) | |||||||||||||||||||

| Deposit insurance and regulatory expense | 34 | 18 | 16 | 89 | |||||||||||||||||||

| Credit-related expense | 7 | 6 | 1 | 17 | |||||||||||||||||||

| Other | 27 | 29 | (2) | (7) | |||||||||||||||||||

Total noninterest expense | $ | 526 | $ | 512 | $ | 14 | 3 | % | |||||||||||||||

Adjusted noninterest expense (non-GAAP) | $ | 511 | $ | 509 | $ | 2 | — | % | |||||||||||||||

13

Total noninterest expense increased $14 million, or 3%, relative to the prior year quarter. Deposit insurance and regulatory expense increased $16 million, driven largely by a $13 million accrual associated with an updated special assessment estimate by the FDIC during the current quarter, which was related to the bank closures in early 2023.

Technology, telecom, and information processing expense increased $7 million, or 13%, primarily due to increases in software amortization expenses associated with the replacement of our core loan and deposit banking systems, as well as other related application software, license, and maintenance expenses. Salaries and employee benefits expense decreased $8 million, or 2%, primarily due to a decline in incentive compensation accruals.

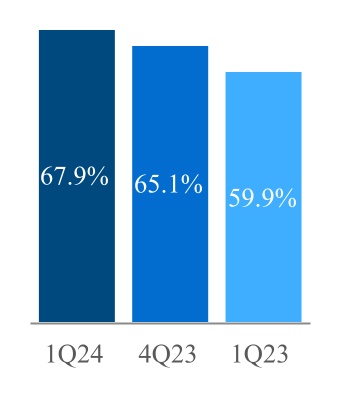

Adjusted noninterest expense remained relatively flat at $511 million. The efficiency ratio was 67.9%, compared with 59.9%, primarily due to a decline in adjusted taxable-equivalent revenue. For information on non-GAAP financial measures, see page 35.

Technology Spend

Consistent with our strategic objectives, we invest in technologies that will make us more efficient and enable us to remain competitive. We generally consider these investments as technology spend, which represents expenditures associated with technology-related investments, operations, systems, and infrastructure, and includes current period expenses presented on the consolidated statement of income, as well as capitalized investments, net of related amortization and depreciation, presented on the consolidated balance sheet. Technology spend is reported as a combination of the following:

•Technology, telecom, and information processing expense — includes expenses related to application software licensing and maintenance, related amortization, telecommunications, and data processing;

•Other technology-related expense — includes related noncapitalized salaries and employee benefits, occupancy and equipment, and professional and legal services; and

•Technology investments — includes capitalized technology infrastructure equipment, hardware, and purchased or internally developed software, less related amortization or depreciation.

The following schedule presents the composition of our technology spend:

TECHNOLOGY SPEND

| Three Months Ended March 31, | Amount change | Percent change | |||||||||||||||||||||

| (Dollar amounts in millions) | 2024 | 2023 | |||||||||||||||||||||

| Technology, telecom, and information processing expense | $ | 62 | $ | 55 | $ | 7 | 13 | % | |||||||||||||||

| Other technology-related expense | 60 | 54 | 6 | 11 | |||||||||||||||||||

| Technology investments | 15 | 26 | (11) | (42) | |||||||||||||||||||

| Less: related amortization and depreciation | (20) | (14) | (6) | 43 | |||||||||||||||||||

Total technology spend | $ | 117 | $ | 121 | $ | (4) | (3) | % | |||||||||||||||

Total technology spend decreased $4 million, or 3%, relative to the prior year quarter, as the aforementioned increase in technology, telecom, and information processing expense was offset by a decrease in certain technology investments, as the replacement of our core loan and deposit banking systems nears completion in 2024.

14

Income Taxes

The following schedule summarizes the income tax expense and effective tax rates for the periods presented:

INCOME TAXES

| Three Months Ended March 31, | |||||||||||

| (Dollar amounts in millions) | 2024 | 2023 | |||||||||

| Income before income taxes | $ | 203 | $ | 282 | |||||||

| Income tax expense | 50 | 78 | |||||||||

| Effective tax rate | 24.6 | % | 27.7 | % | |||||||

The effective tax rate was 24.6% and 27.7% for the three months ended March 31, 2024 and 2023, respectively. The higher effective tax rate in the prior year period was the result of a change in a discrete item that affected the reserve for uncertain tax positions. See Note 12 of the Notes to Consolidated Financial Statements for more information about the factors that impacted the income tax rates, as well as information about deferred income tax assets and liabilities.

Preferred Stock Dividends

Preferred stock dividends totaled $10 million and $6 million for the first quarter of 2024 and 2023, respectively. The increase was primarily due to changes in the timing and rates of dividend payments for certain series of preferred stock.

BALANCE SHEET ANALYSIS

Interest-Earning Assets

Interest-earning assets have associated interest rates or yields, and generally consist of loans and leases, securities, and money market investments. We strive to maintain a high level of interest-earning assets relative to total assets. For more information regarding the average balances, associated revenue generated, and the respective yields of our interest-earning assets, see the Consolidated Average Balance Sheet on page 10.

Investment Securities Portfolio

We invest in securities to actively manage liquidity and interest rate risk and to generate interest income. We primarily own securities that can readily provide us cash and liquidity through secured borrowing agreements without the need to sell the securities. Our fixed-rate securities portfolio helps balance the inherent interest rate mismatch between loans and deposits and protects the economic value of shareholders’ equity. At March 31, 2024, the estimated duration, which measures price sensitivity to interest rate changes, of our securities portfolio was 3.6 percent, unchanged from December 31, 2023.

For information about our borrowing capacity associated with the investment securities portfolio and how we manage our liquidity risk, refer to the “Liquidity Risk Management” section on page 31. See also Note 3 and Note 5 of the Notes to Consolidated Financial Statements for more information on fair value measurements and the accounting for our investment securities portfolio.

15

The following schedule presents the major components of our investment securities portfolio:

INVESTMENT SECURITIES PORTFOLIO

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||

| (In millions) | Par Value | Amortized cost | Fair value | Par Value | Amortized cost | Fair value | |||||||||||||||||||||||||||||

| Held-to-maturity | |||||||||||||||||||||||||||||||||||

| U.S. Government agencies and corporations: | |||||||||||||||||||||||||||||||||||

| Agency securities | $ | 92 | $ | 92 | $ | 85 | $ | 93 | $ | 93 | $ | 87 | |||||||||||||||||||||||

| Agency guaranteed mortgage-backed securities | 11,748 | 9,776 | 9,696 | 11,966 | 9,935 | 10,041 | |||||||||||||||||||||||||||||

| Municipal securities | 341 | 341 | 324 | 354 | 354 | 338 | |||||||||||||||||||||||||||||

| Total held-to-maturity | 12,181 | 10,209 | 10,105 | 12,413 | 10,382 | 10,466 | |||||||||||||||||||||||||||||

| Available-for-sale | |||||||||||||||||||||||||||||||||||

| U.S. Treasury securities | 585 | 584 | 481 | 585 | 585 | 492 | |||||||||||||||||||||||||||||

| U.S. Government agencies and corporations: | |||||||||||||||||||||||||||||||||||

| Agency securities | 634 | 629 | 596 | 669 | 663 | 630 | |||||||||||||||||||||||||||||

| Agency guaranteed mortgage-backed securities | 8,267 | 8,335 | 7,053 | 8,460 | 8,530 | 7,291 | |||||||||||||||||||||||||||||

| Small Business Administration loan-backed securities | 509 | 543 | 518 | 535 | 571 | 546 | |||||||||||||||||||||||||||||

| Municipal securities | 1,228 | 1,336 | 1,259 | 1,269 | 1,385 | 1,318 | |||||||||||||||||||||||||||||

| Other debt securities | 25 | 25 | 24 | 25 | 25 | 23 | |||||||||||||||||||||||||||||

| Total available-for-sale | 11,248 | 11,452 | 9,931 | 11,543 | 11,759 | 10,300 | |||||||||||||||||||||||||||||

| Total HTM and AFS investment securities | $ | 23,429 | $ | 21,661 | $ | 20,036 | $ | 23,956 | $ | 22,141 | $ | 20,766 | |||||||||||||||||||||||

The amortized cost of total held-to-maturity (“HTM”) and AFS investment securities decreased $480 million, or 2%, from December 31, 2023. Approximately 8% and 7% of the total HTM and AFS investment securities were floating-rate instruments at March 31, 2024 and December 31, 2023, respectively. Additionally, at March 31, 2024, we have $3.6 billion of pay-fixed swaps designated as fair value hedges against fixed-rate AFS securities that effectively convert the fixed interest income to a floating rate on the hedged portion of the securities. At March 31, 2024, total taxable-equivalent premium amortization for our investment securities was $17 million for the first quarter of 2024, compared with $26 million for the same prior year period.

In addition to HTM and AFS securities, we also have a trading securities portfolio, comprised of municipal securities, which totaled $59 million at March 31, 2024, compared with $48 million at December 31, 2023.

Refer to the “Interest Rate Risk Management” section on page 28, the “Capital Management” section on page 33, and Note 5 of the Notes to Consolidated Financial Statements for more discussion regarding our investment securities portfolio, swaps, and related unrealized gains and losses.

16

Municipal Investments and Extensions of Credit

We support our communities by providing products and services to state and local governments (“municipalities”), including deposit services, loans, and investment banking services. We also invest in securities issued by municipalities. Our municipal lending products generally include loans in which the debt service is repaid from general funds or pledged revenues of the municipal entity, or to private commercial entities or 501(c)(3) not-for-profit entities utilizing a pass-through municipal entity to achieve favorable tax treatment.

The following schedule summarizes our total investments and extensions of credit to municipalities:

MUNICIPAL INVESTMENTS AND EXTENSIONS OF CREDIT

| (In millions) | March 31, 2024 | December 31, 2023 | |||||||||

| Loans and leases | $ | 4,277 | $ | 4,302 | |||||||

| Held-to-maturity securities | 341 | 354 | |||||||||

| Available-for-sale securities | 1,259 | 1,318 | |||||||||

| Trading securities | 59 | 48 | |||||||||

| Unfunded lending commitments | 338 | 231 | |||||||||

Total | $ | 6,274 | $ | 6,253 | |||||||

Our municipal loans and securities are primarily associated with municipalities located within our geographic footprint. The municipal loan and lease portfolio is primarily secured by general obligations of municipal entities. Other types of collateral also include real estate, revenue pledges, or equipment. At March 31, 2024, we had no municipal loans on nonaccrual.

Municipal securities are internally graded, similar to loans, using risk-grading systems which vary based on the size and type of credit risk exposure. The internal risk grades assigned to our municipal securities follow our definitions of Pass, Special Mention, and Substandard, which are consistent with published definitions of regulatory risk classifications. At March 31, 2024, all municipal securities were graded as Pass. See Notes 5 and 6 of the Notes to Consolidated Financial Statements for additional information about the credit quality of these municipal loans and securities.

Loan and Lease Portfolio

We provide a wide range of lending products to commercial customers, generally small- and medium-sized businesses. We also provide various retail lending products and services to consumers and small businesses. The following schedule presents the composition of our loan and lease portfolio:

17

LOAN AND LEASE PORTFOLIO

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollar amounts in millions) | Amount | % of total loans | Amount | % of total loans | |||||||||||||||||||

| Commercial: | |||||||||||||||||||||||

| Commercial and industrial | $ | 16,519 | 28.4 | % | $ | 16,684 | 28.9 | % | |||||||||||||||

| Leasing | 388 | 0.7 | 383 | 0.7 | |||||||||||||||||||

| Owner-occupied | 9,295 | 16.0 | 9,219 | 16.0 | |||||||||||||||||||

| Municipal | 4,277 | 7.4 | 4,302 | 7.4 | |||||||||||||||||||

| Total commercial | 30,479 | 52.5 | 30,588 | 53.0 | |||||||||||||||||||

| Commercial real estate: | |||||||||||||||||||||||

| Construction and land development | 2,686 | 4.6 | 2,669 | 4.6 | |||||||||||||||||||

| Term | 10,892 | 18.7 | 10,702 | 18.5 | |||||||||||||||||||

| Total commercial real estate | 13,578 | 23.3 | 13,371 | 23.1 | |||||||||||||||||||

| Consumer: | |||||||||||||||||||||||

| Home equity credit line | 3,382 | 5.8 | 3,356 | 5.8 | |||||||||||||||||||

| 1-4 family residential | 8,778 | 15.1 | 8,415 | 14.6 | |||||||||||||||||||

| Construction and other consumer real estate | 1,321 | 2.3 | 1,442 | 2.5 | |||||||||||||||||||

| Bankcard and other revolving plans | 439 | 0.8 | 474 | 0.8 | |||||||||||||||||||

| Other | 132 | 0.2 | 133 | 0.2 | |||||||||||||||||||

| Total consumer | 14,052 | 24.2 | 13,820 | 23.9 | |||||||||||||||||||

| Total loans and leases | $ | 58,109 | 100.0 | % | $ | 57,779 | 100.0 | % | |||||||||||||||

At March 31, 2024 and December 31, 2023, the ratio of loans and leases to total assets was 67% and 66%, respectively. The largest loan category was commercial and industrial loans, which constituted 28% and 29% of our total loan portfolio for the same respective periods.

During the first three months of 2024, the loan and lease portfolio increased $330 million, or 1%, to $58.1 billion at March 31, 2024. Loan growth was driven largely by increases in consumer 1-4 family residential mortgage and term commercial real estate loans.

Other Noninterest-Bearing Investments

Other noninterest-bearing investments are equity investments that are held primarily for capital appreciation, dividends, or for certain regulatory requirements. The following schedule summarizes our related investments:

OTHER NONINTEREST-BEARING INVESTMENTS

| (Dollar amounts in millions) | March 31, 2024 | December 31, 2023 | Amount change | Percent change | |||||||||||||||||||

| Bank-owned life insurance | $ | 555 | $ | 553 | $ | 2 | — | % | |||||||||||||||

| Federal Home Loan Bank stock | 45 | 79 | (34) | (43) | |||||||||||||||||||

| Federal Reserve stock | 65 | 65 | — | — | |||||||||||||||||||

| Farmer Mac stock | 24 | 24 | — | — | |||||||||||||||||||

| SBIC investments | 196 | 190 | 6 | 3 | |||||||||||||||||||

| Other | 37 | 39 | (2) | (5) | |||||||||||||||||||

| Total other noninterest-bearing investments | $ | 922 | $ | 950 | $ | (28) | (3) | % | |||||||||||||||

Other noninterest-bearing investments decreased $28 million, or 3%, during the first three months of 2024, primarily due to a $34 million decrease in FHLB stock. We are required to invest approximately 4% of our FHLB borrowings in FHLB stock to maintain our borrowing capacity. The decrease in period-end FHLB activity stock was driven largely by an increase in interest-bearing deposits and a decrease in interest-earning assets.

18

Visa Class B Shares

In 2007, we received 460,153 non-transferable Class B shares of Visa, Inc. in connection with a restructuring and public offering by Visa U.S.A. These shares are carried at no cost on our consolidated balance sheet. In January 2024, Visa’s previously announced exchange offer proposal was approved by common stockholders, which resulted, among other actions, in a redenomination of all Visa Class B common shares to Class B-1 common shares. In April 2024, Visa commenced its exchange offer allowing Class B-1 shareholders the option to exchange up to 50% of their Class B-1 shares for shares that would be convertible into freely transferable Visa Class A common shares following a temporary restriction period. We did not participate in the exchange offer, which expired on May 3, 2024, in view of contingent obligations associated with certain make-whole provisions required as a condition of the exchange.

Premises, Equipment, and Software

We are in the final phase of a three-phase project to replace our core loan and deposit banking systems. This final phase includes the replacement of our deposit banking systems through multiple affiliate bank conversions. The first and second conversions were successfully completed in May 2023 and April 2024, respectively. We anticipate completing the migration of substantially all of the remaining accounts by late summer 2024.

The following schedule summarizes the capitalized costs associated with our core system replacement project, which are depreciated using a useful life of ten years:

CAPITALIZED COSTS ASSOCIATED WITH THE CORE SYSTEM REPLACEMENT PROJECT

| March 31, 2024 | |||||||||||||||||||||||

| (In millions) | Phase 1 | Phase 2 | Phase 3 | Total | |||||||||||||||||||

| Total amount of capitalized costs, less accumulated depreciation | $ | 19 | $ | 43 | $ | 228 | $ | 290 | |||||||||||||||

Deposits

Deposits are our primary funding source. The following schedule presents the composition of our deposit portfolio:

DEPOSIT PORTFOLIO

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollar amounts in millions) | Amount | % of total deposits | Amount | % of total deposits | |||||||||||||||||||

| Deposits by type | |||||||||||||||||||||||

| Noninterest-bearing demand | $ | 25,137 | 33.9 | % | $ | 26,244 | 35.0 | % | |||||||||||||||

| Interest-bearing: | |||||||||||||||||||||||

| Savings and money market | 38,835 | 52.3 | 38,663 | 51.6 | |||||||||||||||||||

| Time | 5,972 | 8.0 | 5,619 | 7.5 | |||||||||||||||||||

| Brokered | 4,293 | 5.8 | 4,435 | 5.9 | |||||||||||||||||||

| Total deposits | $ | 74,237 | 100.0 | % | $ | 74,961 | 100.0 | % | |||||||||||||||

| Deposit-related metrics | |||||||||||||||||||||||

| Estimated amount of insured deposits | $ | 42,192 | 57 | % | $ | 41,777 | 56 | % | |||||||||||||||

| Estimated amount of uninsured deposits | 32,045 | 43 | % | 33,184 | 44 | % | |||||||||||||||||

Estimated amount of collateralized deposits 1 | $ | 3,180 | 4 | % | $ | 3,979 | 5 | % | |||||||||||||||

| Loan-to-deposit ratio | 78% | 77% | |||||||||||||||||||||

1 Includes both insured and uninsured deposits.

Total deposits decreased $724 million, or 1%, from December 31, 2023. At March 31, 2024 and December 31, 2023, customer deposits (excluding brokered deposits) were $69.9 billion and $70.5 billion, and included approximately $7.5 billion and $6.8 billion, respectively, of reciprocal deposits.

19

At March 31, 2024, the estimated total amount of uninsured deposits was $32.0 billion, or 43%, of total deposits, compared with $33.2 billion, or 44%, at December 31, 2023, respectively. Our loan-to-deposit ratio was 78%, compared with 77% for the same respective time periods. See “Liquidity Risk Management” on page 31 for additional information on liquidity, including the ratio of available liquidity to uninsured deposits.

RISK MANAGEMENT

Risk management is an integral part of our operations and is a key determinant of our overall performance. We employ various strategies to prudently manage the risks to which our operations are exposed, including credit risk, market and interest rate risk, liquidity risk, strategic and business risk, operational risk, technology risk, cybersecurity risk, capital/financial reporting risk, legal/compliance risk (including regulatory risk), and reputational risk. These risks are overseen by various management committees including the Enterprise Risk Management Committee. For a more comprehensive discussion of these risks, see “Risk Factors” in our 2023 Form 10-K.

Credit Risk Management

Credit risk is the possibility of loss from the failure of a borrower, guarantor, or another obligor to fully perform under the terms of a credit-related contract. Credit risk arises primarily from our lending activities, as well as from off-balance sheet credit instruments. Credit policies, credit risk management, and credit examination functions inform and support the oversight of credit risk. Our credit policies emphasize strong underwriting standards and early detection of potential problem credits in order to develop and implement action plans on a timely basis to mitigate potential losses. These formal credit policies and procedures provide us with a framework for consistent underwriting and a basis for sound credit decisions at the local banking affiliate level.

Our business activity is conducted primarily within the geographic footprint of our banking affiliates. We strive to avoid the risk of undue concentrations of credit in any particular industry, collateral type, location, or with any individual customer or counterparty. For a more comprehensive discussion of our credit risk management, see “Credit Risk Management” in our 2023 Form 10-K.

U.S. Government Agency Guaranteed Loans

We participate in various guaranteed lending programs sponsored by U.S. government agencies, such as the Small Business Administration (“SBA”), Federal Housing Authority, U.S. Department of Veterans Affairs, Export-Import Bank of the U.S., and the U.S. Department of Agriculture. At March 31, 2024, $540 million of related loans were guaranteed, primarily by the SBA. The following schedule presents the composition of U.S. government agency guaranteed loans:

U.S. GOVERNMENT AGENCY GUARANTEED LOANS

| (Dollar amounts in millions) | March 31, 2024 | Percent guaranteed | December 31, 2023 | Percent guaranteed | |||||||||||||||||||

| Commercial | $ | 654 | 79 | % | $ | 664 | 80 | % | |||||||||||||||

| Commercial real estate | 25 | 76 | 24 | 79 | |||||||||||||||||||

| Consumer | 4 | 100 | 4 | 100 | |||||||||||||||||||

| Total loans | $ | 683 | 79 | % | $ | 692 | 80 | % | |||||||||||||||

20

Commercial Lending

The following schedule provides information regarding lending exposures to certain industries in our commercial lending portfolio:

COMMERCIAL LENDING BY INDUSTRY GROUP 1

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollar amounts in millions) | Amount | Percent | Amount | Percent | |||||||||||||||||||

| Retail trade | $ | 3,002 | 9.9 | % | $ | 2,995 | 9.8 | % | |||||||||||||||

| Real estate, rental and leasing | 3,002 | 9.9 | 2,946 | 9.6 | |||||||||||||||||||

| Finance and insurance | 2,780 | 9.1 | 2,918 | 9.5 | |||||||||||||||||||

| Healthcare and social assistance | 2,497 | 8.2 | 2,527 | 8.3 | |||||||||||||||||||

| Public Administration | 2,245 | 7.4 | 2,279 | 7.5 | |||||||||||||||||||

| Manufacturing | 2,238 | 7.3 | 2,190 | 7.2 | |||||||||||||||||||

| Wholesale trade | 1,994 | 6.5 | 1,850 | 6.0 | |||||||||||||||||||

| Transportation and warehousing | 1,513 | 5.0 | 1,499 | 4.9 | |||||||||||||||||||

Utilities 2 | 1,437 | 4.7 | 1,409 | 4.6 | |||||||||||||||||||

| Educational services | 1,275 | 4.2 | 1,298 | 4.2 | |||||||||||||||||||

| Construction | 1,273 | 4.2 | 1,355 | 4.4 | |||||||||||||||||||

| Hospitality and food services | 1,171 | 3.8 | 1,180 | 3.9 | |||||||||||||||||||

| Mining, quarrying, and oil and gas extraction | 1,107 | 3.6 | 1,133 | 3.7 | |||||||||||||||||||

| Professional, scientific, and technical services | 1,078 | 3.5 | 1,010 | 3.3 | |||||||||||||||||||

| Other Services (except Public Administration) | 1,060 | 3.5 | 1,047 | 3.4 | |||||||||||||||||||

Other 3 | 2,807 | 9.2 | 2,952 | 9.7 | |||||||||||||||||||

| Total | $ | 30,479 | 100.0 | % | $ | 30,588 | 100.0 | % | |||||||||||||||

1 Industry groups are determined by North American Industry Classification System (“NAICS”) codes.

2 Includes primarily utilities, power, and renewable energy.

3 No other industry group exceeds 3.3%.

Commercial Real Estate Loans

At March 31, 2024 and December 31, 2023, our CRE loan portfolio totaled $13.6 billion and $13.4 billion, respectively, representing 23% of the total loan portfolio for both periods. The majority of our CRE loans are secured by real estate primarily located within our geographic footprint. The following schedule presents the geographic distribution of our CRE loan portfolio based on the location of the primary collateral:

COMMERCIAL REAL ESTATE LENDING BY COLLATERAL LOCATION

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollar amounts in millions) | Amount | Percent | Amount | Percent | |||||||||||||||||||

| Arizona | $ | 1,727 | 12.7 | % | $ | 1,726 | 12.9 | % | |||||||||||||||

| California | 3,840 | 28.3 | 3,865 | 28.9 | |||||||||||||||||||

| Colorado | 718 | 5.3 | 709 | 5.3 | |||||||||||||||||||

| Nevada | 1,077 | 7.9 | 1,072 | 8.0 | |||||||||||||||||||

| Texas | 2,489 | 18.3 | 2,385 | 17.8 | |||||||||||||||||||

| Utah/Idaho | 2,232 | 16.5 | 2,214 | 16.6 | |||||||||||||||||||

| Washington/Oregon | 1,076 | 7.9 | 1,004 | 7.5 | |||||||||||||||||||

| Other | 419 | 3.1 | 396 | 3.0 | |||||||||||||||||||

| Total CRE | $ | 13,578 | 100.0 | % | $ | 13,371 | 100.0 | % | |||||||||||||||

21

Term CRE loans generally mature within a three- to seven-year period and consist of full, partial, and non-recourse guarantee structures. Typical term CRE loan structures include annually tested operating covenants that require loan rebalancing based on minimum debt service coverage, debt yield, or loan-to-value tests. Construction and land development loans generally mature in 18 to 36 months and contain full or partial recourse guarantee structures with one- to five-year extension options or roll-to-perm options that often result in term loans. At March 31, 2024, approximately 85% of our CRE loan portfolio was variable-rate, and approximately 21% of these variable-rate loans were swapped to a fixed rate.

Underwriting on commercial properties is primarily based on the economic viability of the project with significant consideration given to the creditworthiness and experience of the sponsor. We generally require that the owner’s equity be included prior to any advances. Re-margining requirements (required equity infusions upon a decline in value or cash flow of the collateral) are often included in the loan agreement along with guarantees of the sponsor. For a more comprehensive discussion of CRE loans and our underwriting, see “Commercial Real Estate Loans” in our 2023 Form 10-K.

The following schedule presents our CRE loan portfolio by collateral type:

COMMERCIAL REAL ESTATE LENDING BY COLLATERAL TYPE

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollar amounts in millions) | Amount | Percent | Amount | Percent | |||||||||||||||||||

| Commercial property | |||||||||||||||||||||||

| Multi-family | $ | 3,854 | 28.4 | % | $ | 3,709 | 27.7 | % | |||||||||||||||

| Industrial | 3,189 | 23.5 | 3,062 | 22.9 | |||||||||||||||||||

| Office | 1,946 | 14.3 | 1,984 | 14.8 | |||||||||||||||||||

| Retail | 1,502 | 11.1 | 1,503 | 11.2 | |||||||||||||||||||

| Hospitality | 662 | 4.9 | 688 | 5.2 | |||||||||||||||||||

| Land | 216 | 1.6 | 211 | 1.6 | |||||||||||||||||||

Other 1 | 1,684 | 12.4 | 1,682 | 12.6 | |||||||||||||||||||

Residential property 2 | |||||||||||||||||||||||

| Single family | 264 | 1.9 | 287 | 2.1 | |||||||||||||||||||

| Land | 99 | 0.7 | 90 | 0.7 | |||||||||||||||||||

| Condo/Townhome | 43 | 0.3 | 37 | 0.3 | |||||||||||||||||||

Other 1 | 119 | 0.9 | 118 | 0.9 | |||||||||||||||||||

| Total | $ | 13,578 | 100.0 | % | $ | 13,371 | 100.0 | % | |||||||||||||||

1 Included in the total amount of the “Other” commercial and residential categories was approximately $216 million and $202 million of unsecured loans at March 31, 2024 and December 31, 2023, respectively.

2 Residential property consists primarily of loans provided to commercial homebuilders for land, lot, and single-family housing developments.

As previously described, our CRE portfolio is diversified across geography and collateral type, with the largest concentration in multi-family. We provide additional analysis of our multi-family and office CRE portfolios below in view of increased investor interest in those collateral types in recent periods.

22

Multi-family

At March 31, 2024 and December 31, 2023, our multi-family loan portfolio totaled $3.9 billion and $3.7 billion, representing 28% of the total CRE loan portfolio for both periods. Approximately 36% of the multi-family CRE loan portfolio is scheduled to mature in the next 12 months. The following schedule presents the composition of our multi-family CRE loan portfolio and other related credit quality metrics:

MULTI-FAMILY CRE LOAN PORTFOLIO

| (Dollar amounts in millions) | March 31, 2024 | December 31, 2023 | |||||||||

| Multi-family CRE | |||||||||||

| Construction and land development | $ | 953 | $ | 902 | |||||||

| Term | 2,901 | 2,807 | |||||||||

| Total multi-family CRE | $ | 3,854 | $ | 3,709 | |||||||

| Credit quality metrics | |||||||||||

| Criticized loan ratio | 10.1 | % | 6.1 | % | |||||||

| Classified loan ratio | 0.8 | % | 0.5 | % | |||||||

| Nonaccrual loan ratio | — | % | — | % | |||||||

| Delinquency ratio | — | % | — | % | |||||||

| Net charge-offs, annualized | — | % | — | % | |||||||

| Ratio of allowance for credit losses to multi-family CRE loans, at period end | 2.28 | % | 1.70 | % | |||||||

The following schedules present our multi-family CRE loan portfolio by collateral location for the periods presented:

MULTI-FAMILY CRE LOAN PORTFOLIO BY COLLATERAL LOCATION

| (Dollar amounts in millions) | March 31, 2024 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Collateral Location | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Loan type | Arizona | California | Colorado | Nevada | Texas | Utah/ Idaho | Wash-ington | Other 1 | Total | |||||||||||||||||||||||||||||||||||||||||||||||

| Multi-family CRE | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Construction and land development | $ | 138 | $ | 167 | $ | 65 | $ | 62 | $ | 352 | $ | 49 | $ | 120 | $ | — | $ | 953 | ||||||||||||||||||||||||||||||||||||||

| Term | 280 | 995 | 89 | 193 | 671 | 360 | 251 | 62 | 2,901 | |||||||||||||||||||||||||||||||||||||||||||||||

Total Multi-family CRE | $ | 418 | $ | 1,162 | $ | 154 | $ | 255 | $ | 1,023 | $ | 409 | $ | 371 | $ | 62 | $ | 3,854 | ||||||||||||||||||||||||||||||||||||||

| % of total | 10.8 | % | 30.2 | % | 4.0 | % | 6.6 | % | 26.6 | % | 10.6 | % | 9.6 | % | 1.6 | % | 100.0 | % | ||||||||||||||||||||||||||||||||||||||

| (Dollar amounts in millions) | December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Collateral Location | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Loan type | Arizona | California | Colorado | Nevada | Texas | Utah/ Idaho | Wash-ington | Other 1 | Total | |||||||||||||||||||||||||||||||||||||||||||||||

| Multi-family CRE | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Construction and land development | $ | 118 | $ | 183 | $ | 46 | $ | 40 | $ | 359 | $ | 44 | $ | 112 | $ | — | $ | 902 | ||||||||||||||||||||||||||||||||||||||

| Term | 322 | 994 | 90 | 188 | 578 | 345 | 228 | 62 | 2,807 | |||||||||||||||||||||||||||||||||||||||||||||||

Total Multi-family CRE | $ | 440 | $ | 1,177 | $ | 136 | $ | 228 | $ | 937 | $ | 389 | $ | 340 | $ | 62 | $ | 3,709 | ||||||||||||||||||||||||||||||||||||||

| % of total | 11.9 | % | 31.7 | % | 3.7 | % | 6.1 | % | 25.3 | % | 10.4 | % | 9.2 | % | 1.7 | % | 100.0 | % | ||||||||||||||||||||||||||||||||||||||

1 Other included $55 million of multi-family loans with collateral located in New Mexico at both March 31, 2024 and December 31, 2023.

23

Office CRE loan portfolio

At March 31, 2024 and December 31, 2023, our office CRE loan portfolio totaled $1.9 billion and $2.0 billion, representing 14% and 15% of the total CRE loan portfolio, respectively. Approximately 32% of the office CRE loan portfolio is scheduled to mature in the next 12 months. The following schedule presents the composition of our office CRE loan portfolio and other related credit quality metrics:

OFFICE CRE LOAN PORTFOLIO

| (Dollar amounts in millions) | March 31, 2024 | December 31, 2023 | |||||||||

| Office CRE | |||||||||||

| Construction and land development | $ | 187 | $ | 191 | |||||||

| Term | 1,759 | 1,793 | |||||||||

| Total office CRE | $ | 1,946 | $ | 1,984 | |||||||

| Credit quality metrics | |||||||||||

| Criticized loan ratio | 11.0 | % | 11.9 | % | |||||||

| Classified loan ratio | 7.6 | % | 8.9 | % | |||||||

| Nonaccrual loan ratio | 1.4 | % | 2.4 | % | |||||||

| Delinquency ratio | 2.1 | % | 2.3 | % | |||||||

| Net charge-offs, annualized | (0.1) | % | 0.2 | % | |||||||

| Ratio of allowance for credit losses to office CRE loans, at period end | 4.01 | % | 3.80 | % | |||||||

The following schedules present our office CRE loan portfolio by collateral location for the periods presented:

OFFICE CRE LOAN PORTFOLIO BY COLLATERAL LOCATION

| (Dollar amounts in millions) | March 31, 2024 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Collateral Location | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Loan type | Arizona | California | Colorado | Nevada | Texas | Utah/ Idaho | Wash-ington | Other 1 | Total | |||||||||||||||||||||||||||||||||||||||||||||||

| Office CRE | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Construction and land development | $ | — | $ | 44 | $ | — | $ | 6 | $ | 23 | $ | 31 | $ | 83 | $ | — | $ | 187 | ||||||||||||||||||||||||||||||||||||||

| Term | 277 | 375 | 92 | 84 | 192 | 485 | 225 | 29 | 1,759 | |||||||||||||||||||||||||||||||||||||||||||||||

Total Office CRE | $ | 277 | $ | 419 | $ | 92 | $ | 90 | $ | 215 | $ | 516 | $ | 308 | $ | 29 | $ | 1,946 | ||||||||||||||||||||||||||||||||||||||

| % of total | 14.3 | % | 21.5 | % | 4.7 | % | 4.6 | % | 11.1 | % | 26.5 | % | 15.8 | % | 1.5 | % | 100.0 | % | ||||||||||||||||||||||||||||||||||||||

| (Dollar amounts in millions) | December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Collateral Location | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Loan type | Arizona | California | Colorado | Nevada | Texas | Utah/ Idaho | Wash-ington | Other 1 | Total | |||||||||||||||||||||||||||||||||||||||||||||||

| Office CRE | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Construction and land development | $ | — | $ | 64 | $ | — | $ | 2 | $ | 22 | $ | 29 | $ | 74 | $ | — | $ | 191 | ||||||||||||||||||||||||||||||||||||||

| Term | 281 | 412 | 92 | 86 | 179 | 488 | 226 | 29 | 1,793 | |||||||||||||||||||||||||||||||||||||||||||||||

Total Office CRE | $ | 281 | $ | 476 | $ | 92 | $ | 88 | $ | 201 | $ | 517 | $ | 300 | $ | 29 | $ | 1,984 | ||||||||||||||||||||||||||||||||||||||

| % of total | 14.2 | % | 24.0 | % | 4.6 | % | 4.4 | % | 10.1 | % | 26.1 | % | 15.1 | % | 1.5 | % | 100.0 | % | ||||||||||||||||||||||||||||||||||||||

1 No other geography exceeded $17 million at both March 31, 2024 and December 31, 2023.

Consumer Loans

We originate first-lien residential home mortgages considered to be of prime quality. We generally hold variable-rate loans in our portfolio and sell “conforming” fixed-rate loans to third parties, including Federal National Mortgage Association and Federal Home Loan Mortgage Corporation, for which we make representations and warranties that the loans meet certain underwriting and collateral documentation standards.

24

We also originate home equity credit lines (“HECLs”). At both March 31, 2024 and December 31, 2023, our HECL portfolio totaled $3.4 billion. Approximately 38% and 39% of our HECLs are secured by first liens for the same respective time periods.

At March 31, 2024, loans representing less than 1% of the outstanding balance in the HECL portfolio were estimated to have combined loan-to-value (“CLTV”) ratios above 100%. An estimated CLTV ratio is the ratio of our loan plus any prior lien amounts divided by the estimated current collateral value. At origination, underwriting standards for the HECL portfolio generally include a maximum 80% CLTV with a Fair Isaac Corporation (“FICO”) credit score greater than 700.

Approximately 91% of our HECL portfolio is still in the draw period, and about 19% of those loans are scheduled to begin amortizing within the next five years. We believe the risk of loss and borrower default in the event of a loan becoming fully amortizing and the effect of significant interest rate changes is low, given the rate shock analysis performed at origination. The ratio of HECL net charge-offs (recoveries) for the trailing twelve months to average balances at both March 31, 2024 and December 31, 2023, was 0.05%. See Note 6 of the Notes to Consolidated Financial Statements for additional information on the credit quality of the HECL portfolio.

Nonperforming Assets

Nonperforming assets include nonaccrual loans and other real estate owned (“OREO”) or foreclosed properties. The following schedule presents our nonperforming assets:

NONPERFORMING ASSETS

| (Dollar amounts in millions) | March 31, 2024 | December 31, 2023 | |||||||||

Nonaccrual loans 1 | $ | 248 | $ | 222 | |||||||

Other real estate owned 2 | 6 | 6 | |||||||||

| Total nonperforming assets | $ | 254 | $ | 228 | |||||||

Ratio of nonperforming assets to net loans and leases1 and other real estate owned 2 | 0.44 | % | 0.39 | % | |||||||

| Accruing loans past due 90 days or more | $ | 3 | $ | 3 | |||||||

Ratio of accruing loans past due 90 days or more to loans and leases 1 | 0.01 | % | 0.01 | % | |||||||

Nonaccrual loans1 and accruing loans past due 90 days or more | $ | 251 | $ | 225 | |||||||

Ratio of nonperforming assets1 and accruing loans past due 90 days or more to loans and leases1 and other real estate owned 2 | 0.44 | % | 0.40 | % | |||||||

Nonaccrual loans1 current as to principal and interest payments | 56.0 | % | 48.8 | % | |||||||

1 Includes loans held for sale.

2 Does not include banking premises held for sale.

Nonperforming assets as a percentage of loans and leases and OREO increased to 0.44% at March 31, 2024, compared with 0.39% at December 31, 2023. Total nonaccrual loans at March 31, 2024 increased to $248 million from $222 million at December 31, 2023, primarily due to a small number of loans in the commercial and industrial and term commercial real estate portfolios. See Note 6 of the Notes to Consolidated Financial Statements for more information on nonaccrual loans.

Loan Modifications

Loans may be modified in the normal course of business for competitive reasons or to strengthen our collateral position. Loan modifications may also occur when the borrower experiences financial difficulty and needs temporary or permanent relief from the original contractual terms of the loan. For the first three months of 2024 and 2023, loans that have been modified to accommodate a borrower experiencing financial difficulties totaled $123 million, and $97 million, respectively.

25

If a modified loan is on nonaccrual and performs for at least six months according to the modified terms, and an analysis of the customer’s financial condition indicates that we are reasonably assured of repayment of the modified principal and interest, the loan may be returned to accrual status. The borrower’s payment performance prior to and following the modification is taken into account to determine whether a loan should be returned to accrual status.

ACCRUING AND NONACCRUING MODIFIED LOANS TO BORROWERS EXPERIENCING FINANCIAL DIFFICULTY

| Three Months Ended March 31, | |||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Modified loans – accruing | $ | 116 | $ | 96 | |||||||

| Modified loans – nonaccruing | 7 | 1 | |||||||||

| Total | $ | 123 | $ | 97 | |||||||

For additional information regarding loan modifications to borrowers experiencing financial difficulty, see Note 6 of the Notes to Consolidated Financial Statements.

Allowance for Credit Losses

The ACL includes the ALLL and the RULC. The ACL represents our estimate of current expected credit losses

related to the loan and lease portfolio and unfunded lending commitments as of the balance sheet date. To determine

the adequacy of the allowance, our loan and lease portfolio is segmented based on loan type.

The RULC is a reserve for potential losses associated with off-balance sheet commitments and is included in “Other

liabilities” on the consolidated balance sheet. Any related increases or decreases in the reserve are included in

“Provision for unfunded lending commitments” on the consolidated statement of income.

26

The following schedule presents the changes in and allocation of the ACL:

CHANGES IN THE ALLOWANCE FOR CREDIT LOSSES

| (Dollar amounts in millions) | Three Months Ended March 31, 2024 | Twelve Months Ended December 31, 2023 | Three Months Ended March 31, 2023 | ||||||||||||||

| Loans and leases outstanding | $ | 58,109 | $ | 57,779 | $ | 56,331 | |||||||||||

| Average loans and leases outstanding: | |||||||||||||||||

| Commercial | 30,482 | 30,519 | 30,678 | ||||||||||||||

| Commercial real estate | 13,504 | 13,023 | 12,876 | ||||||||||||||

| Consumer | 13,921 | 13,198 | 12,599 | ||||||||||||||

| Total average loans and leases outstanding | $ | 57,907 | $ | 56,740 | $ | 56,153 | |||||||||||

| Allowance for loan and lease losses: | |||||||||||||||||

| Balance at beginning of period | $ | 684 | $ | 572 | $ | 572 | |||||||||||

| Provision for loan losses | 21 | 148 | 46 | ||||||||||||||

| Charge-offs: | |||||||||||||||||

| Commercial | 10 | 45 | 3 | ||||||||||||||

| Commercial real estate | — | 3 | — | ||||||||||||||

| Consumer | 4 | 14 | 4 | ||||||||||||||

| Total | 14 | 62 | 7 | ||||||||||||||

| Recoveries: | |||||||||||||||||

| Commercial | 6 | 20 | 6 | ||||||||||||||

| Commercial real estate | 1 | — | — | ||||||||||||||

| Consumer | 1 | 6 | 1 | ||||||||||||||

| Total | 8 | 26 | 7 | ||||||||||||||

| Net loan and lease charge-offs | 6 | 36 | — | ||||||||||||||

| Balance at end of period | $ | 699 | $ | 684 | $ | 618 | |||||||||||

| Reserve for unfunded lending commitments: | |||||||||||||||||

| Balance at beginning of period | $ | 45 | $ | 61 | $ | 61 | |||||||||||

| Provision for unfunded lending commitments | (8) | (16) | (1) | ||||||||||||||

| Balance at end of period | $ | 37 | $ | 45 | $ | 60 | |||||||||||

| Total allowance for credit losses: | |||||||||||||||||

| Allowance for loan and lease losses | $ | 699 | $ | 684 | $ | 618 | |||||||||||

| Reserve for unfunded lending commitments | 37 | 45 | 60 | ||||||||||||||

| Total allowance for credit losses | $ | 736 | $ | 729 | $ | 678 | |||||||||||

| Ratio of allowance for credit losses to net loans and leases, at period end | 1.27 | % | 1.26 | % | 1.20 | % | |||||||||||

| Ratio of allowance for credit losses to nonaccrual loans, at period end | 297 | % | 328 | % | 396 | % | |||||||||||

| Ratio of allowance for credit losses to nonaccrual loans and accruing loans past due 90 days or more, at period end | 293 | % | 324 | % | 392 | % | |||||||||||

Ratio of total net charge-offs to average loans and leases 1 | 0.04 | % | 0.06 | % | — | % | |||||||||||

Ratio of commercial net charge-offs to average commercial loans 1 | 0.05 | % | 0.08 | % | (0.04) | % | |||||||||||

Ratio of commercial real estate net charge-offs to average commercial real estate loans 1 | (0.03) | % | 0.02 | % | — | % | |||||||||||

Ratio of consumer net charge-offs to average consumer loans 1 | 0.09 | % | 0.06 | % | 0.10 | % | |||||||||||

1 Ratios are annualized for the periods presented except for the period representing the full twelve months.

During the first three months of 2024, the total ACL increased to $736 million from $729 million. The increase in the ACL primarily reflects incremental reserves associated with portfolio-specific risks including commercial real estate and modest deterioration in credit quality, partially offset by improvements in economic forecasts. See Note 6 of the Notes to Consolidated Financial Statements for additional information related to the ACL and credit trends experienced in each portfolio segment.

27

Interest Rate and Market Risk Management

Interest rate and market risk is the risk of losses to current or future earnings and capital from changes in interest rates and other market conditions. Because we engage in transactions involving various financial products, we are exposed to interest rate and market risk. For a more comprehensive discussion of our interest rate and market risk management, see “Interest Rate and Market Risk Management” in our 2023 Form 10-K.